This episode was first published on The Business Engineer in December 2025. In retrospect, it belongs more appropriately to the AI Supercycle series, as it already provided a framework for understanding the emerging world order.

The geopolitical layer, sitting on top of the macroeconomic and technological layers, is likely to be the decisive factor shaping the next phase of AI development. Understanding how these three forces interact will be critical to making sense of where the AI landscape is headed.

Globalization is not over; it’s instead getting redefined. How?

Neil Shearing, Group Chief Economist at Capital Economics (80 economists spanning the globe), is an Associate Fellow at Chatham House.

This analysis synthesizes his book The Fractured Age with direct insights from a Business Engineer podcast conversation, which shows the structural reality we’re living through in the coming decades.

You can get the book on Amazon. You can also check Neil Shearing’s Work on Capital Economics.

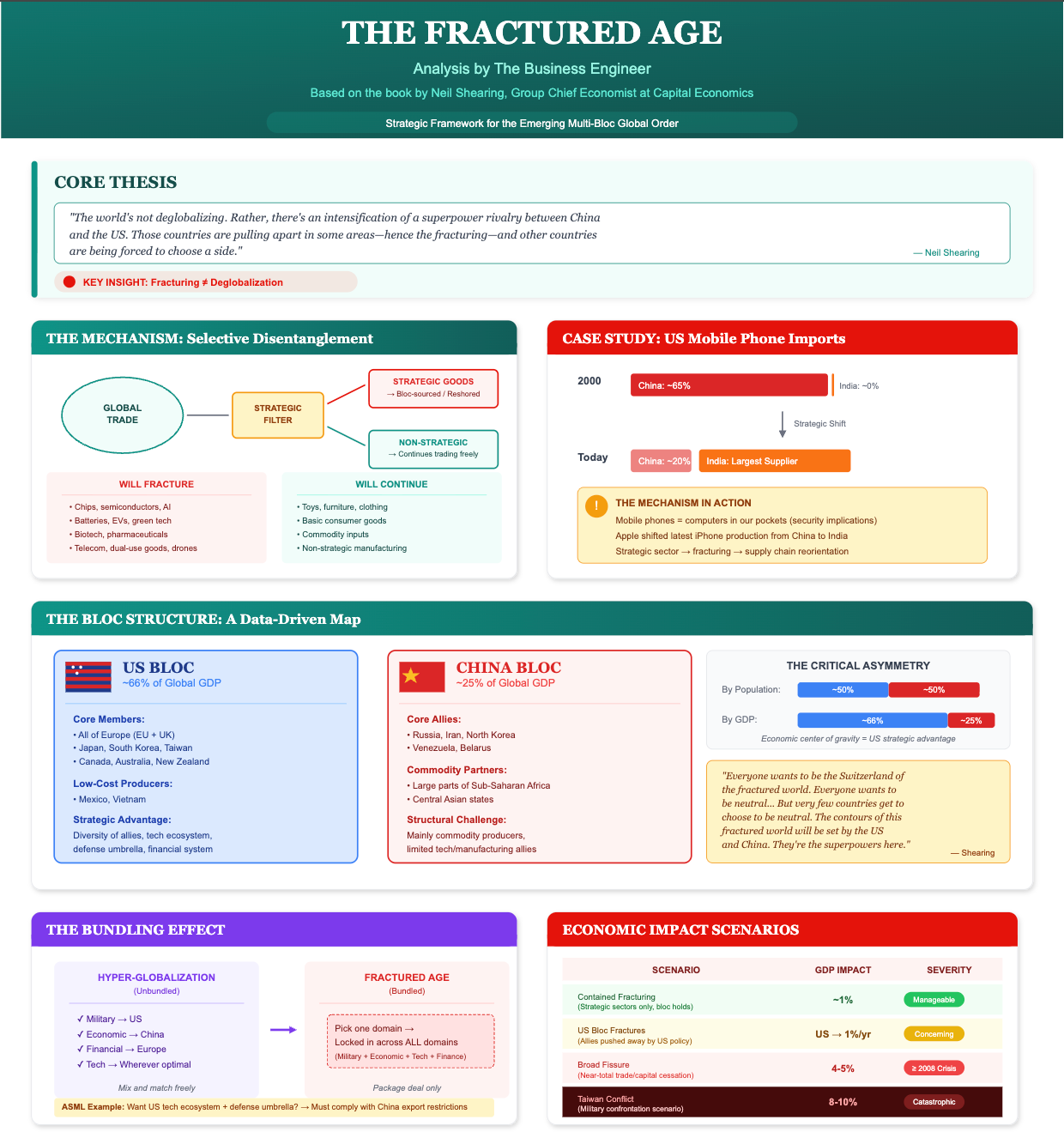

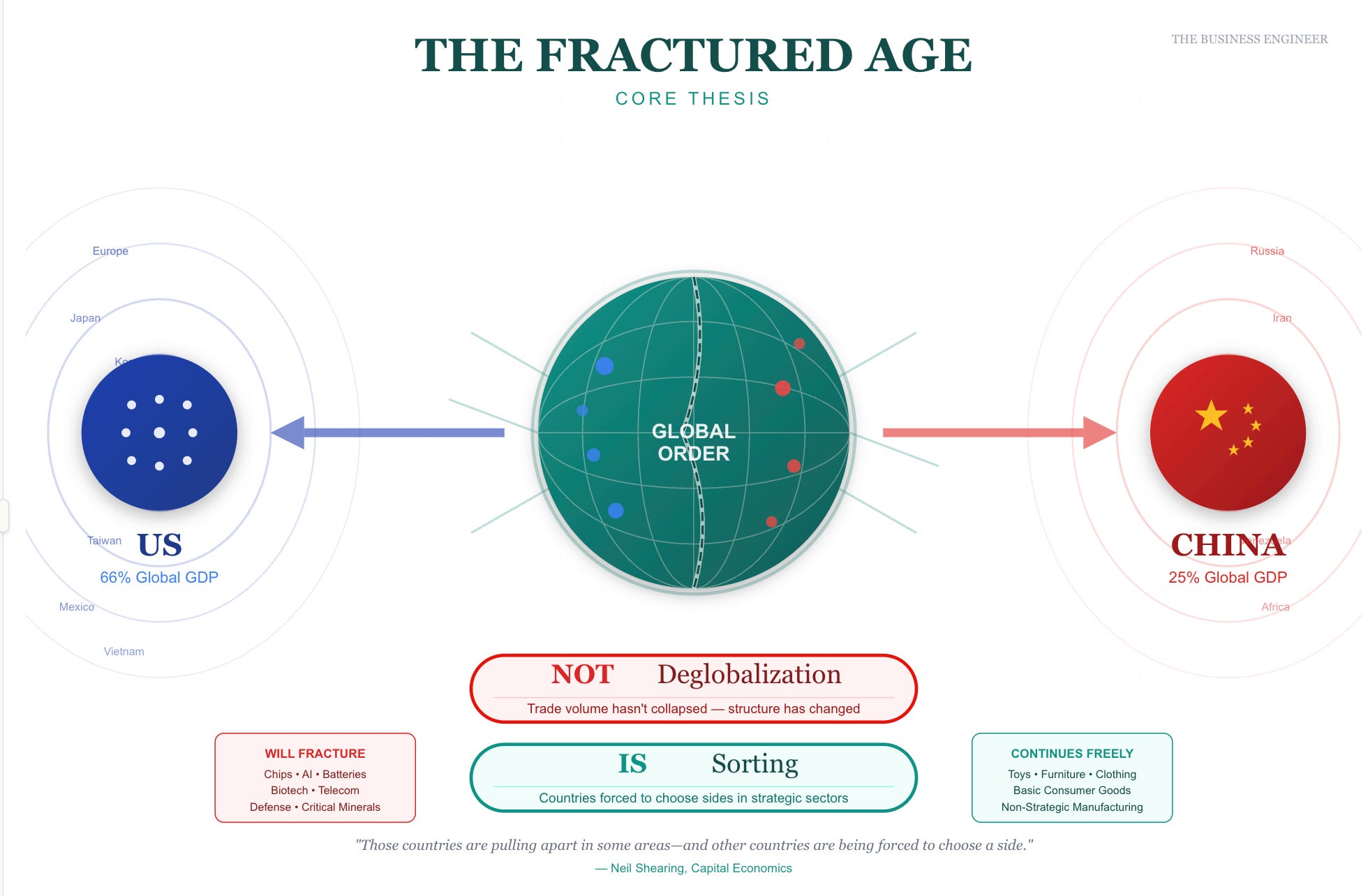

CORE THESIS

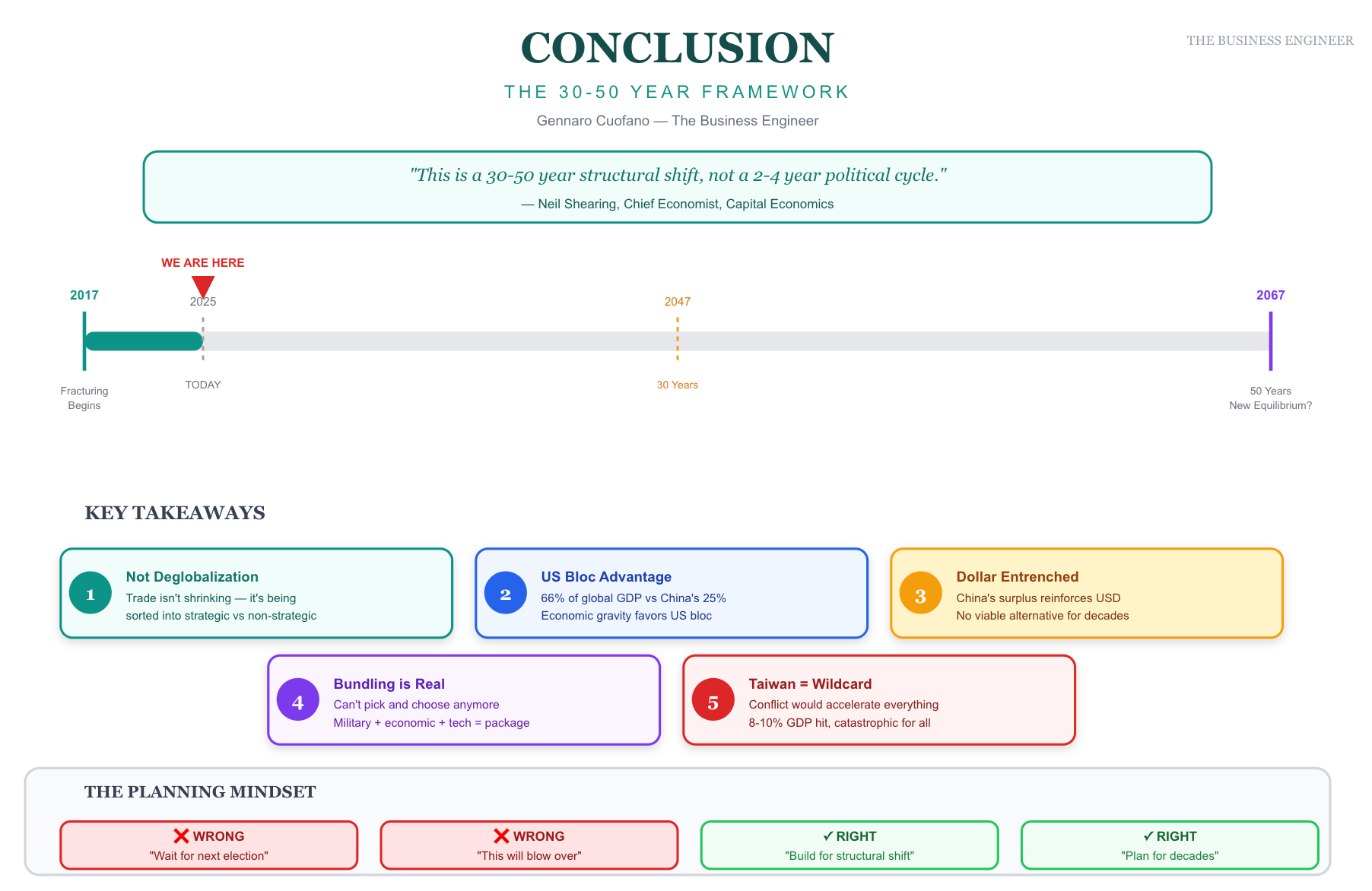

“The world’s not deglobalising. Rather, there’s an intensification of a superpower rivalry between China and the US. Those countries are pulling apart in some areas—hence the fracturing—and other countries are being forced to choose a side.”

— Neil Shearing, Capital Economics

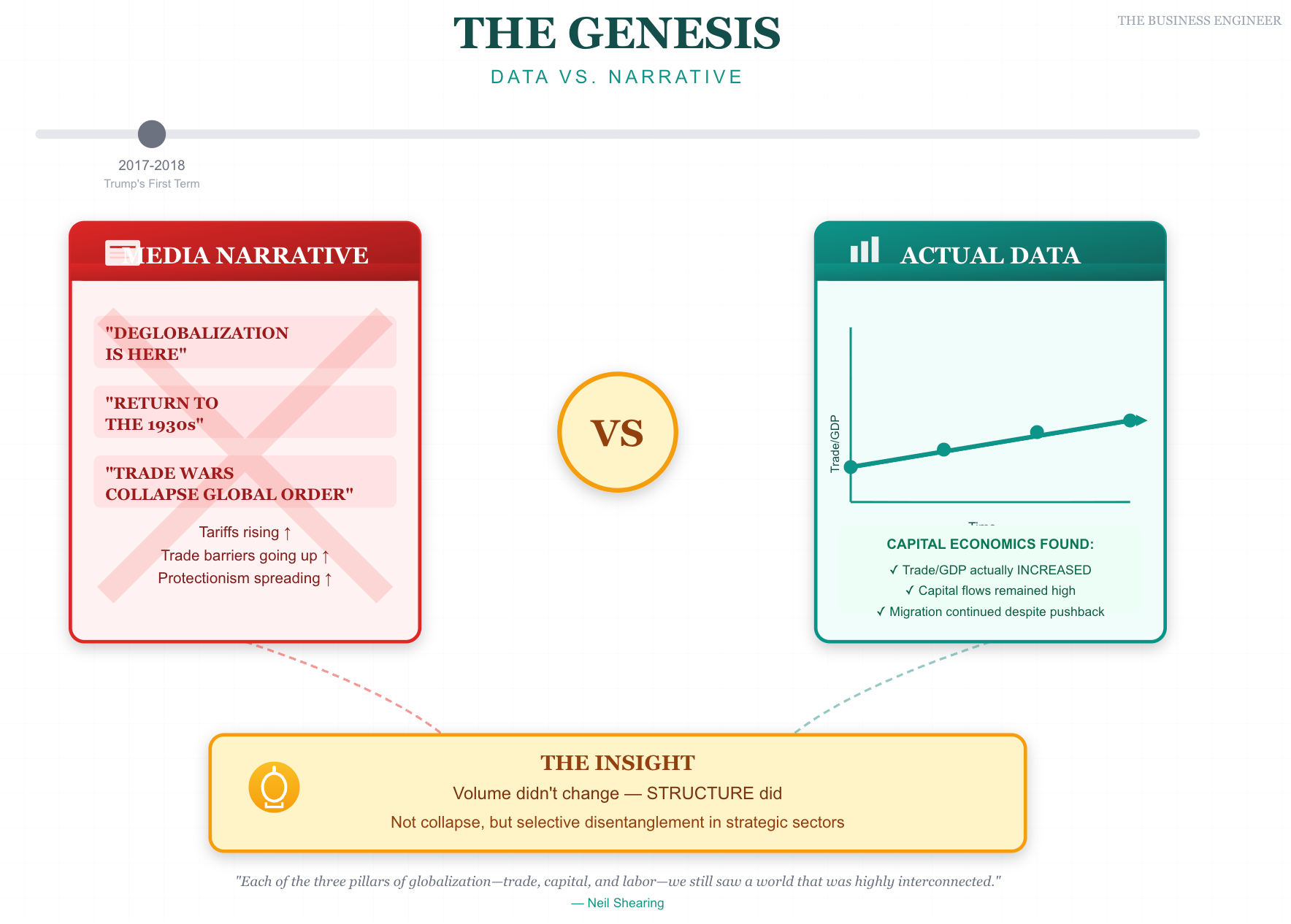

THE GENESIS: DATA VS. NARRATIVE

The thesis emerged from a disconnect. In 2017-2018, during Trump’s first term, media narratives proclaimed deglobalization. Tariffs were rising. Trade barriers were going up. The world was returning to the 1930s.

But when Capital Economics examined the data, they found no evidence of this collapse. Trade as a share of global GDP actually increased slightly during the first Trump administration. Global capital flows remained extremely high by historic standards. Migration flows continued despite Western government pushback.

“Each of the three pillars of globalization—trade, capital, and labor—we still saw a world that was highly interconnected. And yet something had changed. It was clear that something had changed.”

What changed was not the volume but the structure. The defining feature was an intensification of superpower rivalry causing selective disentanglement—not universal retreat, but sorting.

THE MECHANISM: SELECTIVE DISENTANGLEMENT

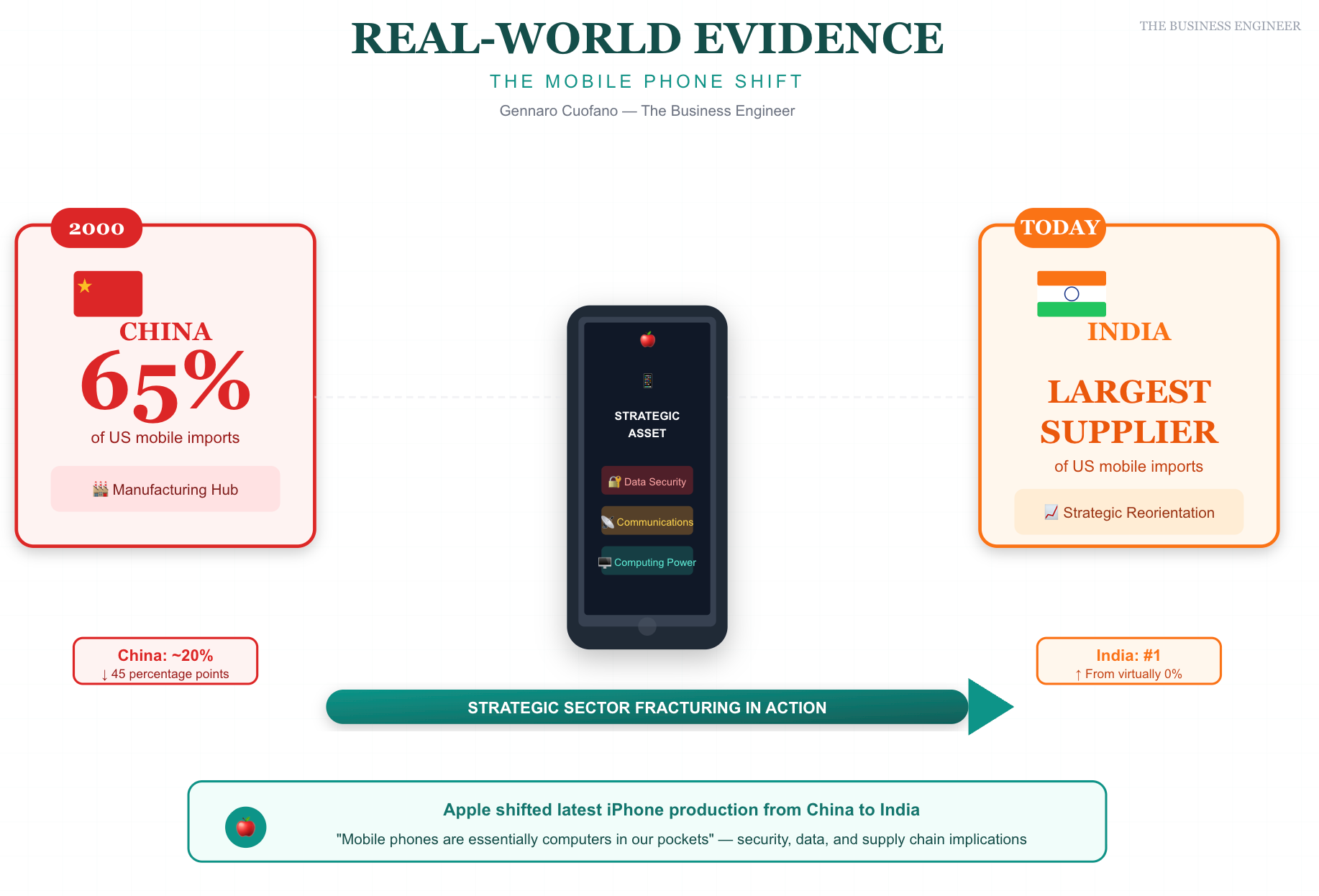

Real-World Evidence: The Mobile Phone Shift

Shearing provides a concrete example of fracturing in action—how America sources its mobile phones:

Metric2000TodayChina’s share of US mobile phone imports~65%~20%India’s share of US mobile phone imports~0%Largest supplierThis shift occurred in a strategically important sector—mobile phones are “essentially computers in our pockets” with massive data and security implications. Apple made the strategic decision to shift production of the latest iPhone out of China into India. That’s the fracturing mechanism in action.

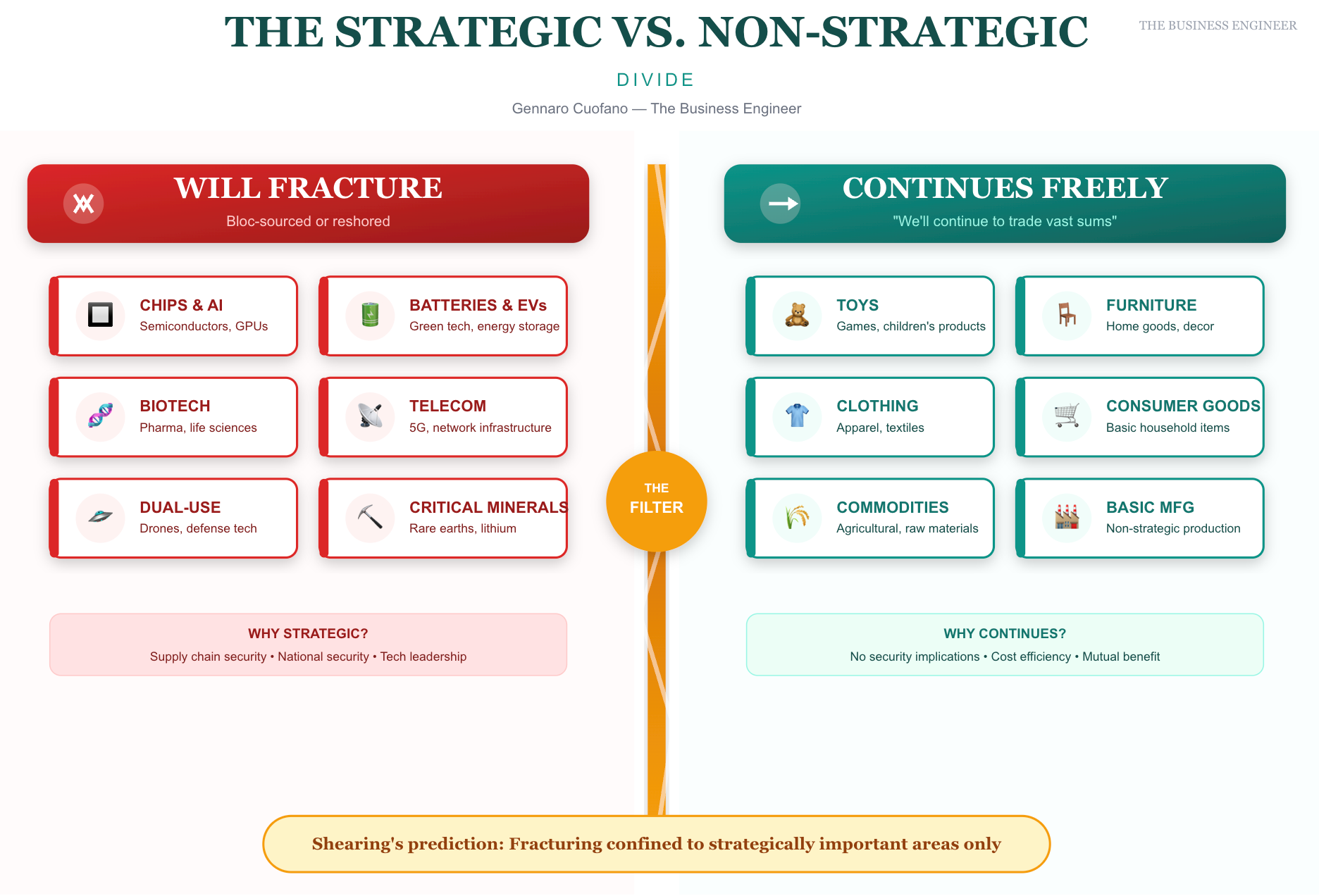

The Strategic vs. Non-Strategic Divide

Shearing’s core prediction: fracturing will be confined to strategically important areas—anything affecting supply chain security, national security, or global technological leadership.

WILL FRACTURE (Bloc-sourced or reshored):

Chips, semiconductors, AI

Batteries, EVs, green tech

Biotech, pharmaceuticals

Dual-use goods (drones)

Telecommunications equipment

Critical minerals, rare earths

WILL CONTINUE TRADING (”We’ll continue to trade vast sums”):

Toys

Furniture

Clothing

Basic consumer goods

Commodity inputs

Non-strategic manufacturing

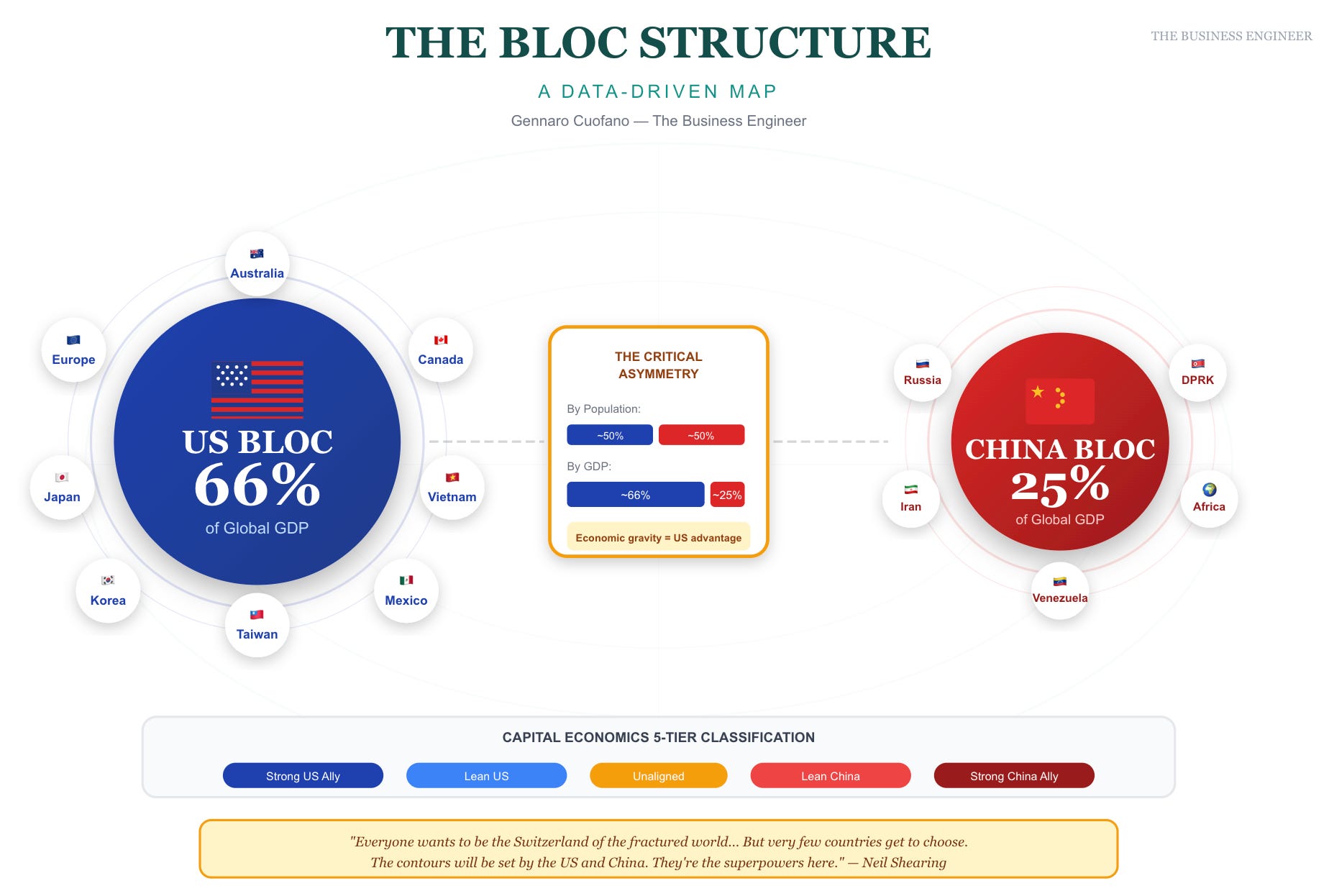

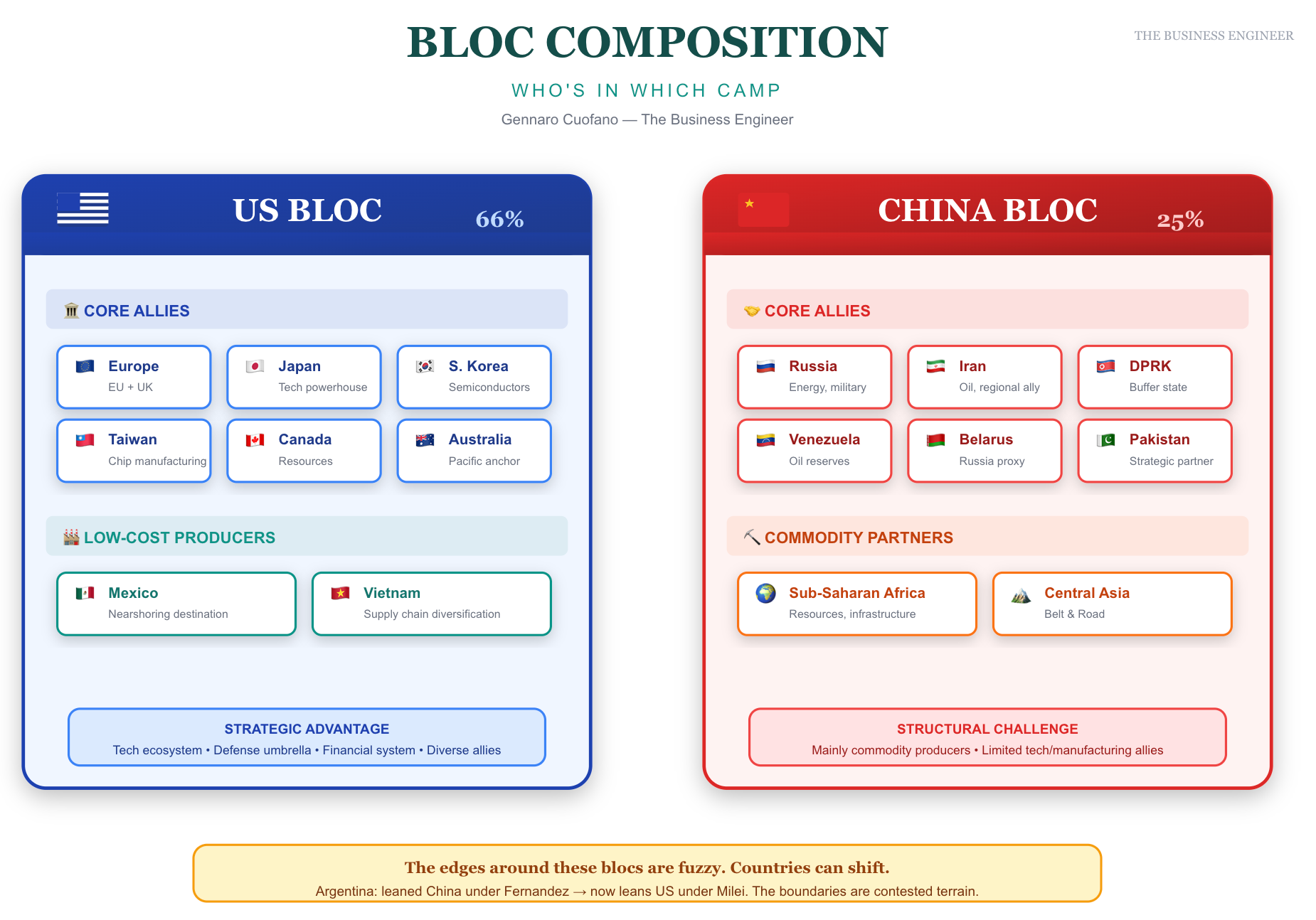

THE BLOC STRUCTURE: A DATA-DRIVEN MAP

Capital Economics developed a methodology to sort countries into blocs using data on trade relationships, capital flows, and cultural/political/geopolitical links. The result is a five-tier classification:

Strong US ally

Lean towards US

Unaligned (a small number will successfully remain here)

Lean towards China

Strong China ally

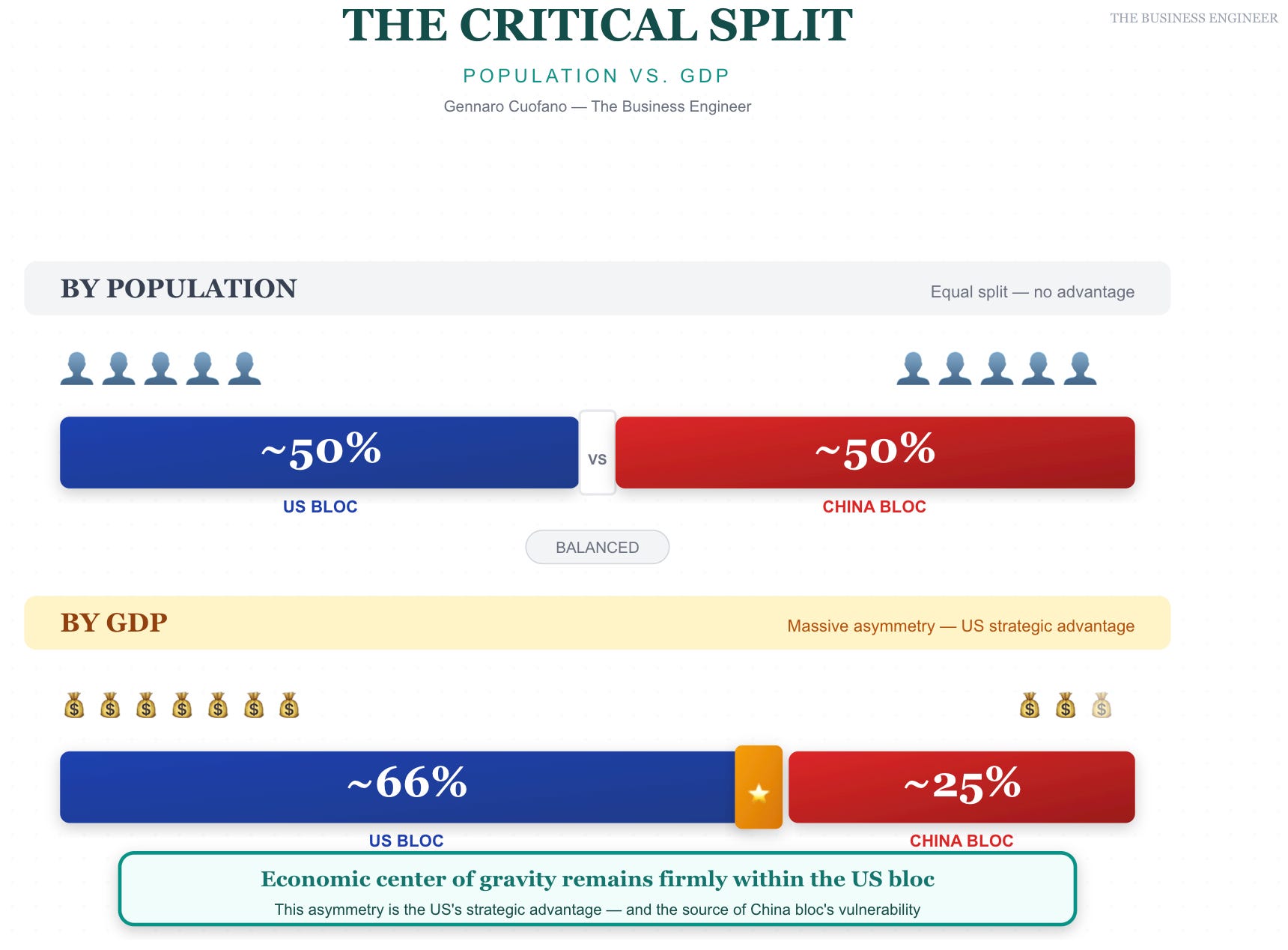

The Critical Split: Population vs. GDP

The center of economic gravity remains firmly within the US bloc. This asymmetry is the US’s strategic advantage—and the source of China bloc’s vulnerability.

Bloc Composition

US Bloc: All of Europe, Japan, Korea, Taiwan, low-cost producers (Mexico, Vietnam), resource countries (Canada, Australia)

China Bloc: Mainly commodity producers—Russia, Iran, Venezuela, large parts of sub-Saharan Africa

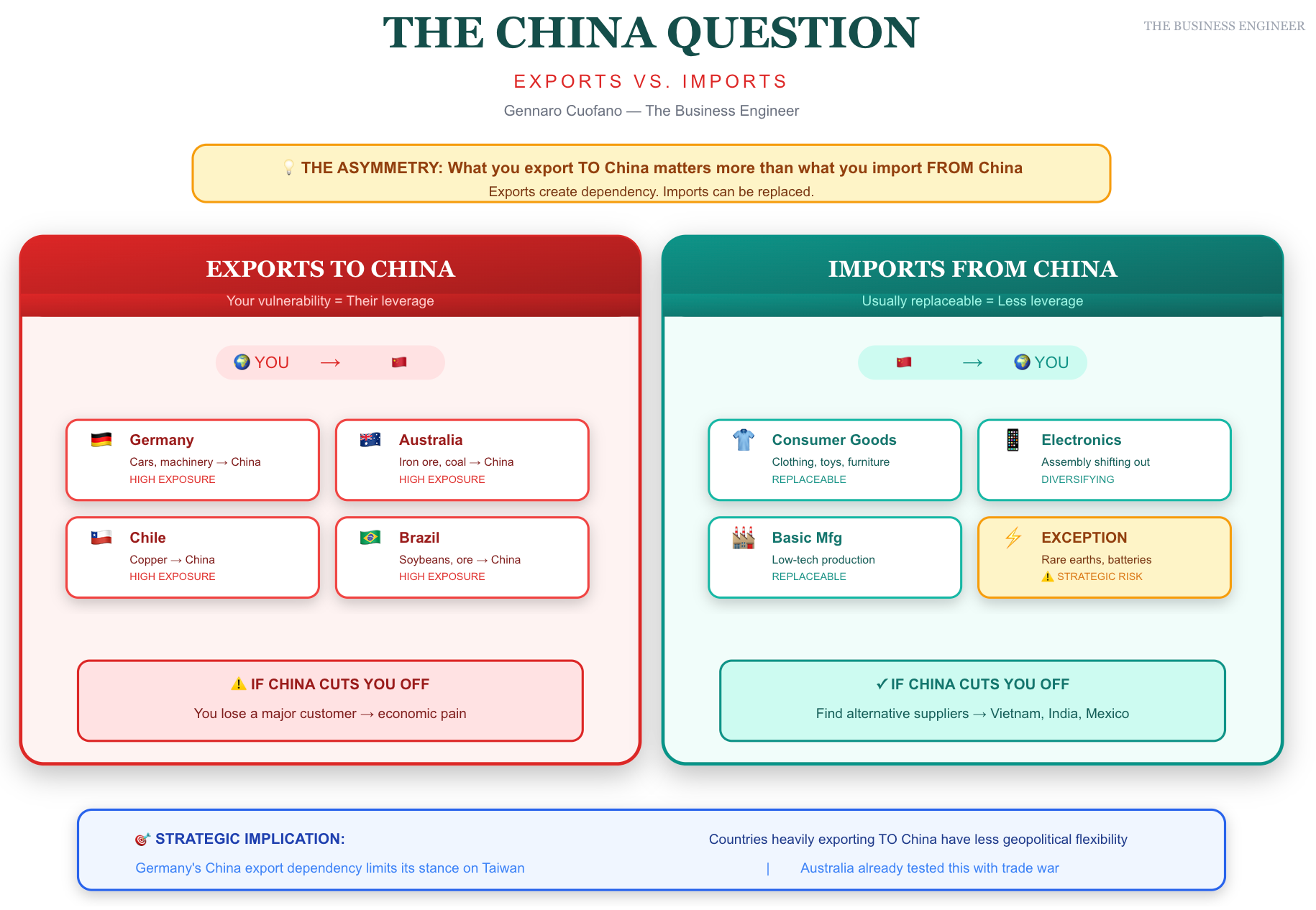

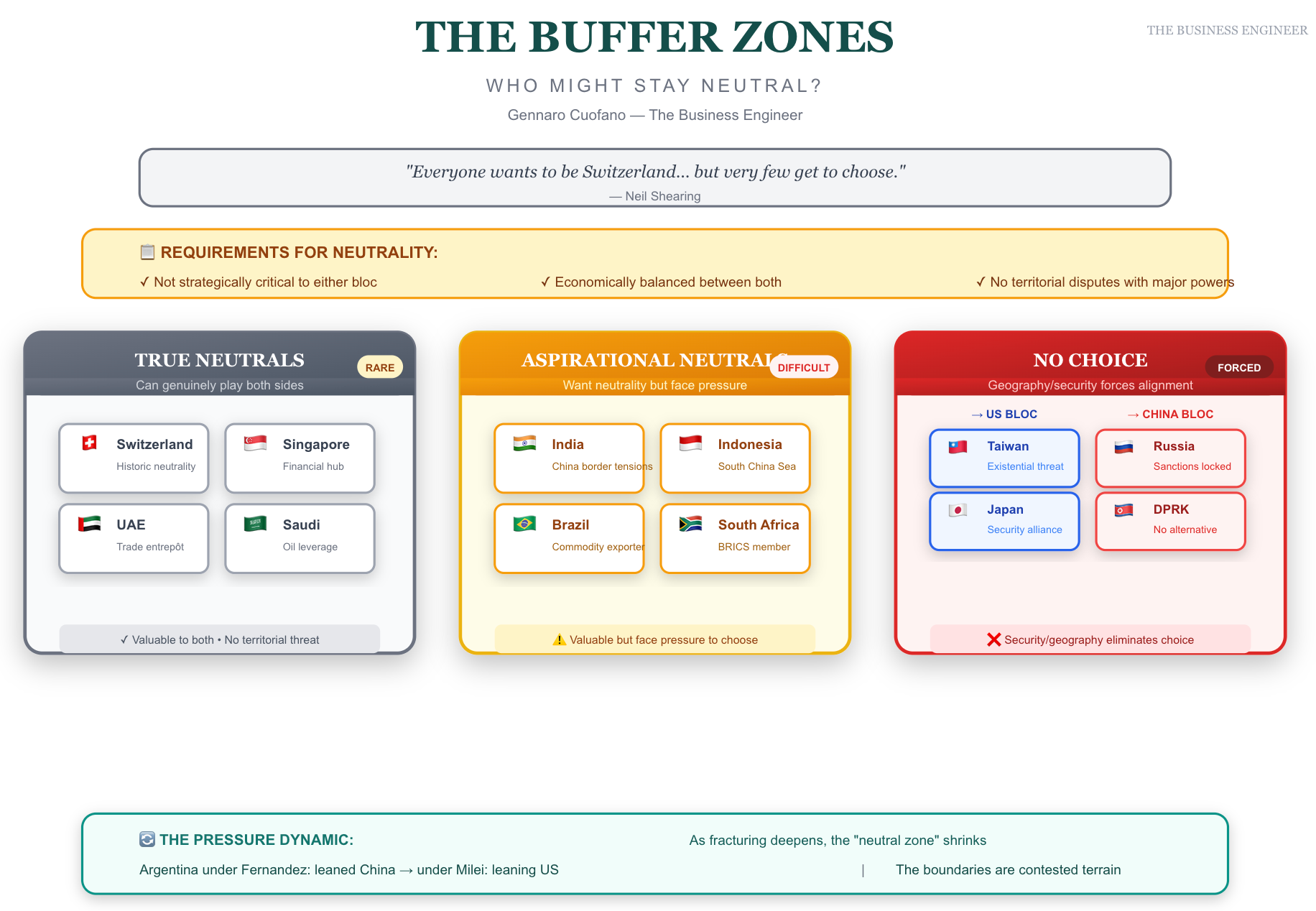

Key insight: The edges around these blocs are fuzzy. Countries can shift. Argentina leaned toward China under Fernandez, now leans toward US under Milei. The boundaries are contested terrain.

“Everyone wants to be the Switzerland of the fractured world. Everyone wants to be neutral. I’ve been through the Middle East, through Asia, through parts of Europe, Latin America—everyone’s trying to position themselves as being neutral. But very few countries get to choose to be neutral. The contours of this fractured world will be set by the US and China. They’re the superpowers here.”

— Neil Shearing

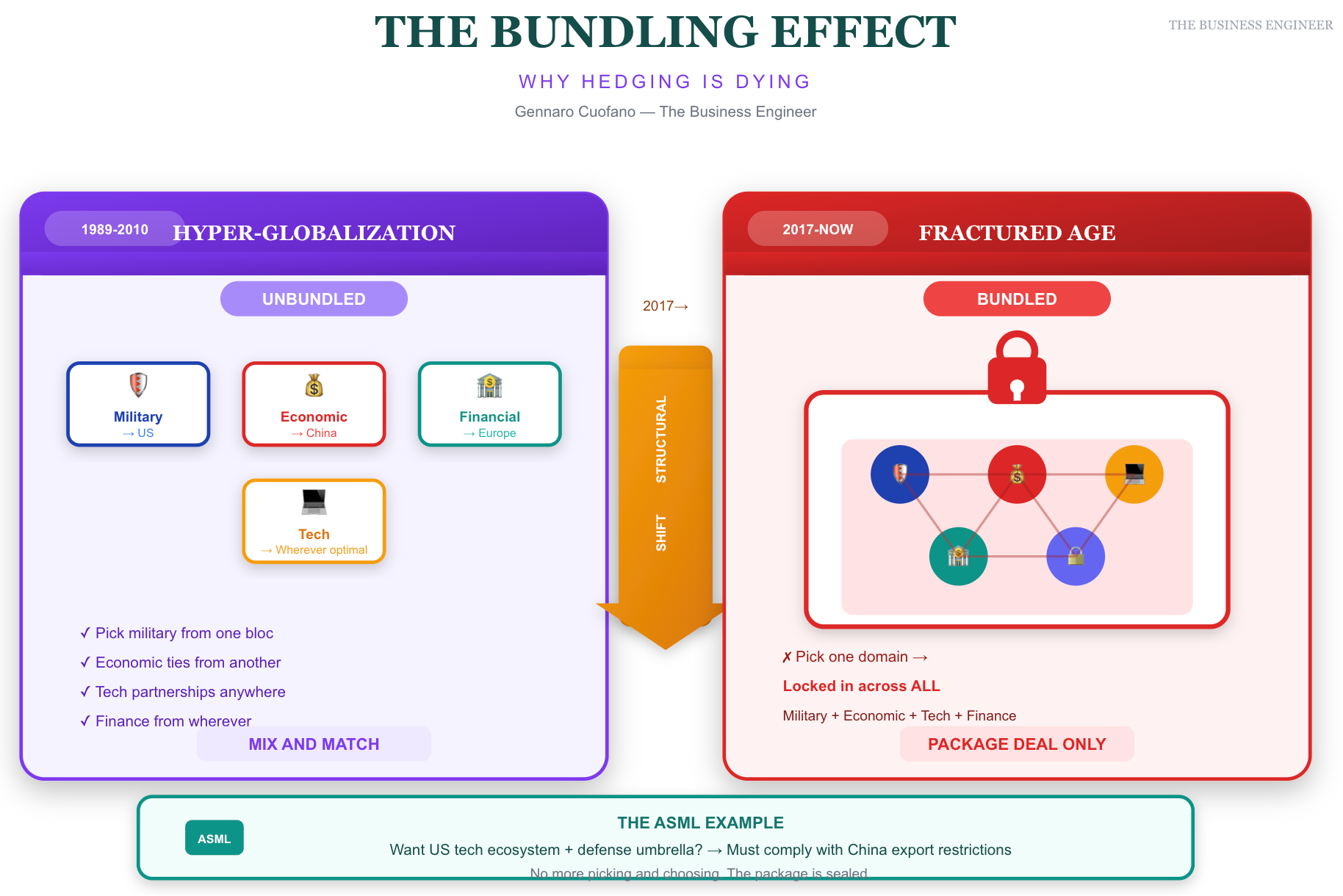

THE BUNDLING EFFECT: WHY HEDGING IS DYING

A critical structural shift identified in the conversation: the unbundling that enabled hyper-globalization is reversing.

During hyper-globalization, you could pick and choose:

Military alignment with the US

Economic integration with China

Financial ties with Europe

Tech partnerships wherever optimal

Now it’s bundled. If you pick one domain, you increasingly get locked into that bloc across all domains. The ASML case illustrates this perfectly: if you want to remain in the US tech ecosphere and under the US defense umbrella, you comply with technology export restrictions to China.

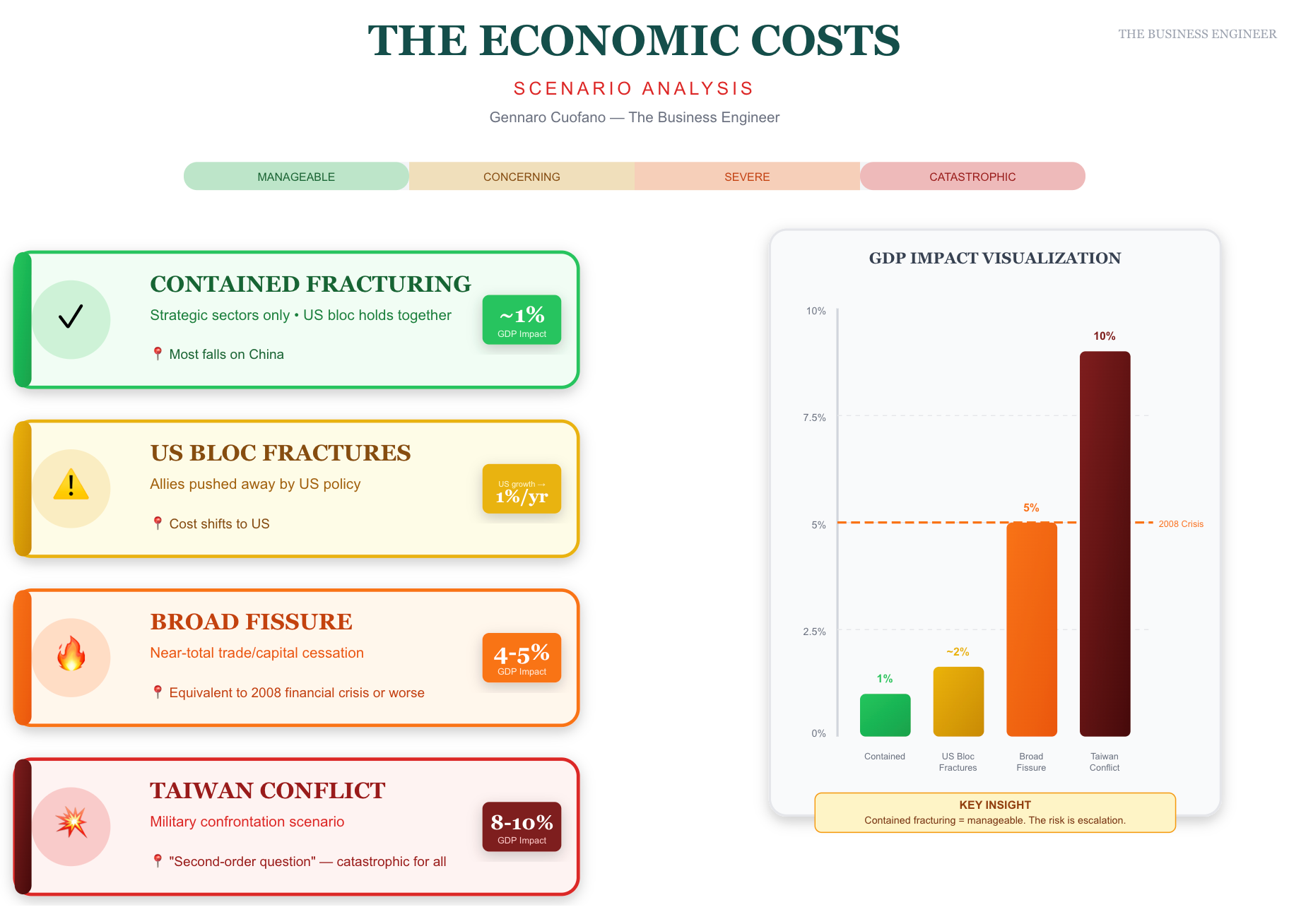

THE ECONOMIC COSTS: SCENARIO ANALYSIS

CRITICAL INSIGHT: “America First policies would actually be America Last. America’s great strength in this fractured world is the diversity of its allies. If the US pushes those countries away, then it becomes much more difficult for multinationals to reorganize their supply chains and meet the national security challenges.”

— Neil Shearing

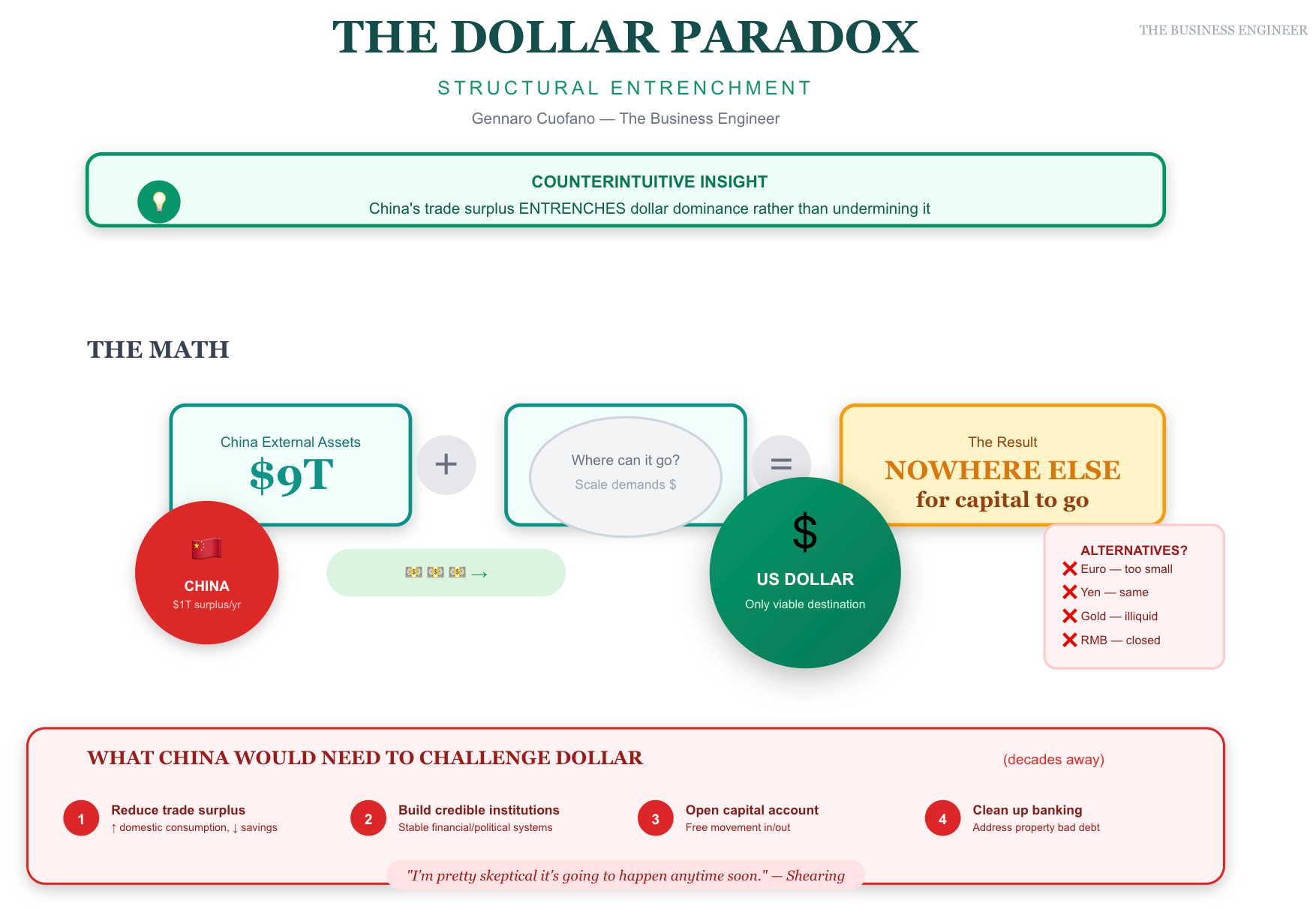

THE DOLLAR’S STRUCTURAL ENTRENCHMENT

Shearing provides a counterintuitive insight on the dollar’s position: China’s trade surplus actually entrenches rather than undermines dollar dominance.

The numbers:

China holds $9 trillion in external assets

China runs a $1 trillion annual trade surplus

There’s nowhere else for this capital to go except dollar-based assets

China may wish to diversify away from US securities—and has reduced Treasury holdings—but the sheer scale of its surplus means dollar assets remain the only viable destination. The renminbi will become more widely used in China-ally transactions, but won’t fundamentally challenge the dollar because China’s trade surplus keeps recycling into dollar assets.

What Would China Need to Challenge the Dollar?

Shearing outlines the prerequisites—each would take decades:

Reduce the trade surplus — increase domestic consumption, reduce savings

Build credible institutions — stable, reliable financial and political institutions globally

Open the capital account — investors must be able to get money in and out freely

Clean up the banking sector — address bad debt from property sector overinvestment

Shearing’s assessment: “I’m pretty skeptical it’s going to happen anytime soon.”

THE CHINA QUESTION: EXPORTS VS. IMPORTS

Shearing reframes the China trade debate in a way that cuts through populist narratives:

“The big issue in my mind is not how much China exports. That’s not the issue. It’s how little it imports. This export-led growth model has suppressed domestic demand and consumption, which means it’s not sucking in as many exports from the US and other Western countries as it otherwise would be.”

The problem isn’t globalization or trade integration—it’s that integration happened on an unlevel playing field. China spends an estimated 5% of GDP on industrial subsidies annually. The WTO was supposed to guarantee a level playing field. China didn’t play by those rules.

And importantly: China is showing no intention of pushing to raise consumption as a share of GDP. The structural imbalance persists.

Globalization as Convenient Scapegoat

Shearing notes that globalization has become a convenient scapegoat for deeper problems that require more thoughtful policy responses:

Skill-biased technological development — technology favoring skilled over unskilled workers, increasing returns to high earners

Labor market deregulation — 1970s/80s reforms that diminished union power

Weak productivity growth — particularly in Europe over the past 15 years

These created fertile ground for populists who promise that hemming off from trade and immigration will solve economic problems. It won’t—but the narrative persists.

THE BUFFER ZONES: WHO MIGHT STAY NEUTRAL

While most countries won’t get to choose neutrality, Shearing identifies a few potential buffer states:

Singapore: The Financial Bridgehead

“Singapore is the obvious bridgehead, financial bridgehead between the China bloc and the US bloc. If there’s going to be vast capital flows going between the two blocs and some trade happening between the blocs too, it’s got to go through somewhere. Singapore becomes an obvious financial bridge.”

Saudi Arabia: Security for Oil

The US is no longer dependent on Saudi oil, but wants Saudi in its defense/security orbit. The US “probably doesn’t mind Saudi sending vast amounts of oil to China, so long as it keeps Saudi in its defense, security, and technology orbit.” Saudi’s trade has already transformed: one-fifth of exports went to the US in 1990; now barely 2-4%, with a quarter going to China.

Commodity Producers Generally

Countries whose primary value is commodity supply—not strategic technology or manufacturing—may have more room to maneuver between blocs.

Potential Winners from Reorientation

Though the world as a whole loses, some countries benefit from supply chain reorientation:

Mexico — USMCA renegotiation likely to increase rules of origin requirements, benefiting Mexican producers

Vietnam — clear beneficiary of supply chain diversification from China

India — potential beneficiary, contingent on resolution of tariff issues around Russian oil purchases

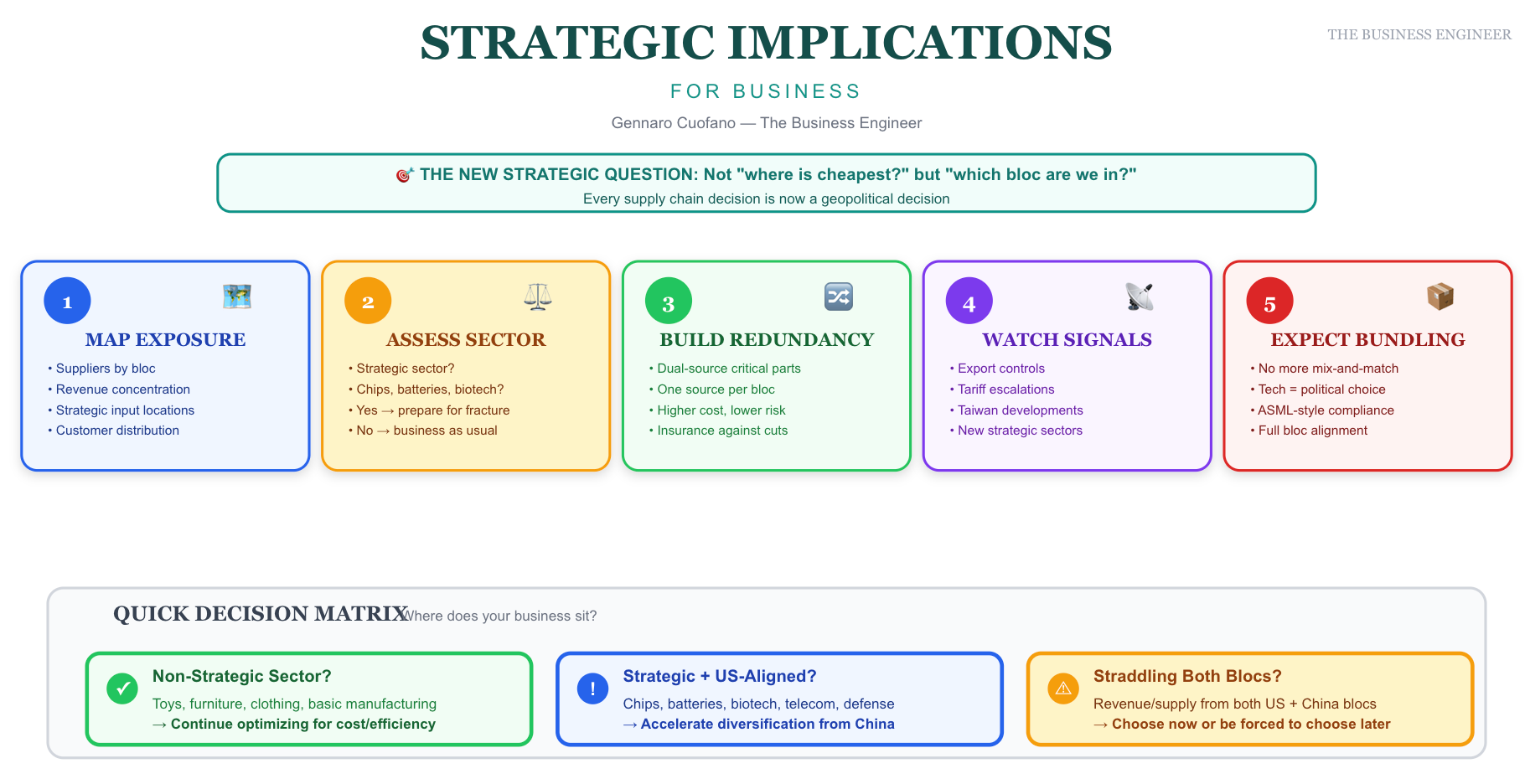

STRATEGIC IMPLICATIONS FOR BUSINESS

Capital Economics advises thousands of clients globally navigating these issues in real time. Shearing’s guidance distills to several core principles:

The Timing Principle: Start Now, Move Slowly

“If you do it relatively slowly over time—start taking steps now to shore up your supply chains and reduce single points of failure—it doesn’t embed that much cost. If you do it very quickly and you’re forced to do it very quickly, then it can become enormously disruptive and enormously costly. So the key point from a corporate perspective is to start taking steps now and to move slowly.”

The Strategic Sector Question

The critical question for any business: Are you operating in a sector that could be perceived to be geostrategically important?

This breaks into two sub-questions:

Are you in a strategic sector? (chips, biotech, dual-use goods, batteries, EVs)

Are you using geostrategically important inputs? (critical minerals, advanced semiconductors)

The implications for a toy manufacturer are “somewhat different” from those for a white goods manufacturer, which are “very different” from chips or biotech. Know where you sit on this spectrum.

The Dual Geography Problem

Businesses must think separately about:

Where is your final demand? (your customers, your markets)

Where are your inputs coming from? (suppliers, commodities, manufacturing)

These can be different. You can source commodities from China-aligned countries while serving US-bloc final demand. Your manufacturing plant might be in China even if you’re a Western firm. The fracturing risk depends on whether those flows cross strategic sector boundaries.

Winners and Losers at the Corporate Level

Winners: Those who take steps to plan for the fractured world early, now

Losers: Those forced to reorient very quickly in a short period of time, incurring greater costs

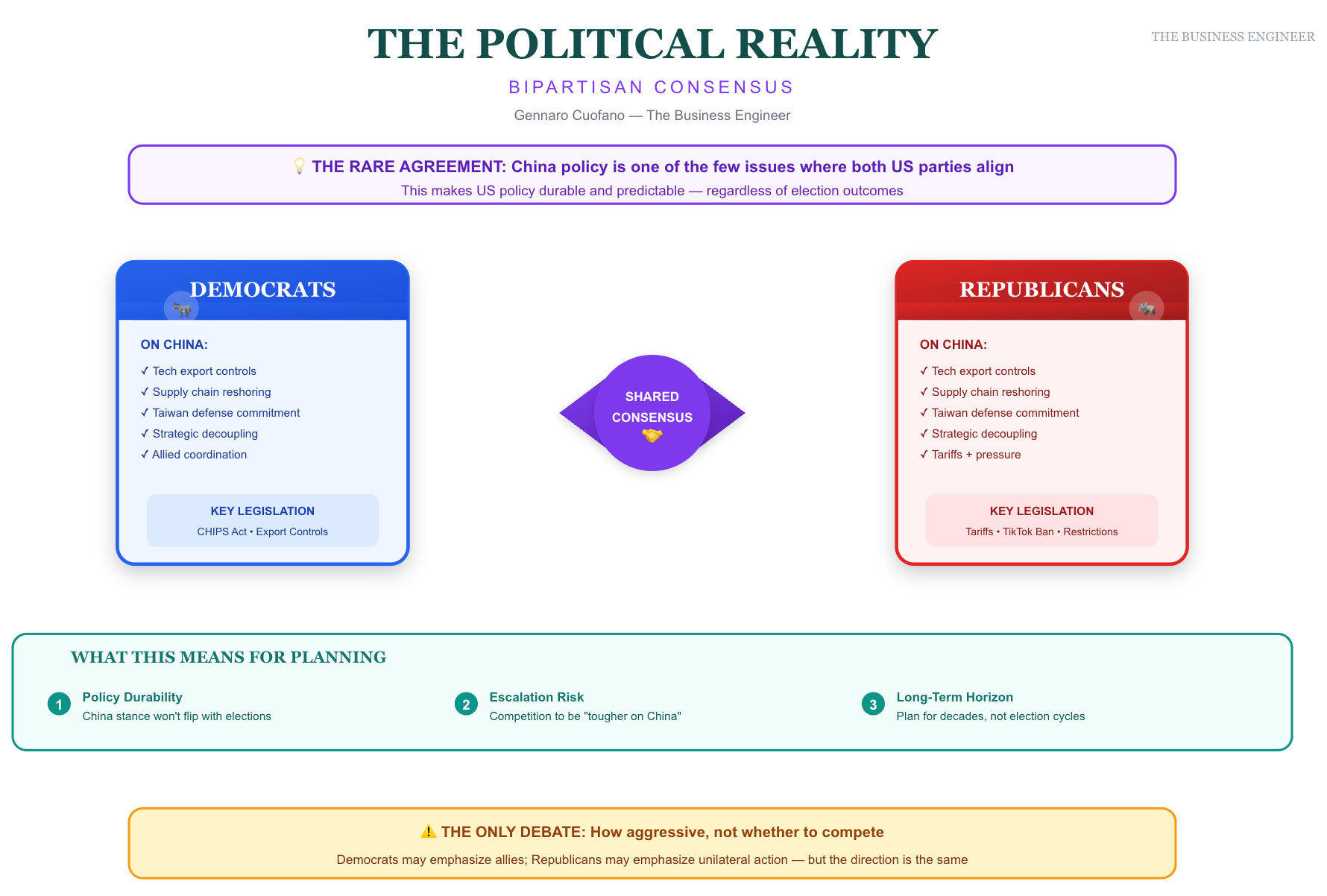

THE POLITICAL REALITY: BIPARTISAN CONSENSUS

A critical point for business planning: this is not a temporary policy that will reverse with the next election.

“If there’s one thing that unites an otherwise completely fragmented US political system, it’s the need to be strong and push back against China and Chinese competition. That’s the thing that motivates lawmakers and administration officials through the first Trump administration, then the Biden administration, and now the second Trump administration. And that cuts across economic competition, military competition, geostrategic competition.”

The evidence: tariff rates under Trump 2.0 remain differentiated by bloc alignment. UK at 10%, EU at 15%, China at over 30%. The structure follows the fracturing logic, not arbitrary protectionism.

China’s Own Decoupling Push

Importantly, fracturing is not unilateral. When NVIDIA was finally allowed to sell H20 chips to China, “China said, we don’t want those chips. We want to develop self-reliance, self-sufficiency in those areas.” There’s a push for decoupling from the China side, too.

China is no longer just “the workshop of the world” churning out toys and furniture. It’s “genuinely pushing the technological frontier” in batteries, EVs, some areas of pharmaceuticals, and biotech. In AI, the US lead is now measured in months, not decades. The race is real and both sides are running.

THE 30-50 YEAR FRAMEWORK

This is not a five-year disruption. It’s the mental model for the next several decades.

The hyper-globalization of 1989-2010 was historically unusual—a period when one superpower sought to reshape the world in its image, expecting that integrating China and Russia would make them “look and feel and act more American, more Western.” That clearly has not played out. Instead, China emerged as a strategic peer competitor.

The new equilibrium is not collapse. It’s controlled interdependence, selective cooperation, and permanent tension. Trade continues. Supply chains continue. Financial flows continue. But everything filters through a new logic:

Trust is political. Interdependence is strategic. Globalization is conditional.

The companies that thrive won’t be those waiting for normalization. They’ll be those who recognize this is the new normal.

The world is not shrinking. It is sorting. The question is whether you’re positioned to be sorted favorably.

Recap: In This Issue!

Globalization is not reversing; it is sorting along a US–China rivalry, producing selective disentanglement, not collapse.

Fracturing is strategic, sector-specific, and governed by bloc logic that bundles trade, tech, finance, and security.

The next 30–50 years are defined by controlled interdependence, not decoupling, with winners being firms that reorient supply chains early and deliberately.

Structured Narrative

Context: Narrative vs Data

Media narratives declared deglobalization in 2017–2018. Tariffs rose, politics hardened, and analogies to the 1930s proliferated.

But Capital Economics’ data showed continuity:

Trade/GDP ticked up.

Capital flows stayed high.

Migration persisted.

The shift was not volume but structure: a realignment driven by superpower rivalry.

Core move: The world isn’t withdrawing; it’s reorganizing around strategic fault lines.

Transformation: Selective Disentanglement

Disentanglement happens only in strategically sensitive sectors.

Evidence: The Smartphone Supply Chain

China’s share of US mobile phone imports: 65 percent → 20 percent (2000 to today).

India became the largest supplier as Apple diversified iPhone production.

This is fracturing by design — security-driven, not cost-driven.

What fractures vs what flows

Will fracture: chips, batteries, EVs, AI, telecoms, biotech, rare earths, drones.

Will continue: toys, clothing, furniture, basic consumer goods.

This selective pattern is the defining mechanism of the fractured world.

Mechanisms: Bloc Structure and Power Asymmetry

Capital Economics’ five-tier bloc map:

Strong US ally

Lean US

Unaligned (very few stay here)

Lean China

Strong China ally

Power Asymmetry

Population: US bloc ~50 percent, China bloc ~50 percent.

GDP: US bloc ~66 percent, China bloc ~25 percent.

The economic center of gravity remains firmly in the US camp. This is the structural advantage the US leverages; China’s bloc is commodity-heavy and strategically thin.

Key dynamic: Everyone wants neutrality. Very few get it. The US and China set the boundaries.

Rebundling: The End of Hedging

Hyper-globalization allowed mix-and-match alignment: US military, Chinese factories, European finance.

Today, alignment in one dimension increasingly locks you into the bloc package:

ASML can’t sell advanced lithography to China because tech ties follow defense ties.

Countries can’t split security and technology choices anymore.

Hedging is dying. Bundling is back.

Currency Power: Why the Dollar Deepens

China’s huge surplus forces capital back into dollar markets:

$9 trillion external assets

$1 trillion annual trade surplus

There is no alternative asset pool deep and liquid enough.

Shearing’s judgment: RMB internationalization remains a distant prospect until China reforms consumption, institutions, capital controls, and banking — a multi-decade agenda China has no clear plan to execute.

China’s Real Issue: Imports, Not Exports

China’s export dominance is not the distortion; it’s under-importing because domestic consumption is suppressed.

China spends ~5 percent of GDP on industrial subsidies.

Integration happened on an unlevel playing field.

The West blamed globalization instead of:

Skill-biased tech shifts

Labor market deregulation

Weak productivity trends

These internal failures opened the door to populist anti-trade narratives.

Buffer Zones: Who Stays Neutral

Very few, but some can:

Singapore: the bridgehead for capital flows between blocs.

Saudi Arabia: tight US security alignment; energy flows to China are tolerated.

Commodity exporters: more freedom due to non-strategic output.

Winners from reorientation: Mexico, Vietnam, India (conditional).

Corporate Implications: Strategies for the Fractured Age

1. Move early, move slowly

Early diversification is low-cost. Forced diversification is massively expensive.

2. Ask the strategic-sector question

Are you in a strategic sector or do you depend on strategic inputs?

The risk profile differs dramatically between toys, white goods, chips, or biotech.

3. Solve the Dual Geography problem

Separate:

Where you sell

Where you source

Fracturing risk appears where sensitive inputs cross bloc boundaries.

4. Winners vs losers

Winners: firms that adapt supply chains deliberately.

Losers: firms that wait and are forced to pivot suddenly.

Political Reality: Durable Bipartisan Consensus

US–China competition is the only durable bipartisan alignment in US politics.

Tariffs differ by bloc alignment:

UK ~10 percent

EU ~15 percent

China ~30+ percent

The structure maps to fracturing, not protectionism.

China is also choosing decoupling in strategic tech domains, not merely reacting to the US.

The 30–50 Year Frame

Hyper-globalization was an exceptional window (1989–2010).

The new worldview: controlled interdependence — steady trade, but politically filtered and strategically constrained.

Principles of the new era:

Trust is political.

Interdependence is a strategic choice.

Globalization is conditional and sortable.

Firms that treat this as temporary will lose. Firms that accept it as the baseline will win.

Key Takes

Globalization persists but fractures along strategic US–China lines.

Disentanglement is selective, concentrated in tech, energy transition, and dual-use sectors.

The world is reorganizing into two blocs with asymmetric economic power.

The dollar remains entrenched because China must recycle surpluses through US assets.

For business: start supply-chain reorientation now, slowly, while evaluating strategic exposure.

The next era is controlled interdependence, not decoupling. The world is not shrinking — it is sorting.

With Massive ♥️ Gennaro, The Business Engineer