There is a moment in every major technology wave when the debate stops being about whether the demand is real and starts being about whether the underlying system can actually carry that demand. The AI Supercycle is happening right now.

This is part of The AI Supercycle Series. You will find the curated version of the live in the AI supercycle in the coming days.

That was the through-line of our latest AI Supercycle session with William from the Exponential View team, whose State of the AI Economy report is one of the most rigorous attempts I’ve seen to answer, at the level of financial mechanics rather than vibes, one deceptively simple question:

Where is the money in AI actually coming from — and is any of it real?

Their answer, stripped to the bone: demand is real, it is bigger than most narratives give it credit for, and it is arriving faster than any prior tech wave. But how that demand is being funded, absorbed, and priced is where the interesting structural story lives.

Here is the compressed version of the conversation — what it means, and why it matters if you’re trying to make sense of this cycle for the next decade, not the next quarter.

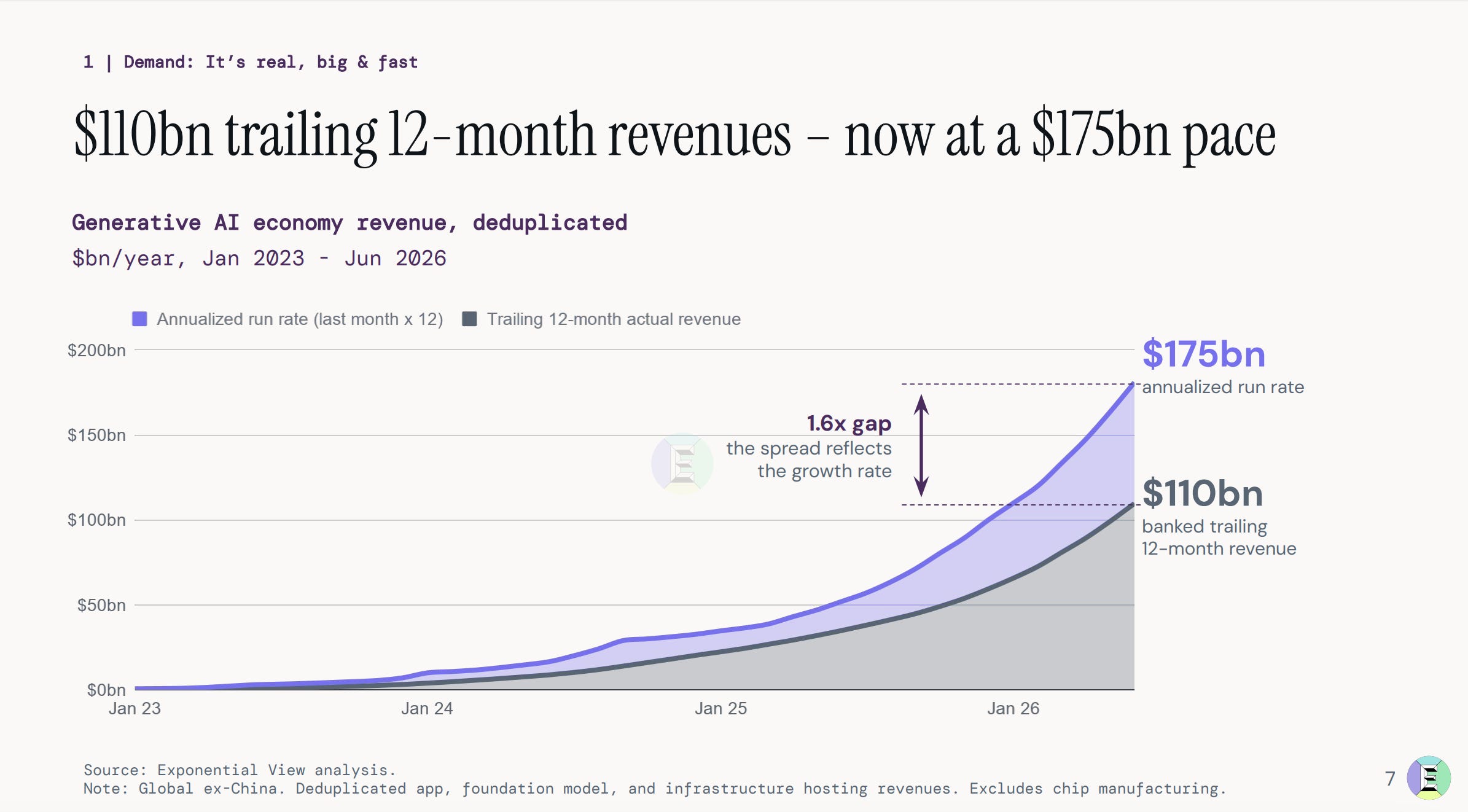

The deduplication problem — and why “$110B in revenue” is actually an honest number

The first thing Exponential View did — and it is the reason their report is worth reading in full — is refuse to accept the industry’s own accounting at face value.

The AI stack has a circularity problem. A Cursor or a Harvey generates revenue from an end user, then spends most of it on tokens from OpenAI or Anthropic. Those labs generate revenue, then spend it on compute from hyperscalers and NeoClouds. Those hyperscalers and NeoClouds generate revenue, then spend it on chips from NVIDIA. Each transaction shows up on someone’s income statement. If you naively stack them, you double- and triple-count the same underlying dollar as it flows down the stack.

Exponential View built bottom-up financial models — P&Ls and cash flow statements — for every major player in the stack, and every meaningful minor one. They then deduplicated the revenues across layers to isolate genuine external demand from internal recycling.

The number that survives that filter: ~$110B of real AI revenue in the last 12 months, now trending toward $175–200B on current momentum.

Why this matters: the loudest critique of the AI economy — “it’s all circular, they’re just paying each other” — is the exact critique this methodology was designed to test. It doesn’t fully vanish. But it turns out to be a much smaller share of the whole than the critics assume, and the residual, deduplicated demand is very large and growing very fast.

The Compression: The bear case that “AI revenue is just financing dressed up as demand” survives contact with the data only in a much narrower form than it’s usually stated.

Nobody in this stack is a static actor

The most useful mental model I took from William’s analysis is this:

Every layer of the AI stack is trying to eat the layer above it and the layer below it — simultaneously.

Foundation model labs are moving up into applications. Claude Code and Codex are direct assaults on Cursor and the coding-assistant category. Anthropic has now shipped Claude for Teacher into education. OpenAI is pushing into legal, finance, and productivity verticals. These are not accidents. They are structural responses.

Meanwhile, the application layer is moving down toward the frontier. The Cursor–xAI deal is the canonical example. Cursor became the largest Anthropic API customer, then found itself directly competing with Claude Code. The path forward wasn’t to sit still — it was to acquire compute (through the xAI/SpaceX deal), leverage the enormous corpus of agentic traces from Cursor’s own users as post-training signal, and push a Cursor-native frontier model (Composer) into production. That is vertical integration under duress. And it works because the harness — the agentic scaffolding around the raw model — has become nearly as important as the model weights themselves.

This is the pattern to watch in every boardroom right now: do we tie ourselves to a hyperscaler and a lab, or do we vertically integrate? Apple tried the closed path and reversed itself. AWS launched Bedrock. Almost every serious operator is running this calculation in Q4 2026.

The Compression: In the AI Supercycle, no one accepts their assigned layer. Every player is negotiating vertical integration or being negotiated into it.

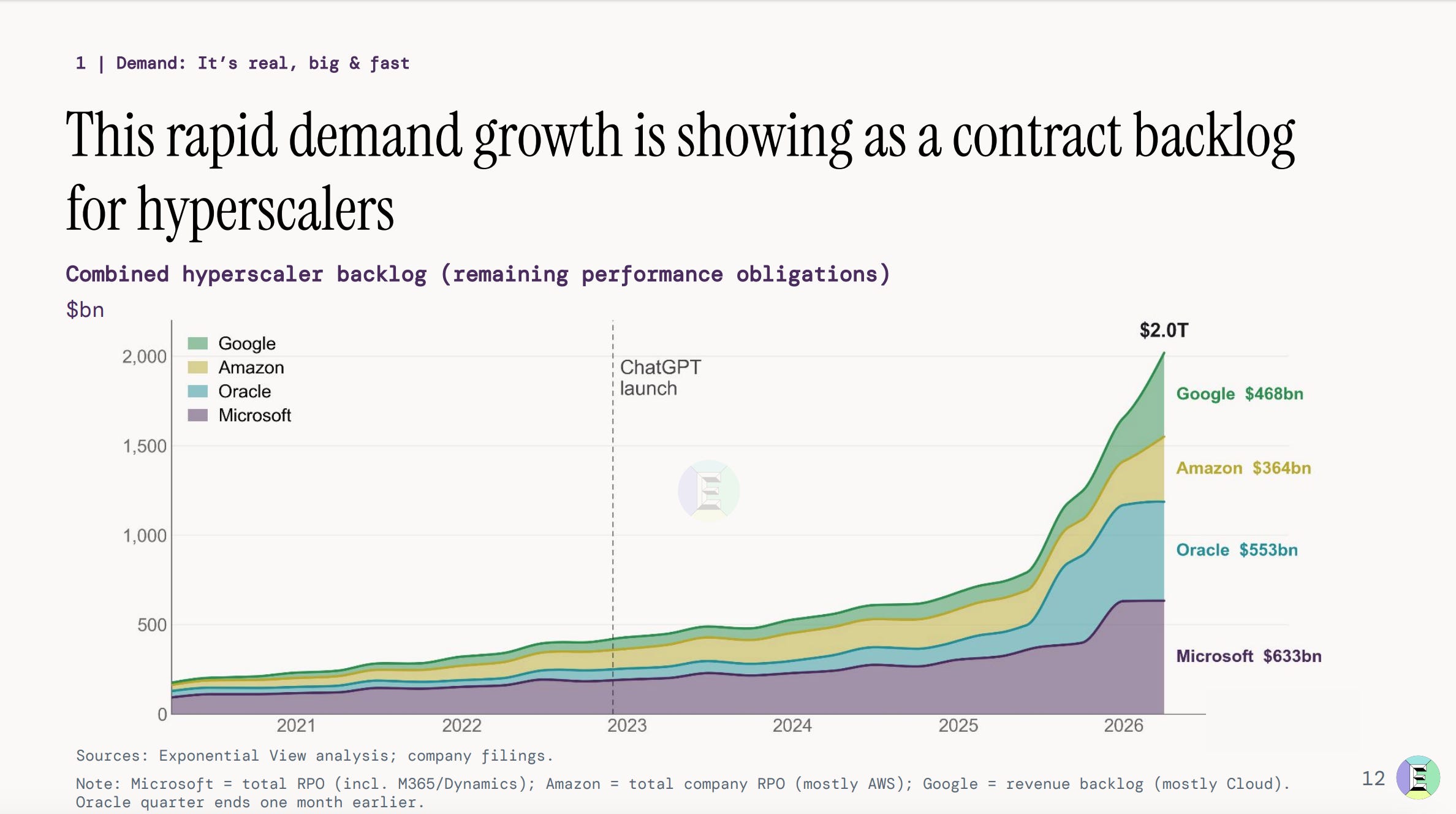

CapEx, depreciation, and busting the “hyperscalers are just lighting money on fire” narrative

The day before we recorded, TSMC announced another ~$260B in capacity commitments. Every week the CapEx numbers move. And every week the same critique returns: “these companies are spending more than they earn — it’s a bubble.”

William’s response is the most honest reframing of the CapEx question I’ve heard:

CapEx is a stock, not a flow. When Microsoft or Meta commits $80B this year to AI infrastructure, they are not expected to earn that back this year. They are building an asset with a depreciation schedule — roughly 6 years for chips, 14 years for the rest of the data center envelope (building, cooling, power). Each year, only a fraction of that spend passes through the income statement as a cost. But that fraction accumulates on top of every prior year’s fraction. That is the payback pressure that matters — not the headline number.

Similarly, Remaining Performance Obligations and forward energy commitments are the market pricing in future demand. They look terrifying next to today’s revenue precisely because they are not meant to be compared to today’s revenue.

The deduplicated-revenue methodology is what lets you actually answer the question everyone is really asking, which is not “is the CapEx big?” (it obviously is), but rather:

Is the accumulated depreciation stack going to be paid back by the real, external demand — and on what timeline?

That question has a more nuanced answer than either the bulls or the bears usually want to admit.

The Compression: You cannot judge the AI CapEx cycle by comparing this year’s spend to this year’s revenue. You have to compare the depreciation waterfall to the demand trajectory.

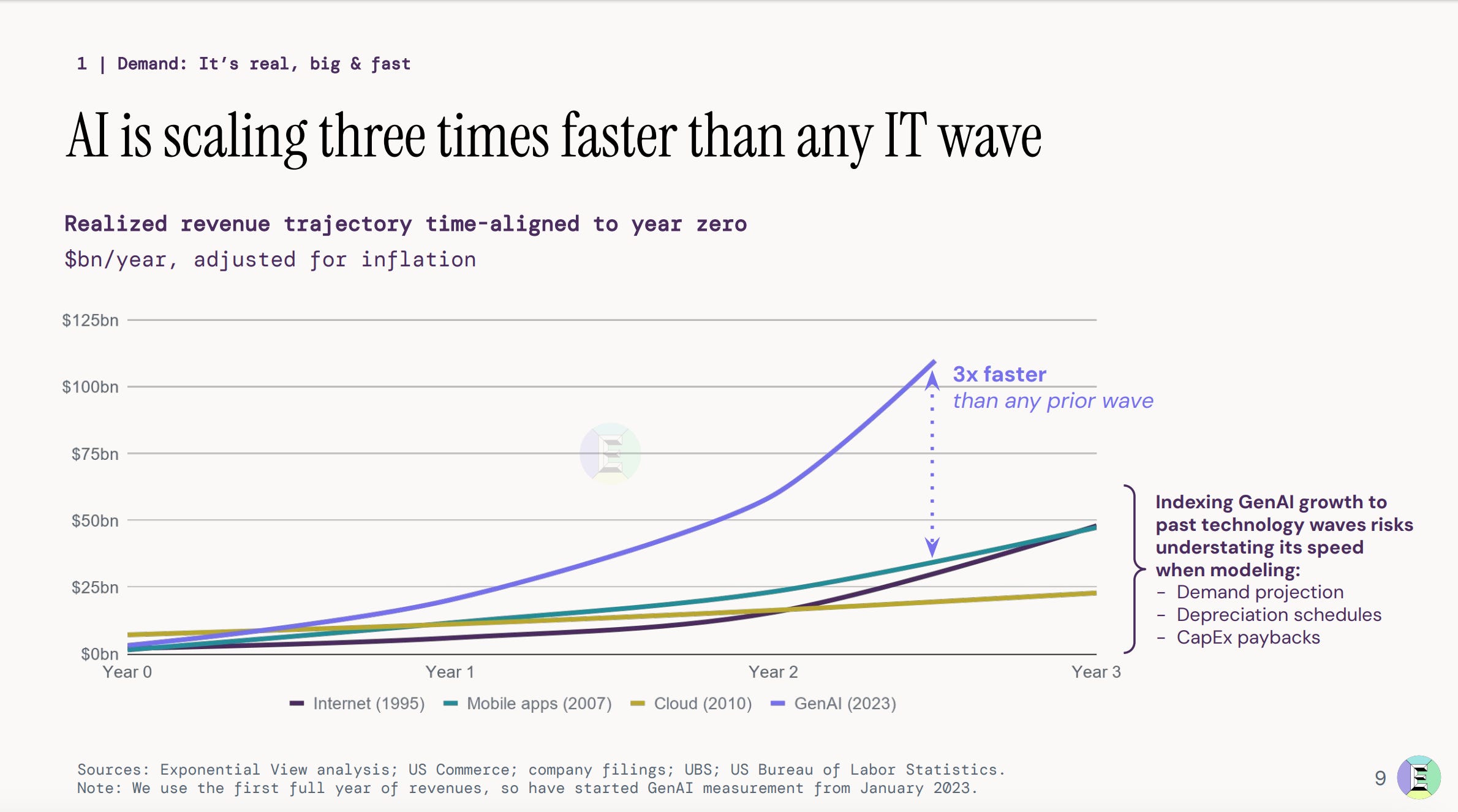

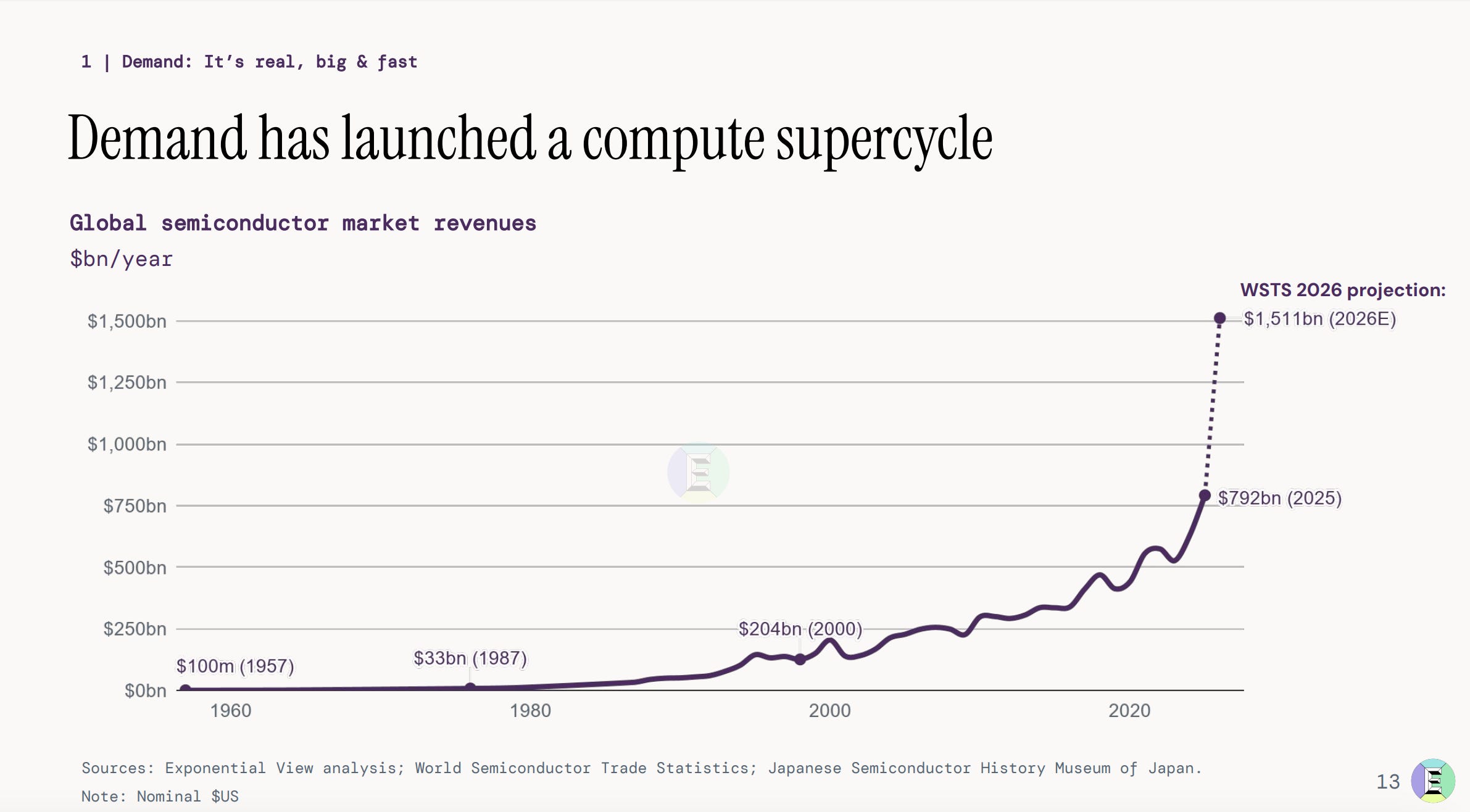

Why this wave grew faster than any prior wave — and why that changes everything

One of the most important slides in the report is the one that plots AI investment and revenue against the internet, mobile, and cloud waves.

AI has grown much, much faster than any of them. That is not a qualitative claim — it is a measurement.

The reason is not primarily that AI is a “better” technology than the internet. The internet was arguably more foundational. The reason is compounding: AI is arriving in a world that already has the internet, mobile, cloud, ubiquitous payments, mature distribution, and instant global software delivery. Every prior wave is now infrastructure for this one. What took the internet a decade to distribute takes a foundation model six months.

This changes everything downstream, but the most under-discussed consequence is societal: we and our institutions had roughly ten years to make sense of the internet before it reshaped work, media, politics, and family life. We are being given twelve to twenty-four months for AI. Our institutions were caught off guard by the internet even at its slower pace. With generative AI, that adjustment gap is going to be far more violent.

If you are still using “the .com bubble” as your reference model for this cycle, you are underestimating both the upside and the systemic pressure.

The Compression: AI compounds on top of every prior tech wave. That is why the revenue curve is faster, and also why the societal adjustment is harder.

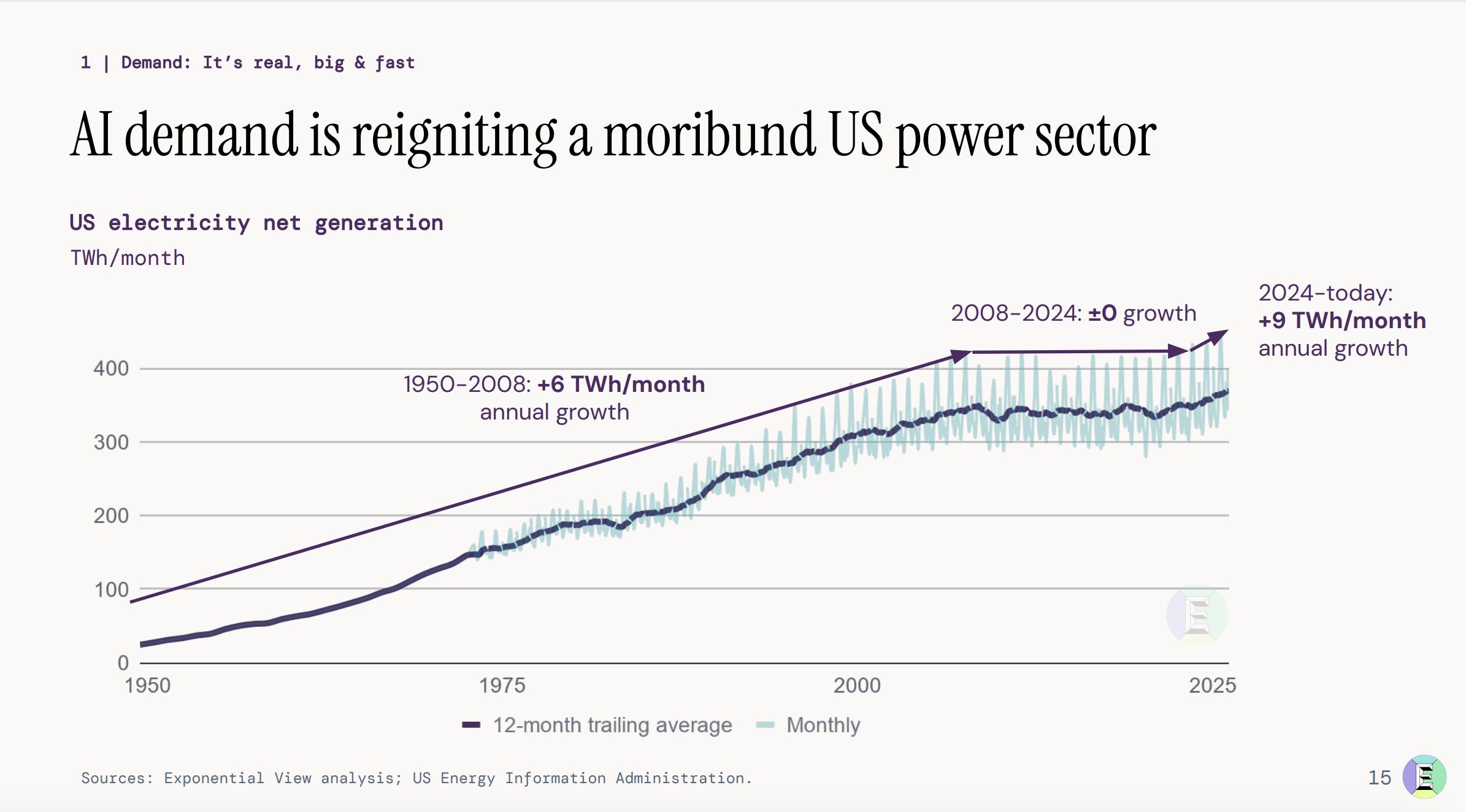

The bottleneck cascade — energy, chips, capital

The rapid demand growth doesn’t just show up as revenue. It shows up as bottlenecks, which is the word the industry keeps involuntarily returning to.

Chips: the semiconductor industry is deeply cyclical, used to peak-and-trough dynamics. AI demand is not one of those cycles. It is an order of magnitude larger and structurally exogenous to the industry’s own cycle. This is why TSMC keeps revising up.

Energy: the US power sector plateaued for years. It is now the binding constraint on data center deployment, and grid planning has to be done for a future state, not a present one.

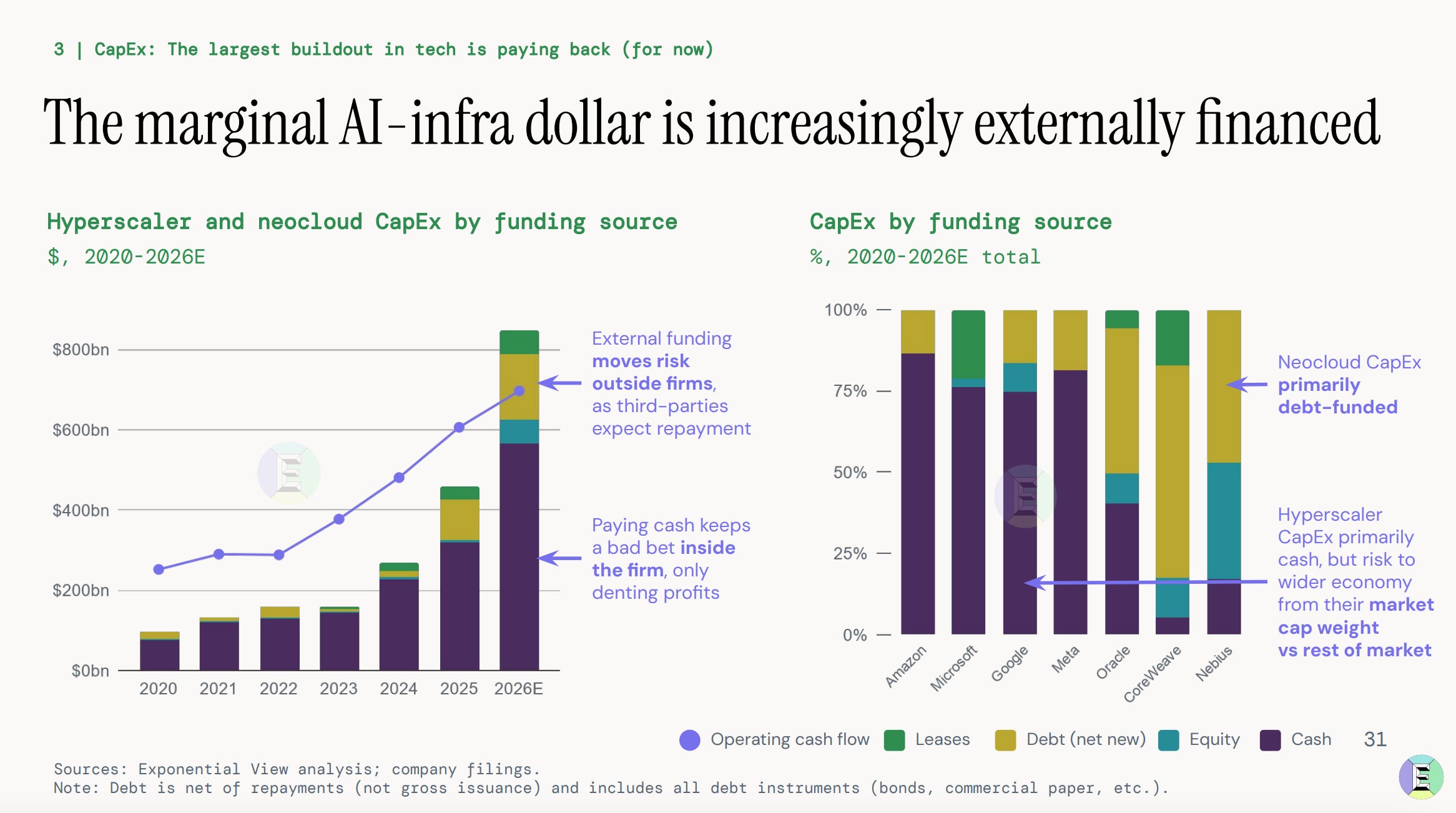

Capital: this is the one people underestimate most. In 2022–2024, hyperscaler CapEx was overwhelmingly funded from existing cash. Hyperscalers are cash-rich. But the pace of growth has now outrun internal cash generation. External capital is filling the gap.

That last point deserves its own section, because it is where systemic risk actually enters the picture.

The financing shift — and the NeoCloud SPV problem

When AI CapEx was being funded out of hyperscaler cash flow, an underperformance risk was contained: the share price of a specific company might take a hit, but the wider market was insulated.

External capital changes the picture. Debt, private credit, and — most interestingly — Special Purpose Vehicles at the NeoCloud layer are doing an increasing share of the funding. The NeoCloud business model was designed precisely for this: gather capital in an SPV, buy the GPUs, hold them off the primary hyperscaler’s balance sheet, and rent capacity back.

From Microsoft’s perspective, it would be nearly irrational not to use this structure to add compute right now. From the system’s perspective, it means CapEx risk is being pushed off the balance sheets of the strongest players and into a more distributed set of counterparties.

This is fine while demand keeps compounding. It is where the interconnectivity risk lives if any part of the cascade slows.

The Compression: The AI CapEx race has moved from cash-funded to externally-funded, which means the systemic interconnectivity of the industry is materially higher than it was 18 months ago.

Why the bubble, if it pops, won’t pop the way the .com bubble did

I’ve been saying this for a while and William’s data reinforced it: the mental model of “one big bubble that inflates and pops” is wrong for this cycle.

The reason is the same reason we call it a Supercycle. This isn’t a single S-curve. It is a stack of overlapping S-curves — chips, energy, models, applications, agents, verticals — each with its own bottleneck, its own capital demand, and its own timeline.

What happens instead is a sequence of smaller, localized re-pricings. Supply catches up to demand in one layer, prices collapse in that layer, capital rotates. Then demand pushes into the next bottleneck. The system as a whole keeps growing, but individual layers experience cyclical pain that looks like a bubble popping in miniature.

If you are pattern-matching to 2000 or 2008, you will misread the next five years.

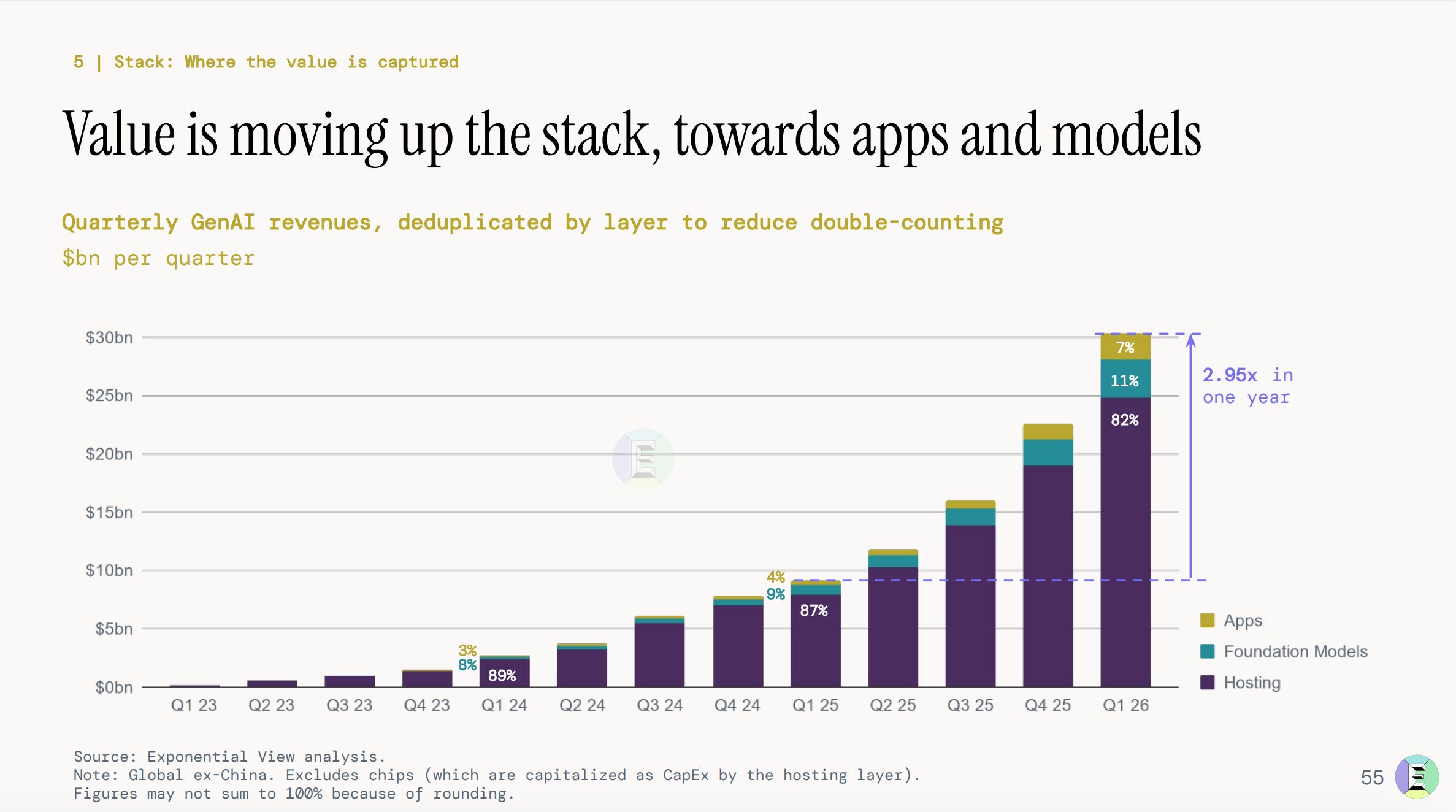

Value is moving up the stack — finally

For the last three years, “who is making money in AI?” had one answer: NVIDIA, then memory (SK Hynix, Samsung), then the labs. The application layer was widely dismissed as “just ChatGPT wrappers” — thin margin on top of a commoditized token spend, no defensible value add.

That is changing, and William’s data captures it. What people pay for Cursor is not a pass-through of their token spend. It is not a subsidy on their token spend either. It is a premium on their token spend. That premium is the app layer starting to earn genuine margin — because customers are getting savvier, because the product surface around the model matters more than people realized, and because the harness (context, memory, tools, agentic scaffolding) is where a lot of the actual utility lives.

This is what value migration up the stack looks like in real time. It is exactly what the .com era did with its own layers over ten years. This one will do it faster.

The precondition is competition strong enough to prevent any single app-layer player from setting pricing power. That competition exists.

The Compression: We are at the transition point where the app layer stops being wrappers and starts being defensible products with real margin.

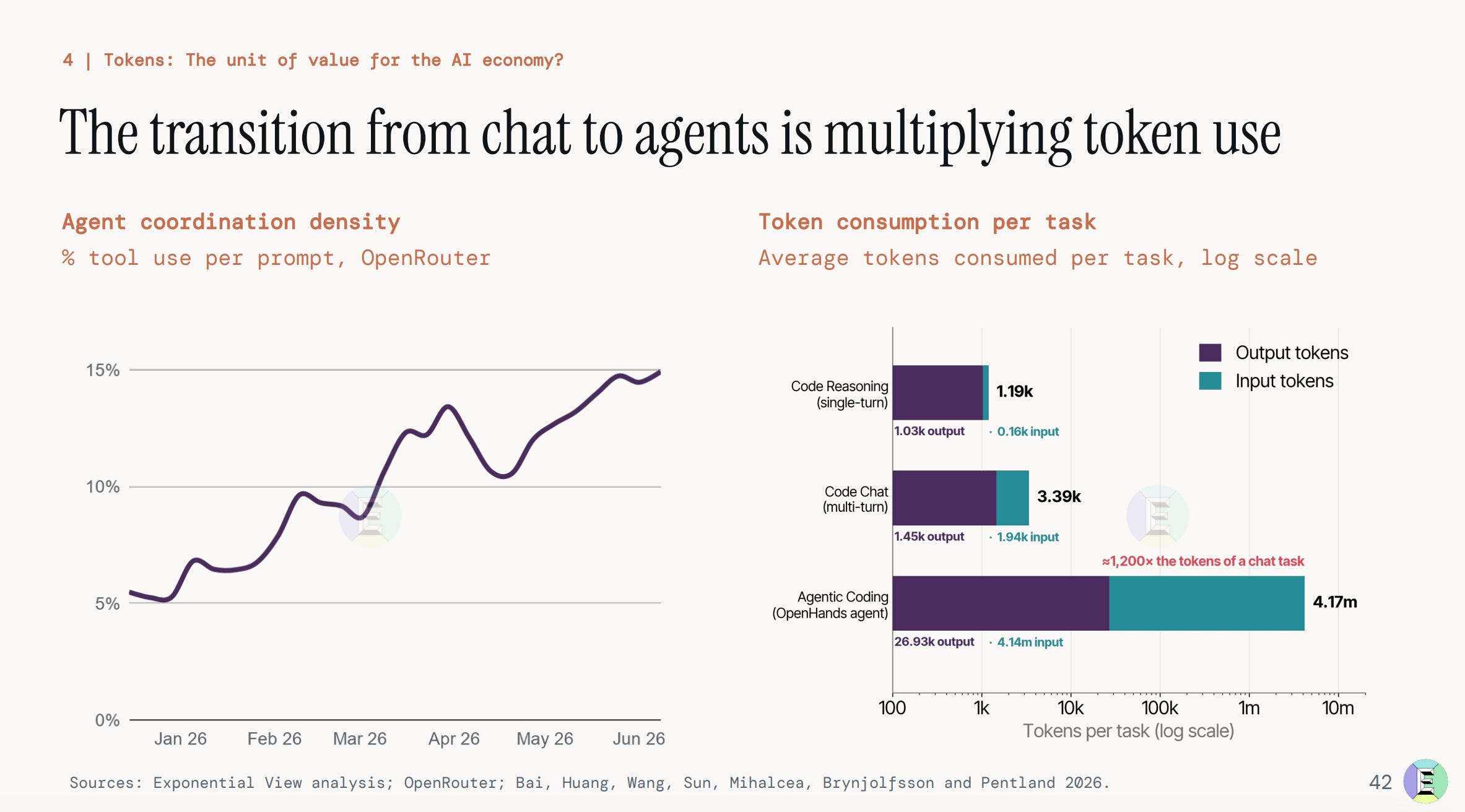

The Jevons paradox is already showing up in the token data

Token consumption has grown in a compounding fashion. Some of that is adoption — more users, more use cases. But a large share is the new modes of use: multi-turn chat, reasoning, and above all agentic execution, which drives massive tool-use per prompt.

Exponential View is tracking agentic intensity as a proxy — the extent to which individual prompts result in tool calls. It is ticking up. Cheaper tokens are not reducing token consumption. They are enabling entirely new workflows that consume vastly more tokens per user session.

The methodological innovation worth flagging: William’s team proposes measuring quality-adjusted output tokens — strip out input and reasoning tokens, weight the remaining output tokens by the benchmark quality of the model that produced them. This is a much better proxy for real user value than raw token counts, and it removes the artificial inflation from models spending more time reasoning.

Expect that to become a standard metric.

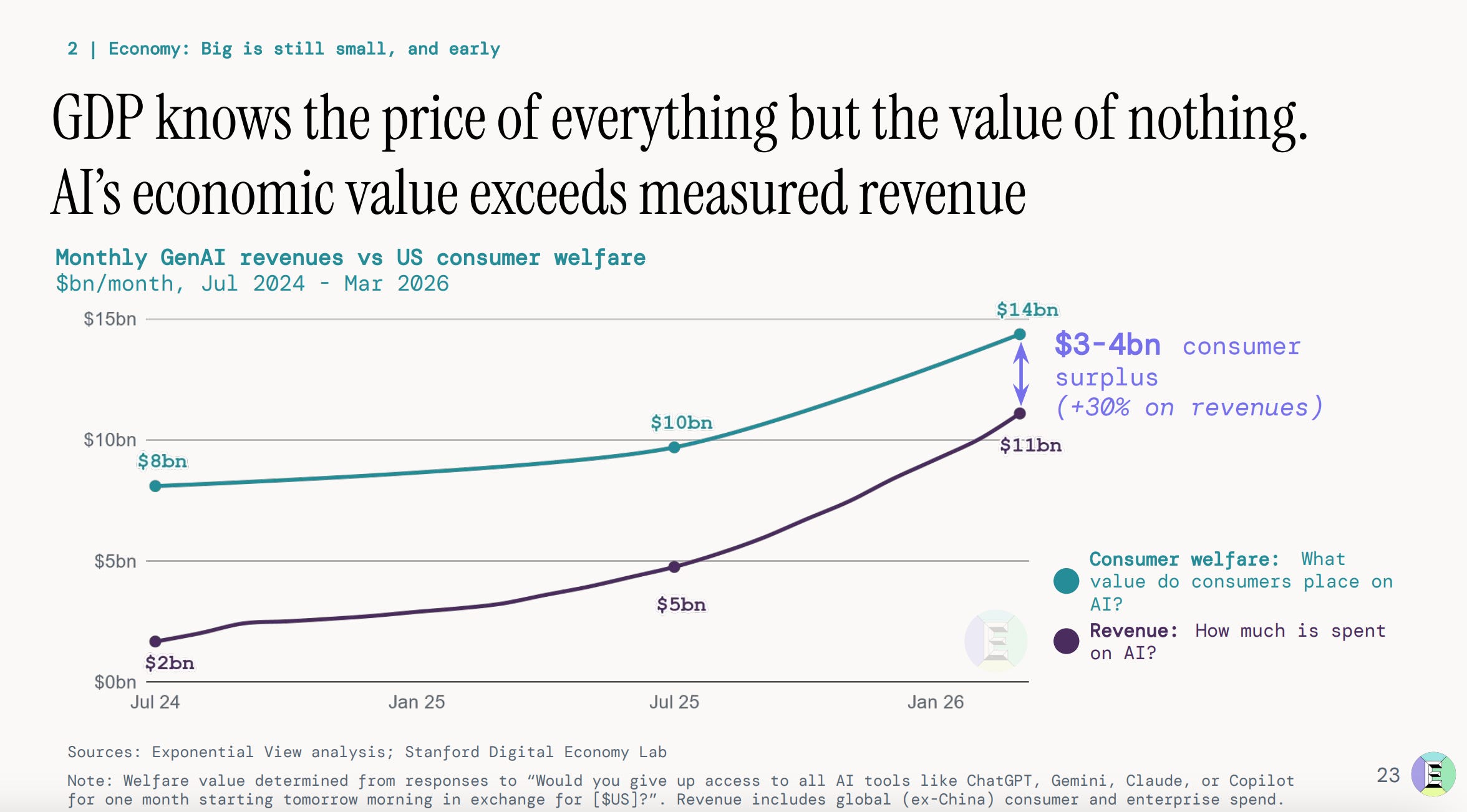

The consumer surplus story that gets left out of every earnings call

The most important reframing of the entire conversation came near the end.

Almost every AI economy debate is about revenue — will it pay back CapEx, will it pay back VC, will it justify the valuations. Almost no one talks about consumer surplus — the value users are extracting from these tools that isn’t captured in anyone’s revenue line.

Erik Brynjolfsson’s Stanford team has been running the “how much would you need to be paid to give up your access to AI?” study — the same methodology used to value Google Maps and other free internet goods. The consumer surplus is enormous. It doesn’t show up in GDP. It certainly doesn’t show up in the revenue models.

The Google Maps analogy is exact: the paper A-to-Z road atlas added to GDP when you bought it. When it was replaced by a vastly better product that people got for free, the GDP contribution went to zero. The world got better. The measurement got worse.

The same thing is happening now, at scale, in real time. Even if the AI CapEx race under-earns for its funders, the value being delivered to users — in their work and in their lives — is real and permanent. There is no going back. Every knowledge worker who has adopted these tools knows this in their bones.

The Compression: A growing generative AI economy is not automatically good news for OpenAI, Anthropic, or the hyperscalers. But it is unambiguously good news for consumers — and that value doesn’t reverse.

What to take home

If you read only one section of the State of the AI Economy, read the deduplicated revenue methodology and the CapEx depreciation waterfall. Those two pieces together are what separate serious analysis of this cycle from the noise on both sides.

The one-line synthesis from William that I’ll be quoting for a while:

“This economy is growing from consumer demand. We can see that unprecedented revenue growth, and there are really quite significant balancing acts where CapEx and the depreciation hurdle meet the pressure of selling tokens at continually collapsing prices for a given intelligence level. All of those competing dynamics make this a much more finely balanced economy — even though the overall consumer benefit continues to grow apace.”

That is the shape of the AI Supercycle in one sentence. Balanced tension all the way down the stack. Real demand. Real payback pressure. Collapsing unit prices. Growing consumer value. And nobody sitting still.

Report: The State of the AI Economy, by Exponential View. Guest: William, Exponential View team.

Hosts: Gennaro (The Business Engineer) and Joel (Leadership in Change).

With massive ♥️ Gennaro Cuofano, The Business Engineer