The Topology of The AI Supercycle

The Master Framework

Over the years, my research on The Business Engineer has turned into the AI Supercycle.

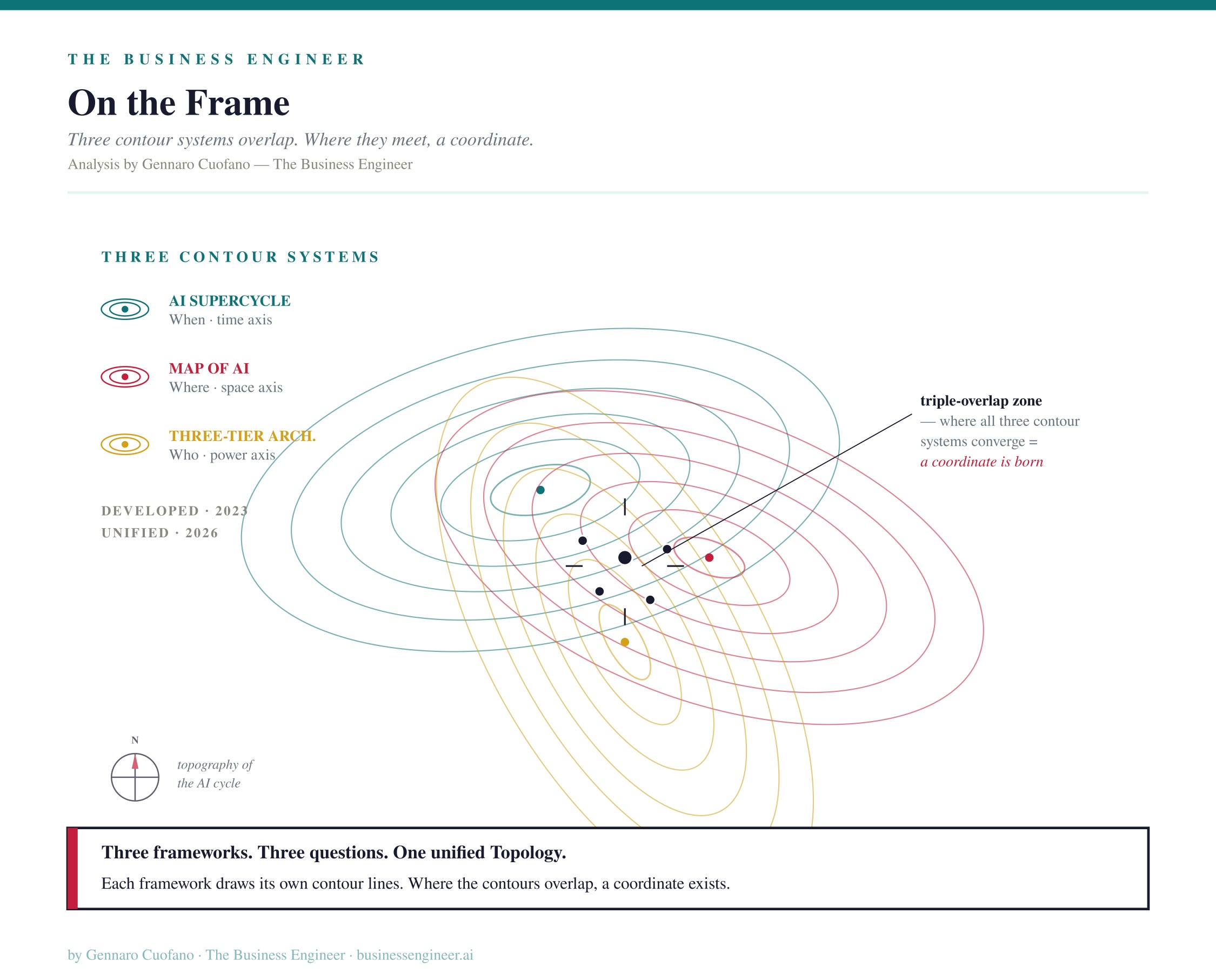

Then, a few years ago, in early 2023, three frameworks began taking shape in parallel to make sense of what the AI cycle actually was. The frameworks were developed separately because each was answering a different question, and the questions did not initially appear related.

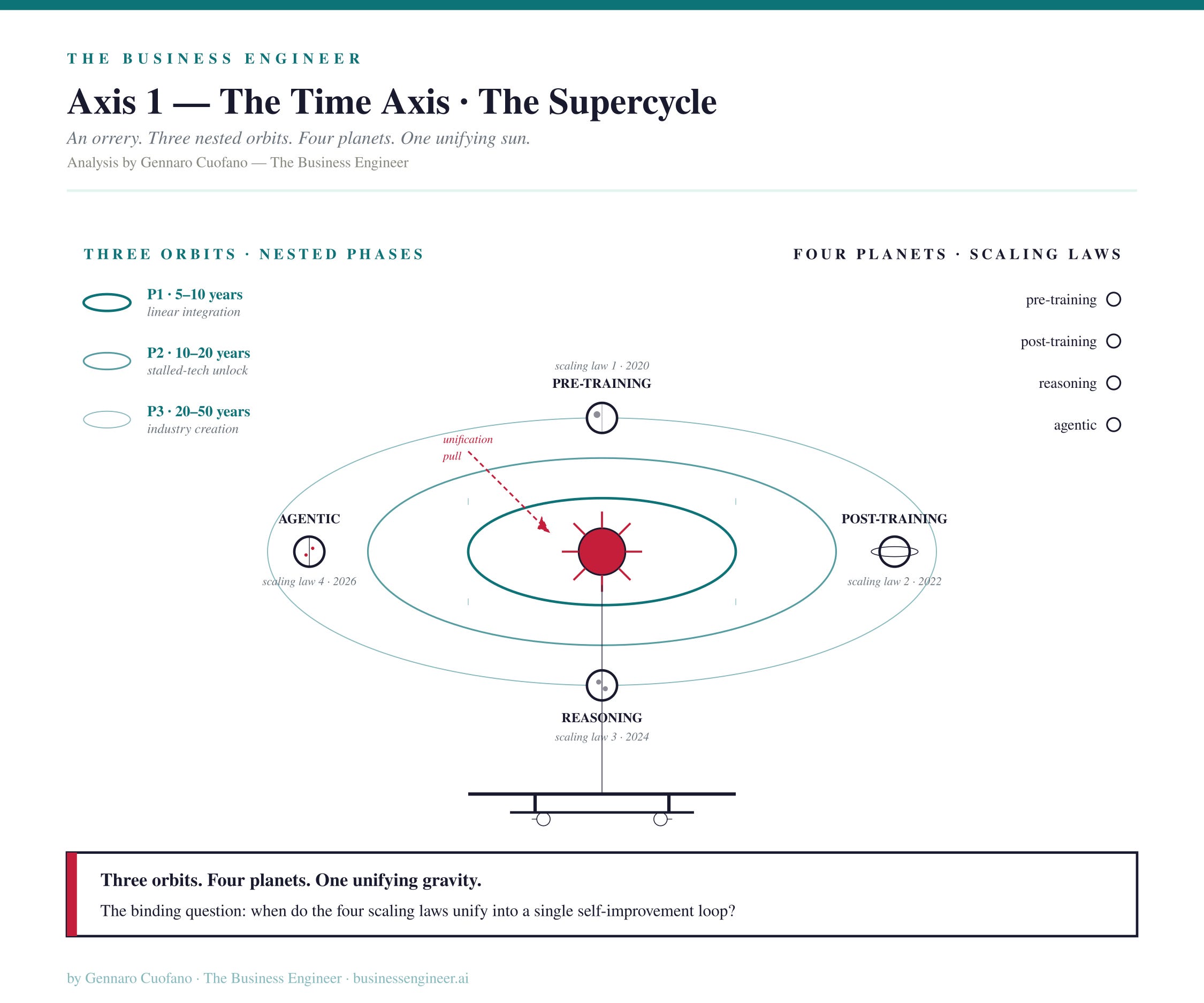

The AI Supercycle asked when: when does a foundational technology like AI become commercially generative, through what phases, and over what time horizon. The answer was a 30-50 year paradigm shift unfolding through three nested cycles, with linear integration into existing industries first, the unlocking of stalled technologies second, and the creation of industries we cannot yet name third.

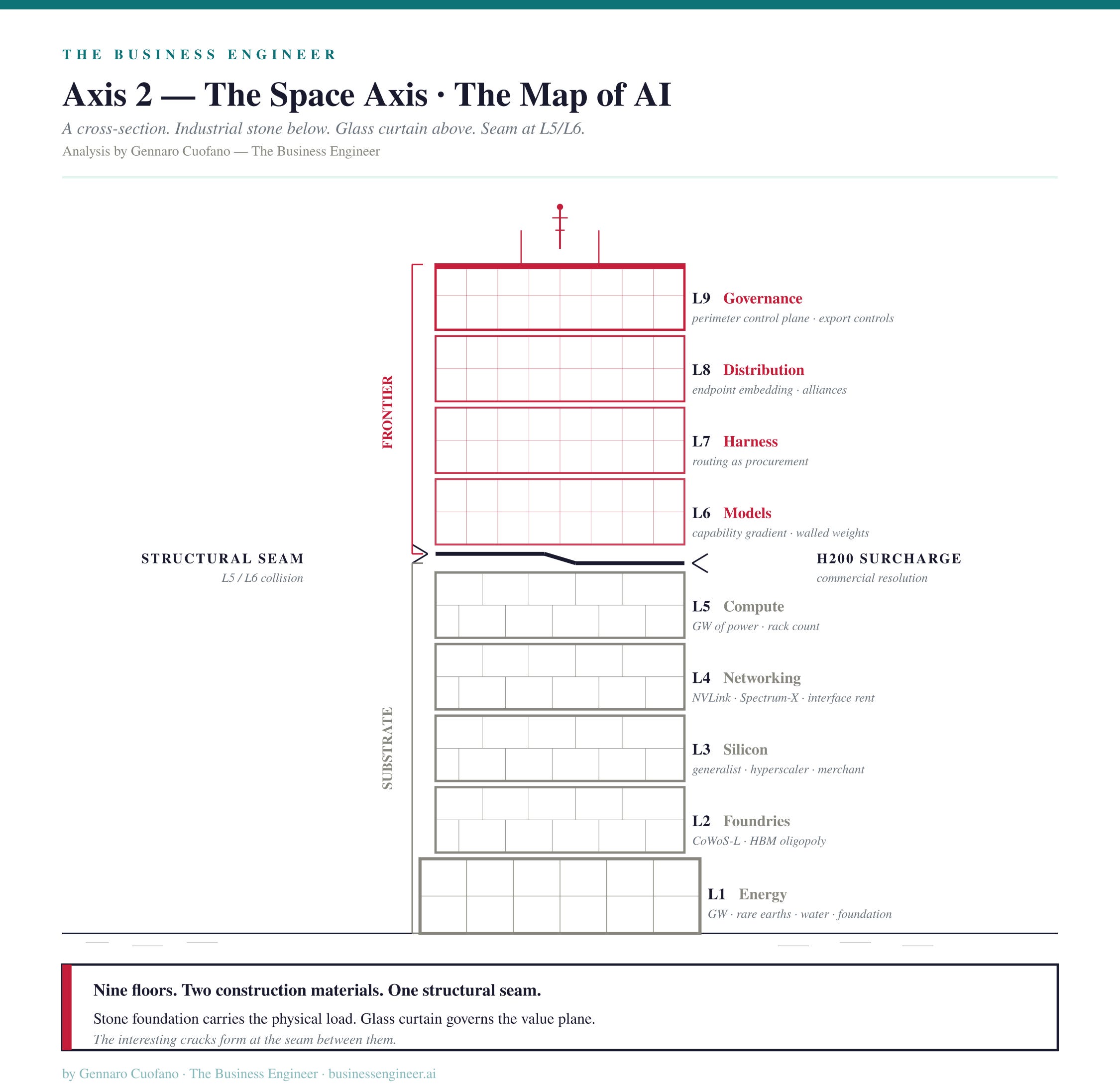

The Map of AI asked where: where in the architectural stack does value accumulate, where do binding constraints live, where does rent get captured. The answer evolved from a three-layer reading into the current nine-layer structure, with each layer constrained by the layer below it and commercialized by the layer above it.

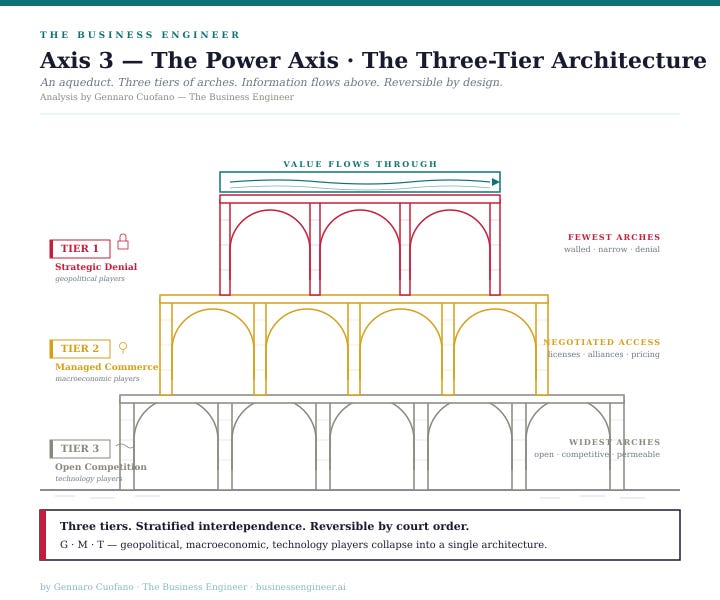

The Three-Tier Architecture of Stratified Interdependence asked who: who is allowed to operate at any given layer, under what political and commercial terms, with what restraint embedded in the access regime. The answer integrated geopolitical players (states, alliances, multilateral control regimes), macroeconomic players (capital markets pricing the tier system into valuations and procurement), and technology players (companies designing their architectures around tier boundaries).

Three frameworks. Three questions. Three years of refinement. The unification is now overdue.

The unified object is best named for what it actually is: a topology. A structure on a set of coordinates that defines which positions are close to which others, how the structure transforms under continuous deformation, and which properties persist through transformation. The diagonal of dominance is a topological feature. The nine-layer architecture is a topological invariant. The tier system is not — it deforms in quarters, not decades. The defects are coordinates where the structure has localized anomalies that produce novel commercial properties. Cascades are deformation events propagating through the structure.

The Topology is rugged. It is reversible by design. And the most strategically interesting action lives where the three axes pull against each other.

On the Spine — The Dual Analogy

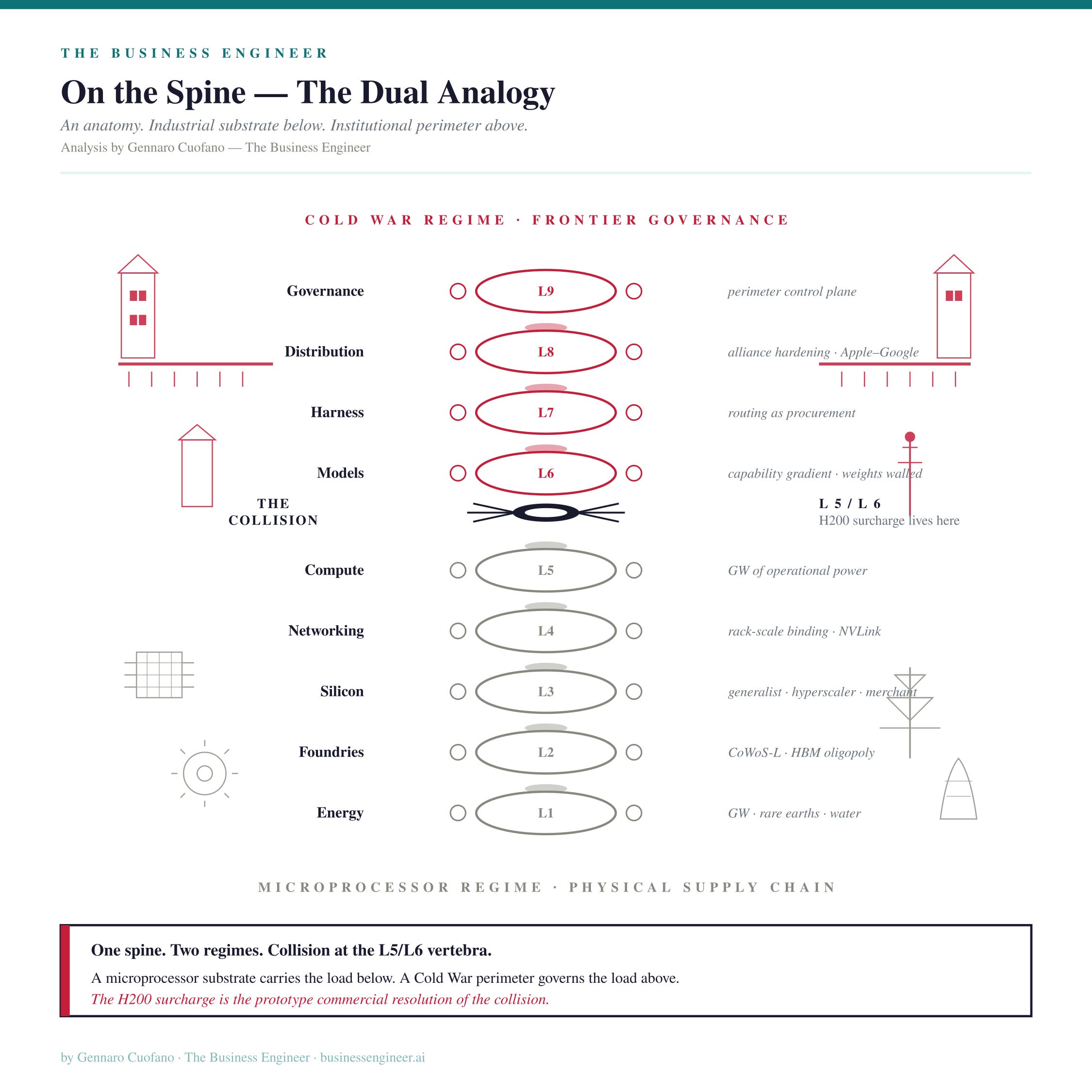

Before the three axes, the spine.

For nearly a decade, the AI cycle has been described by analogy to the microprocessor wave that began in the 1940s and matured into personal computing, the internet, mobile, cloud, and smartphones across subsequent decades. The analogy is correct, and it has done enormous work in explaining the cycle’s economic structure. But it is incomplete. There is a second analogy running in parallel, and the failure to name it explicitly is why so much commentary on the AI cycle misreads the governance regime as a regulatory footnote rather than the structural feature it actually is.

The microprocessor analogy works for the physical supply chain of AI. It covers Layers 1 through 5 of the Map: energy, foundries, silicon, networking, compute. The lessons of the microprocessor cycle apply directly to this region of the stack. Cascading bottlenecks migrate downward as upper layers scale. Geographic concentration of production creates allocation power. Incumbents capture early value because integration is linear and capital advantages dominate. Profit pools migrate up the stack as commercialization at higher layers creates demand. Everything we know about the semiconductor cycle from 1947 through 2010 applies, with translation, to the physical substrate of AI.

The Cold War analogy works for the frontier of AI. It covers Layers 6 through 9: foundation models, agentic harness, distribution surfaces, and the governance perimeter that wraps around them. A note on the analogy before going further: the Cold War is being used here exclusively as a reference for the governance and institutional architecture that emerged between rival blocs during a period of foundational dual-use technology development. The analogy says nothing about whether frontier AI poses risks comparable to nuclear weapons. That is a substantive question the framework deliberately does not take a position on. What the framework observes is that states are behaving as if they are governing frontier AI under a Cold-War-style control architecture, and the observed behavior is the structural fact the Topology has to account for.

The Cold War regime had specific institutional features that map directly onto the AI governance regime. Containment doctrine. Multilateral export controls (COCOM). Alliance-based technology bifurcation (the Iron Curtain as a technology boundary, not only a political one). Non-aligned blocs courted by both sides through infrastructure deals. Strategic redundancy doctrines (second-source supply chains, dual-track command). Capability gradients tracked and disclosed at controlled intervals. Détente as the institutional mechanism for managed commerce between rival blocs at non-strategic layers. Proxy theaters where rivalry expressed itself without direct confrontation.

Every one of these has a direct analog in the AI cycle. The Three-Tier Architecture is the containment architecture. Strategic Denial is COCOM. Sovereign procurement is non-alignment becoming a procurement category — the UAE, Saudi Arabia, India, and Brazil are courted by both the US-led and China-led stacks with infrastructure deals at sovereign scale. The dual-substrate Anthropic story is strategic redundancy doctrine. The Apple-Google distribution embedding is alliance hardening at the consumer surface. The frontier benchmark race is the capability gradient that intelligence services and procurement teams track.

The two analogies meet at the boundary between Layer 5 (Compute Capacity) and Layer 6 (Foundation Models). Below that line, microprocessor logic. Above that line, Cold War logic. The Three-Tier Architecture exists because the two regimes collide at this boundary — and the H200 deal, with its 25% government surcharge, is the prototype of how that collision gets commercially resolved. A microprocessor-era artifact subjected to a Cold-War-era control structure. The first time in industrial history that a chip has been sold under terms that resemble managed-trade détente more than the export of consumer electronics.

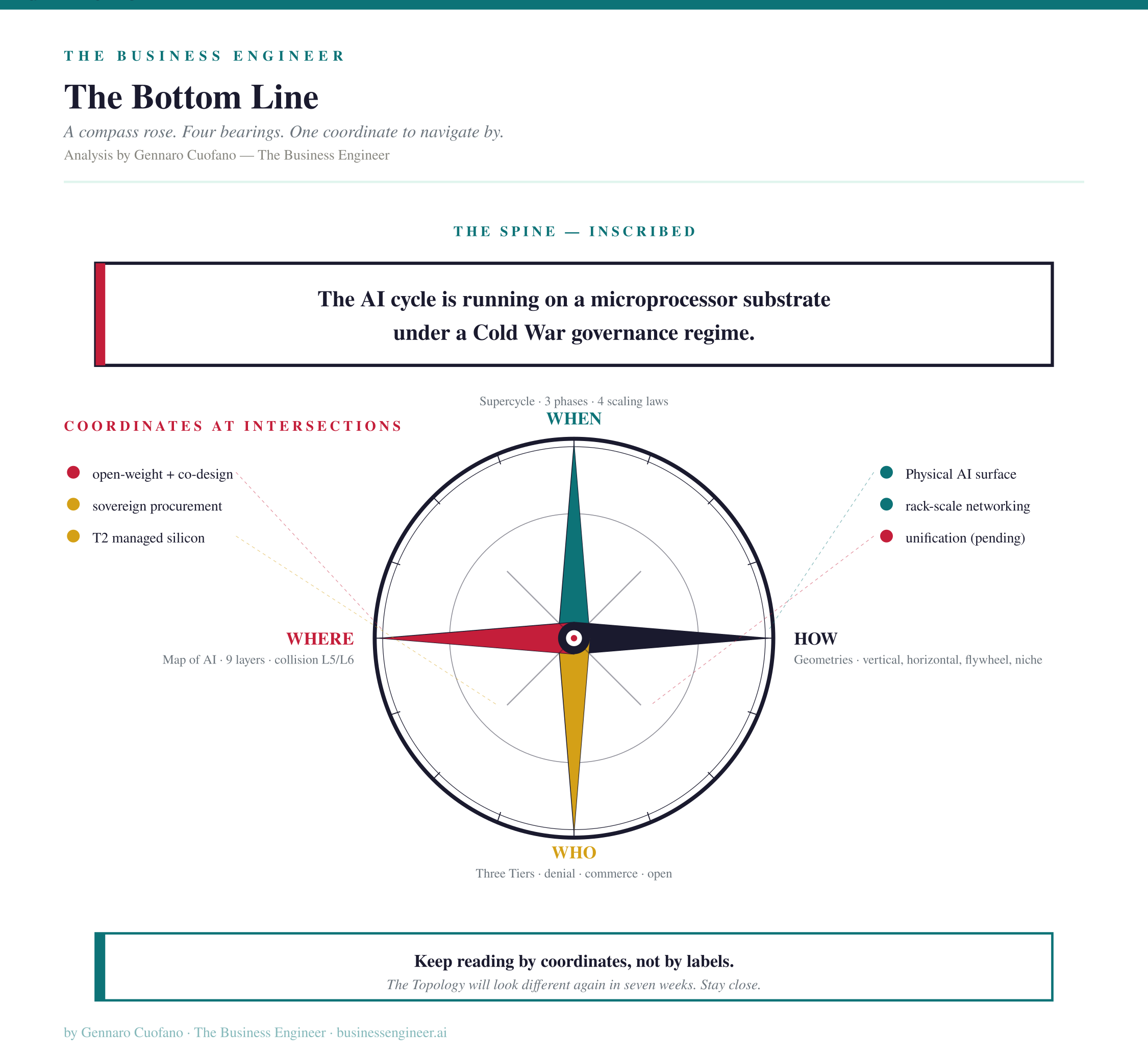

The unified statement: the AI cycle is running on a microprocessor substrate under a Cold War governance regime. That is the spine of the framework. The duality has a location in the stack. The duality has commercial consequences. And the duality is the structural reason the Topology requires three axes rather than the single axis that either analogy alone would imply.

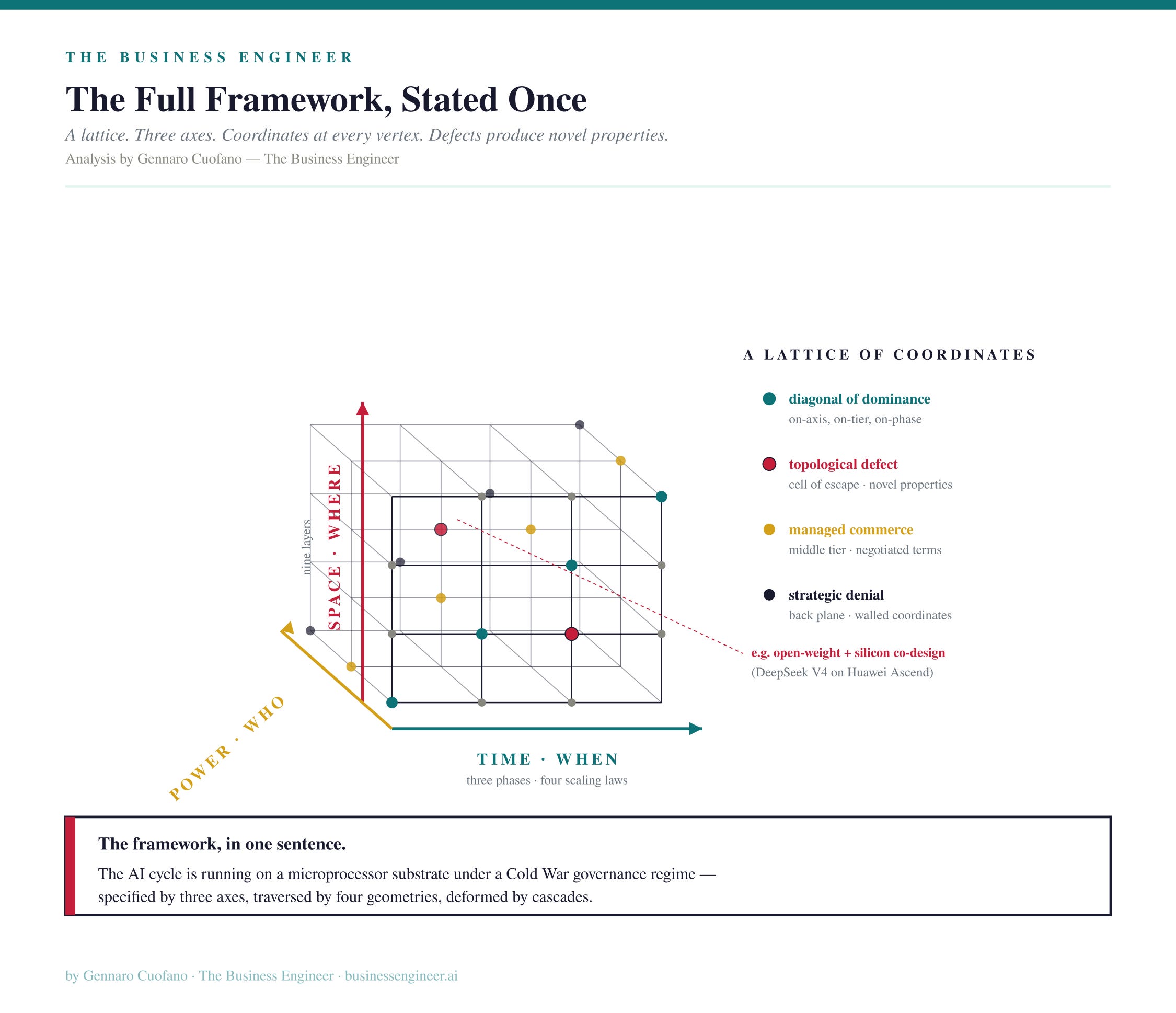

The Full Framework, Stated Once

Before the axis-by-axis walkthrough, the framework stated as a single integrated object.

The AI Supercycle Topology is a three-axis coordinate system that locates any company, technology, or commercial decision in the AI cycle, with five operating components that interact continuously.

The time axis is the AI Supercycle. Three nested phases (5-10 year linear integration, 10-20 year stalled-technology unlock, 20-50 year industry creation) running against four scaling laws operating in parallel (pre-training, post-training, reasoning, agentic tool use), with the binding research question of the next 12-18 months being whether the four scaling laws can be unified into a single self-improvement and continual-learning pipeline. The axis tells you when value emerges.

The space axis is the nine-layer Map of AI. From physical floor to perimeter: Energy, Foundries, Silicon, Networking, Compute Capacity, Foundation Models, Agentic Harness, Distribution Surfaces, Governance. Each layer is constrained by the layer below it and commercialized by the layer above it. The axis tells you where value accumulates.

The power axis is the Three-Tier Architecture of Stratified Interdependence. Strategic Denial at the frontier, Managed Commerce in the negotiated middle, Open Competition at the friction-laden base. The tier system integrates geopolitical players (states, alliances, control regimes), macroeconomic players (capital markets pricing the tier system), and technology players (companies designing architectures around tier boundaries). The axis tells you who is allowed to operate, under what conditions.

The framework runs on a dual analogy spine. The microprocessor analogy explains the physical supply chain of AI (Layers 1-5): cascading bottlenecks, allocation power, geographic concentration, incumbent paradox. The Cold War analogy explains the frontier governance regime (Layers 6-9): containment, multilateral export controls, strategic redundancy, non-aligned procurement, capability gradients. The two regimes collide at the Layer 5/6 boundary. The collision is the structural reason the Three-Tier Architecture exists at all.

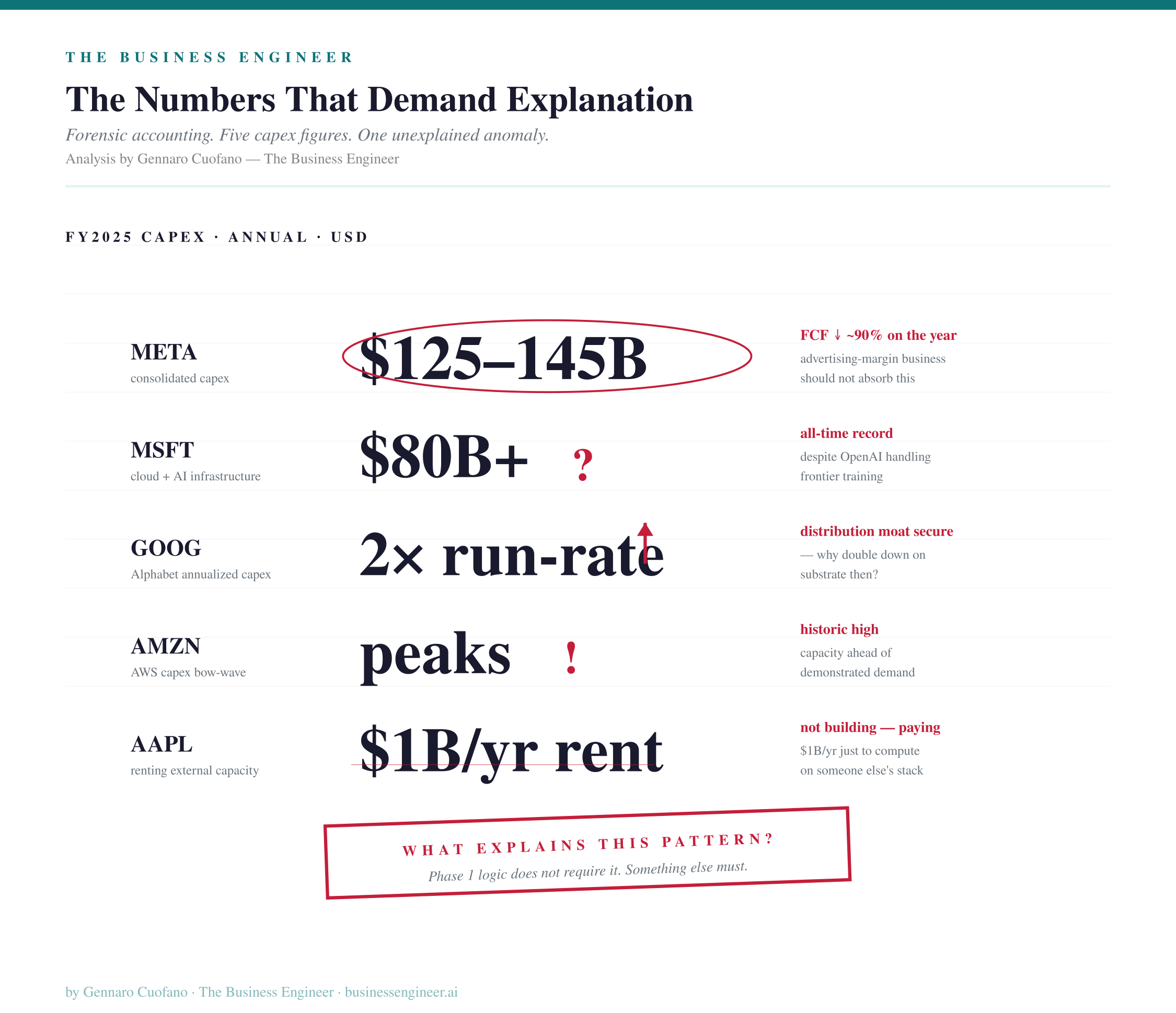

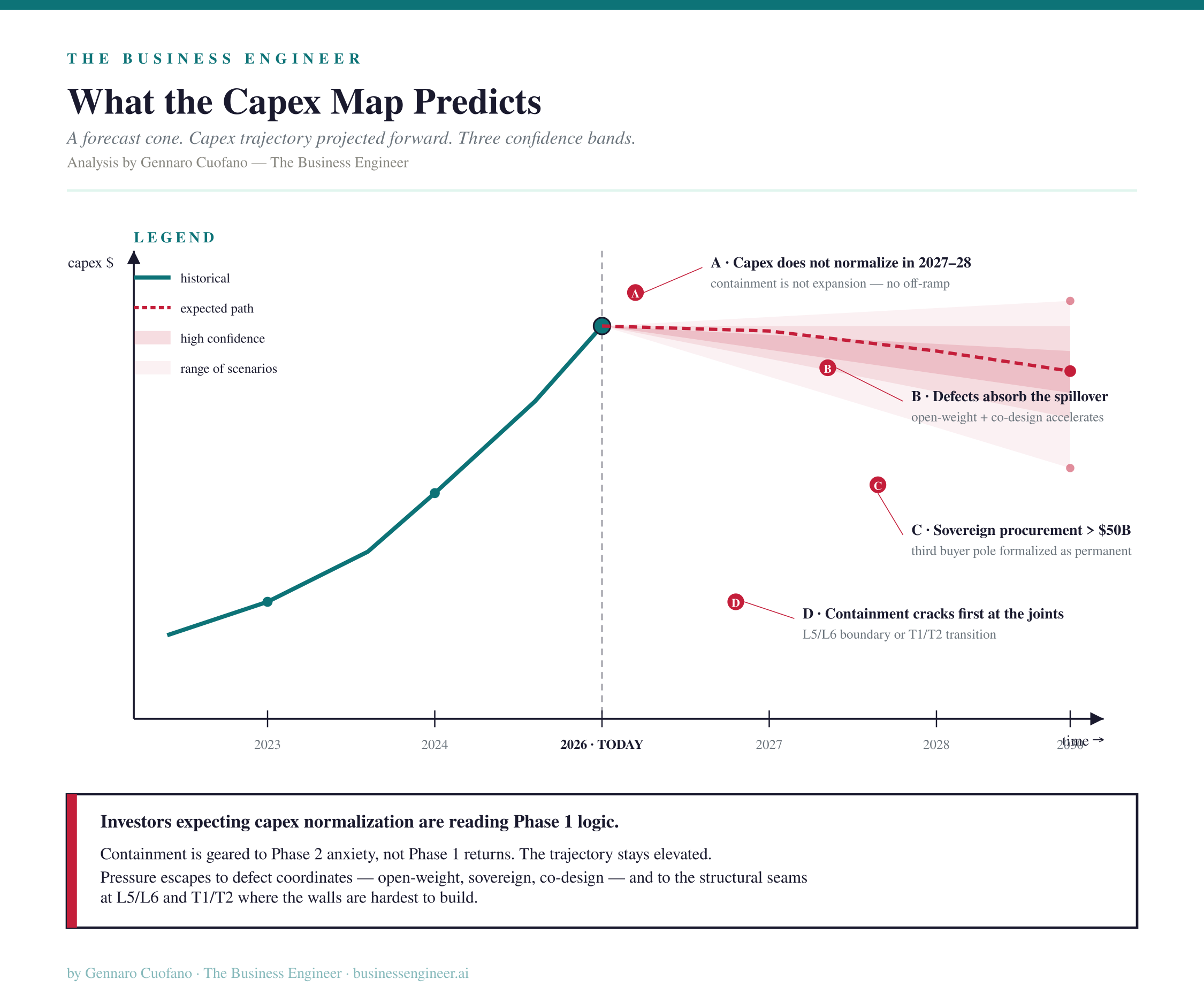

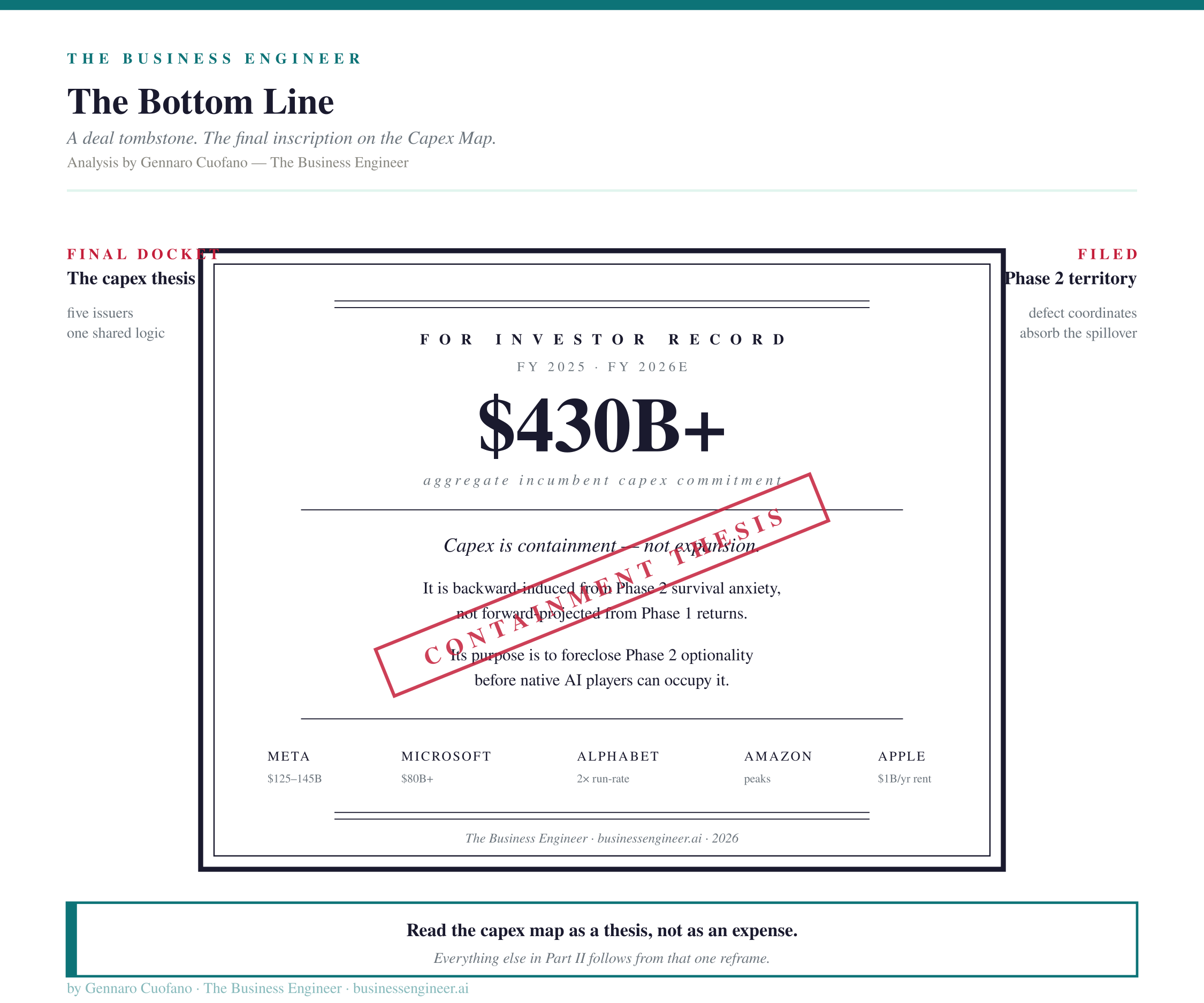

The framework’s most consequential observation is the capex map. Incumbent capex commitments at unprecedented scale (Meta $125-145B, Microsoft $80B+, Google’s doubled run-rate, Apple’s $1B/year embedding) are backward-induced from Phase 2 survival anxiety, not forward-projected from Phase 1 expansion. The incumbents have internalized the second half of the paradox — that native AI players take dominant positions in Phase 2 — and are spending at containment scales to foreclose Phase 2 territory before it can be occupied. The capex behavior is the visible proof that the cycle is being contested as a Phase 2 survival problem, not a Phase 1 integration opportunity.

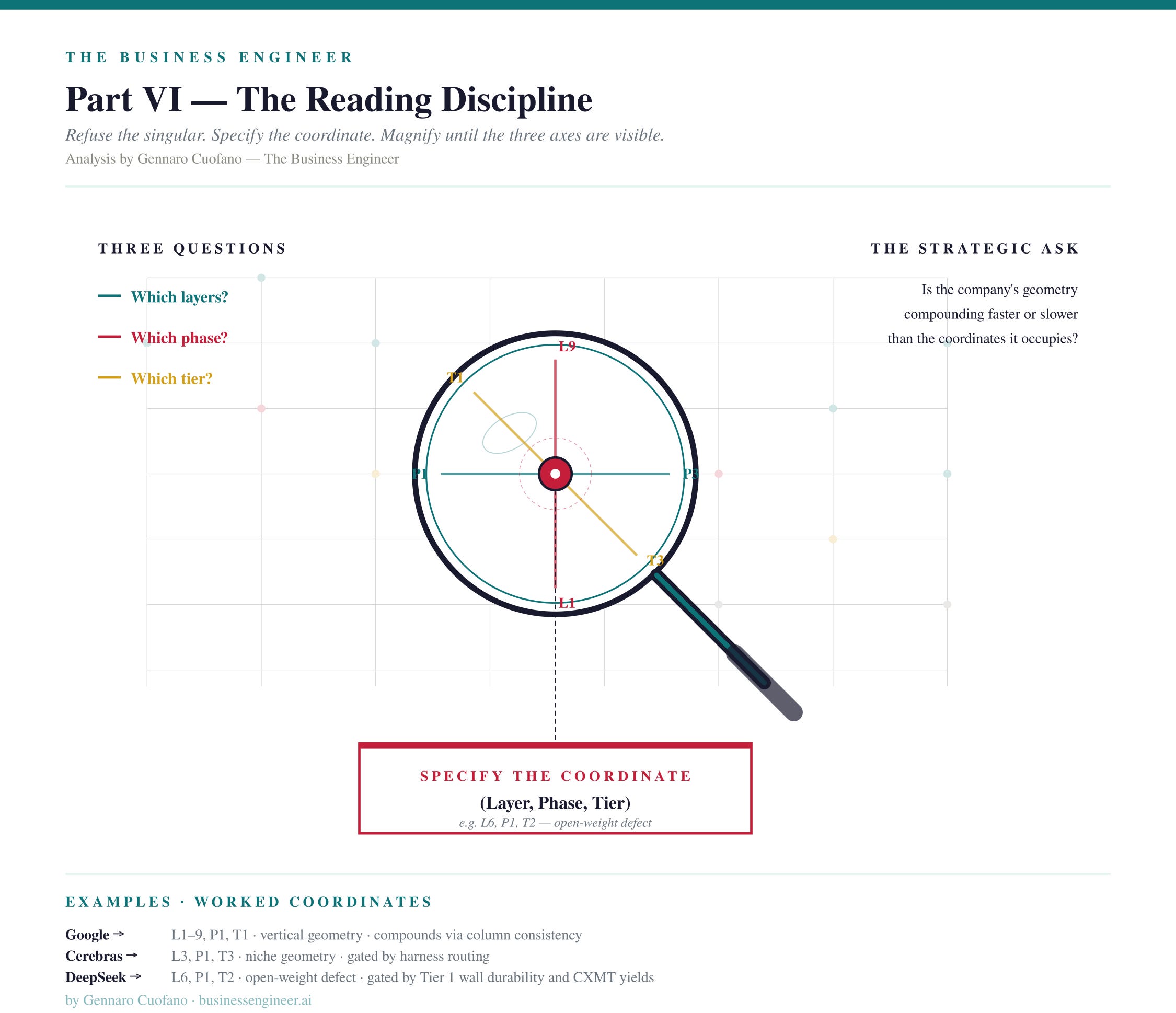

The unit of analysis is the coordinate: a triple of (layer, phase, tier) that locates a company or technology in the Topology. Coordinates are dynamic — they move quarter to quarter as cascades deform the structure.

The mechanism of change is the cascade: a deformation event that propagates through adjacent coordinates, reshaping which regions are loaded. Cascades propagate faster through layers (technical, demand-driven, months) than through tiers (political, negotiation-driven, quarters to years). Four are currently running: the downward cascade from the harness layer, the dual-substrate cascade at the compute layer, the Physical AI cascade at the distribution layer, the sovereign procurement cascade at the compute layer.

The strategic strategies are the geometries: four distinct traversal patterns through the Topology, each a direct response to the incumbent containment environment. Vertical (Google) — column ownership across nine layers within one tier; incumbent containment perfected. Horizontal (NVIDIA) — band ownership across Layers 3-5 across two tiers; selling shovels to the containment effort. Flywheel (SpaceX) — three engines compounding through five loops at Layers 1, 5, 8; operating outside contested territory. Niche by Adjacent Integration (Cerebras, Groq) — single-coordinate optimization at defects the containment cannot reach.

The reading discipline that uses all of the above is: refuse to talk about AI in the singular. Specify the coordinate. Identify the geometry. Read the cascades adjacent to the coordinate. Ask whether the company’s geometry compounds faster or slower than the coordinates it occupies.

That is the framework. Everything that follows is the detail.

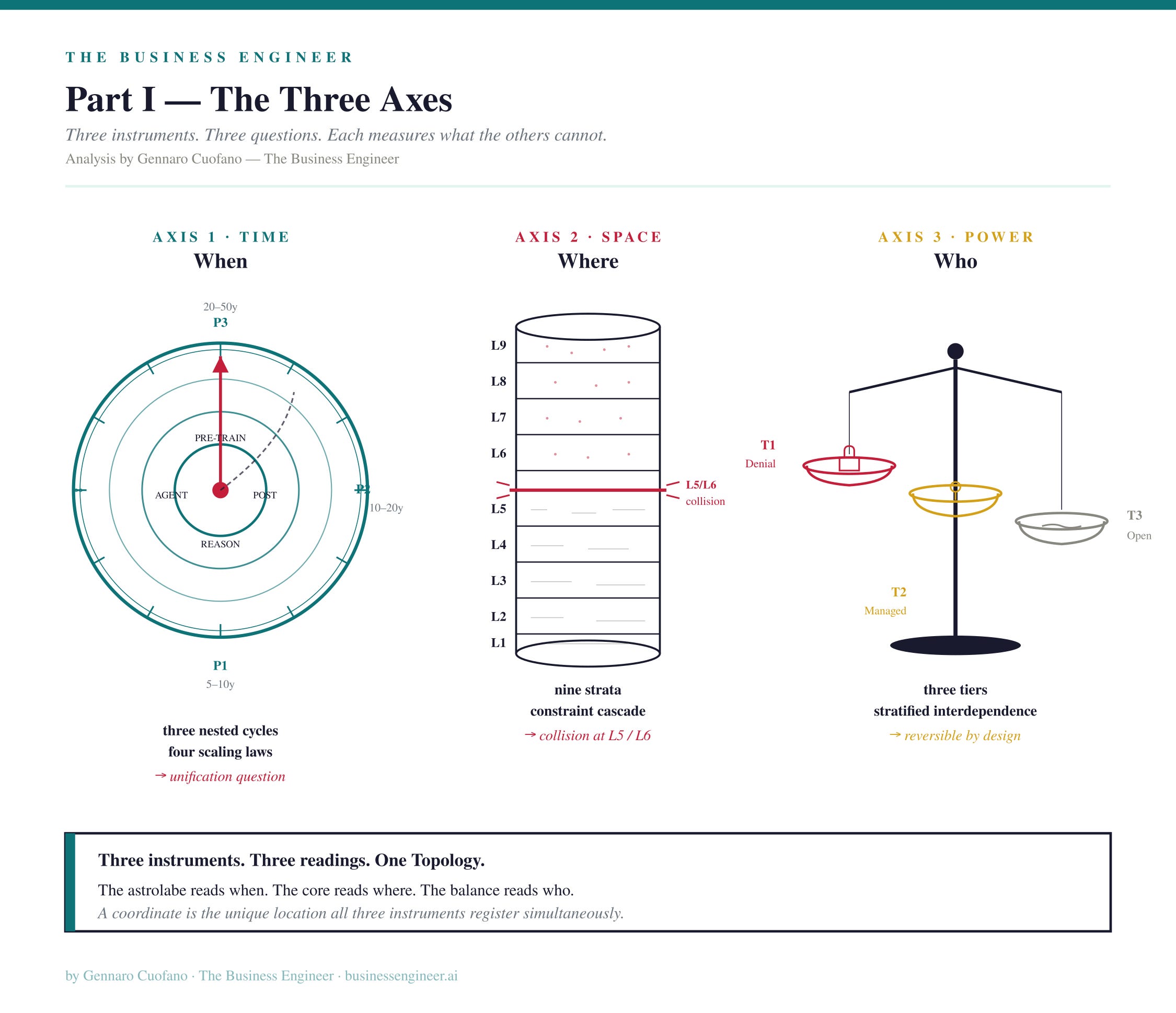

The Three Axes in Full

Axis 1: The Time Axis — The Supercycle

The Supercycle thesis describes AI not as a new industry but as a paradigm shift comparable to the microprocessor wave in its substrate-creating role for subsequent waves of industry formation. The thesis has three core components.

The three nested cycles. Within the 30-50 year supercycle run three sub-cycles of different durations. A short cycle of 5-10 years where AI integrates into existing industries through linear improvements — search becomes generative, advertising becomes hyper-personalized, software becomes 10x cheaper to produce. A medium cycle of 10-20 years where AI unlocks technologies that had stalled for non-AI reasons — robotics, autonomous vehicles, AR, ambient inference at the edge. A long cycle of 20-50 years where AI enables industries that cannot be specified in advance — the way streaming could not be specified before the internet matured.

The four scaling laws operating in parallel — and the unification question. As of mid-2026, four scaling laws are running simultaneously. Pre-training scaling (more parameters, more data, more compute). Post-training scaling (RLHF, constitutional approaches, agentic fine-tuning). Reasoning at inference time (test-time compute, chain-of-thought, deliberative search). Agentic tool use (the harness layer as capability multiplier). Each has different hardware implications, different cost structures, and different commercial profiles. The shape of the time axis is no longer a single curve. It is a four-curve composite.

But the binding research question of the next 12-18 months is not which curve dominates. It is whether the four can be unified into a single pipeline that closes into a self-improvement and continual-learning loop. If unification succeeds, the four scaling laws stop being parallel curves and become one self-reinforcing engine. Pre-training feeds capability into the base model. Post-training feeds task-specific competence into the deployed model. Reasoning feeds deliberate problem-solving into agent execution. Agentic tool use feeds environmental feedback back into the training loop. The model executes agentic tasks in production, generates feedback signal, the feedback gets distilled into post-training updates, the post-training updates feed pre-training continuation, the better pre-trained model reasons better at inference, and the better reasoning generates better agentic execution.

The strategic significance of unification is enormous. If unification succeeds at any single frontier lab before others, that lab compounds at a rate no competitor can match — because every other lab is still running disconnected pipelines. The model race that supposedly ended would resume in a more brutal form, with the winning lab pulling away through compounded self-improvement. The Phase 1/Phase 2 boundary would also become more porous: self-improving models running agentic tasks generate training signal from physical-world deployment, collapsing the distinction between “models in Phase 1” and “Physical AI deployment in Phase 2” into the same engine. And the capex map would change materially, because continuous inference at production scale becomes a training-signal generator, making inference a capex category rather than only an opex one.

The unification question is currently the binding strategic variable at the model layer. Every other variable in the framework — frontier-lab valuations, compute procurement at scale, the dual-substrate doctrine, the Apple-Google distribution embedding — is currently being structured around bets on whether unification works and which lab gets there first.

The incumbent paradox. In Phase 1, incumbents capture most of the value because integration is linear and their distribution and capital advantages dominate. Google captures generative search. Meta captures generative advertising. Microsoft captures enterprise integration. In Phase 2 and Phase 3, native AI players take dominant positions because the underlying business logic changes — and the change is non-linear enough that incumbent advantages do not translate. The paradox sits at the time axis but produces the most consequential behavior at the capital axis, which Part II of this piece treats as a standalone analytical section.

The time axis tells you which phase a layer is in, with the discipline that not all layers sit at the same phase simultaneously. Physical AI deployment surfaces are firing in Phase 2 right now. Reasoning models are deep in Phase 1. Sovereign procurement is creating Phase 1 demand against a Phase 2 deployment timeline. The clock runs differently in different regions of the Topology.

Axis 2: The Space Axis — The Map of AI

The Map of AI describes the architectural geography of the cycle. Four structural shifts forced the current nine-layer structure.

Networking separated from compute. Rack-scale interconnects now exceed 20% of system cost at scale. The unit of AI infrastructure is no longer the GPU. It is the rack. And the rack is bound together by protocols (NVLink, Spectrum-X, InfiniBand) that capture rent at every interface they touch.

Foundries separated from silicon. TSMC’s CoWoS-L allocation became the most contested resource in semiconductors. The HBM oligopoly has been forward-purchased through the late 2020s. Allocation power moved up the stack to become more consequential than chip design itself. A frontier chip without foundry allocation is a slide deck.

Silicon bifurcated internally into three categories. Generalist substrate (NVIDIA at 80%+ share). Hyperscaler custom (TPU, Trainium, MTIA, Maia, Titan). Merchant custom challengers (Cerebras, Groq, SambaNova, Tenstorrent) selling to anyone on physics dimensions NVIDIA does not optimize for. This is a within-layer split but it changes the strategic logic at every layer above silicon.

Governance separated from generic policy and trust and became a priced variable. Single government directives can switch off frontier models globally in days. Governance is no longer a footnote. It is a control plane perpendicular to every layer beneath it.

The current nine layers, from physical floor to perimeter:

LayerNameBinding constraintAnalogy regime9GovernancePolitical stability of the tier systemCold War8Distribution SurfacesEndpoint surface areaCold War7Agentic HarnessRouting economics, cost-per-tokenCold War6Foundation ModelsCapability per parameterCold War5Compute CapacityGW of operational power, rack countBoundary4Networking and ProtocolsInterconnect bandwidth, rack-scale bindingMicroprocessor3SiliconArchitecture, transistor densityMicroprocessor2Foundries and PackagingLithography, advanced packaging allocationMicroprocessor1Energy and PhysicalGW of generation, rare earths, waterMicroprocessor

Two reading rules govern the space axis. Each layer is constrained by the layer below it — you cannot ship a model without compute, you cannot ship compute without silicon, you cannot ship silicon without foundries, you cannot ship foundries without energy. Binding constraints migrate downward when capacity at a lower layer becomes scarce. And each layer is commercialized by the layer above it — silicon needs models to monetize, models need a harness, harnesses need distribution. Profit pools migrate upward when commercialization at a higher layer creates demand.

The space axis tells you where value accumulates, where rent gets captured, and which analogy regime governs the strategic logic at any given layer.

Axis 3: The Power Axis — The Three-Tier Architecture

The Three-Tier Architecture is the power axis. It is not a geopolitical framework alone, a macroeconomic framework alone, or a technology framework alone. It is the integrated regime under which all three operate, because the tier system simultaneously specifies geopolitical access conditions, prices into macroeconomic variables, and forces technological architecture decisions.

Tier 1 — Strategic Denial. Hard wall. The answer is structurally no, and the answer holds across administrations because the underlying logic is alliance capitalism: capability denial as strategic imperative.

Geopolitical layer: Frontier GPUs (Blackwell, Rubin). EUV lithography. Sub-3nm fabrication. Frontier model weights. Quantum computing primitives. The walled perimeter of the allied bloc.

Macroeconomic layer: The wall is priced into NVIDIA’s forward guidance as a permanent base case (zero China data center compute revenue). It is priced into secondary-market valuations of frontier labs (Anthropic’s dual-substrate compute strategy carries a premium that single-substrate execution does not). It is priced into procurement contracts that include compliance clauses with extraterritorial reach.

Technological layer: Forces dual-substrate architectures at frontier labs (Anthropic on Google TPU plus SpaceX COLOSSUS). Forces silicon co-design on the non-allied side of the line (DeepSeek V4 on Huawei Ascend). Forces the inference layer to route on cost-per-token rather than peak capability when the peak is walled off.

Tier 2 — Managed Commerce. Permissioned flows with leverage embedded. Washington controls the tap, monetizes the flow, makes the arrangement politically sustainable.

Geopolitical layer: Previous-generation semiconductors (the H200 deal). Agricultural commodities. Aircraft. Energy. Green technology. The negotiated middle ground.

Macroeconomic layer: The 25% government surcharge on H200 sales is a revenue-sharing mechanism, not a tax. It transforms a layer into an export industry with embedded political conditions. The surcharge model is the prototype that will extend to other previous-generation strategic technologies as Tier 1 walls move forward.

Technological layer: Creates a category of products designed for Tier 2 — chips deliberately specified at one generation behind the frontier, models deliberately released as open-weight to flow through the managed perimeter, infrastructure deliberately scoped to operate under the surcharge regime.

Tier 3 — Open Competition. Non-strategic goods at permanently elevated but negotiated friction. The new structural cost of doing business, not a temporary disruption.

Geopolitical layer: Consumer goods, industrial inputs, general manufacturing. Section 122 (15%) plus Section 301 (7.5-100%) plus Section 232 (sector-specific).

Macroeconomic layer: The friction is priced into supply chain decisions, into reshoring incentives, into the equity valuations of companies positioned for Tier 3 commerce.

Technological layer: Most consumer-facing AI products operate in this tier — the harness layer routing is largely Tier 3, the merchant custom silicon market is largely Tier 3, open-weight model deployment outside the frontier is largely Tier 3.

Two properties of the architecture matter for the Topology.

The tiers are not universal. They are specific to the layer and the asset class. The same two countries in strategic confrontation over semiconductors are simultaneously cooperating on agricultural commodities and co-managing energy stability. The rules of access differ by what is being accessed.

The architecture is reversible by design. It is built on rolling truces, not treaties. A Supreme Court ruling reconfigured the US tariff architecture in 72 hours in February 2026. A China-side breakthrough at CXMT or SMIC could collapse Strategic Denial in semiconductors and reorganize the power axis below the foundation model layer. A single sovereign procurement crossing $50 billion formalizes a new sub-tier inside Compute Capacity that does not currently exist as a stable category.

The power axis tells you who is allowed to operate at a given layer, under what political conditions, with what restraint embedded — and how the access regime simultaneously prices into capital markets and forces architectural decisions on the companies operating across it.

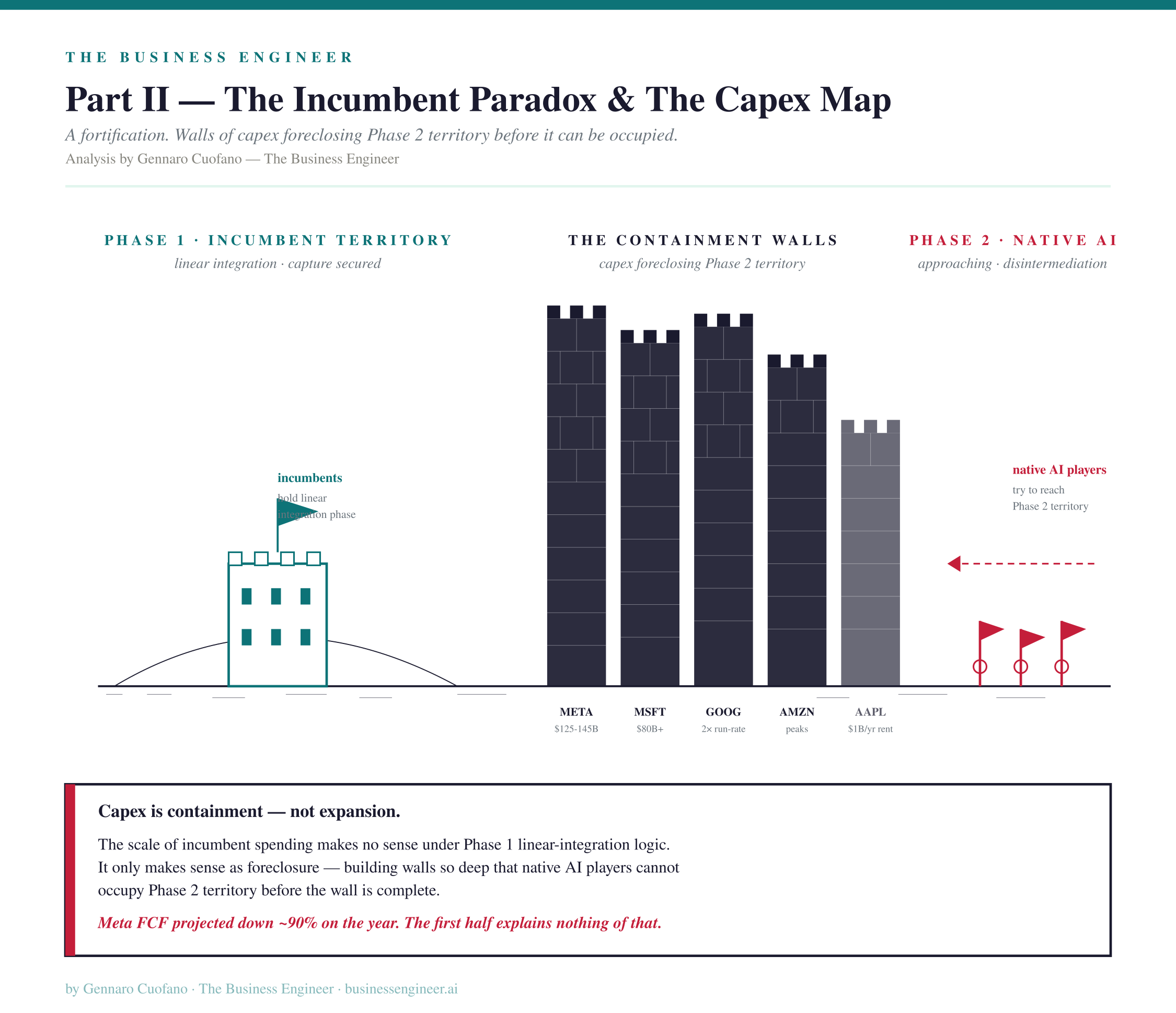

Part II — The Incumbent Paradox and the Capex Map

The most analytically important behavior in the current cycle is not the model race, the silicon race, or even the geopolitical contest. It is the scale of incumbent capex spending. And the spending makes no sense under a forward-looking Phase 1 logic. It only makes sense under a backward-induced Phase 2 survival logic. Reading the capex map correctly is the key to reading the entire cycle.

The Numbers That Demand Explanation

The capex commitments of the largest incumbents are at scales that have no precedent in software industry history.

Meta is guiding to $125-145 billion in capex for 2026, with free cash flow projected down nearly 90% on the year, and has executed approximately 8,000 layoffs to redirect headcount into compute build-out. Microsoft committed $80 billion+ across the Fairwater facility and its successors, then absorbed displaced Stargate capacity (the 700 MW that Norway and the UK declined to host) into its own infrastructure plan. Google’s capex run-rate has doubled in 24 months, and the Apple distribution deal at roughly $1 billion per year is itself a capex substitute — paying to rent distribution capability rather than build it. Amazon’s AWS infrastructure spend is at multi-year peaks. NVIDIA is selling into all of this and recycling the cash into networking acquisitions, foundry pre-payments, and the sovereign procurement pipeline.

These are not the spending patterns of companies that believe they will simply integrate AI into their existing dominance and continue compounding linearly. A linear-integration Phase 1 thesis would justify capex at perhaps half these levels. The remainder is something else.

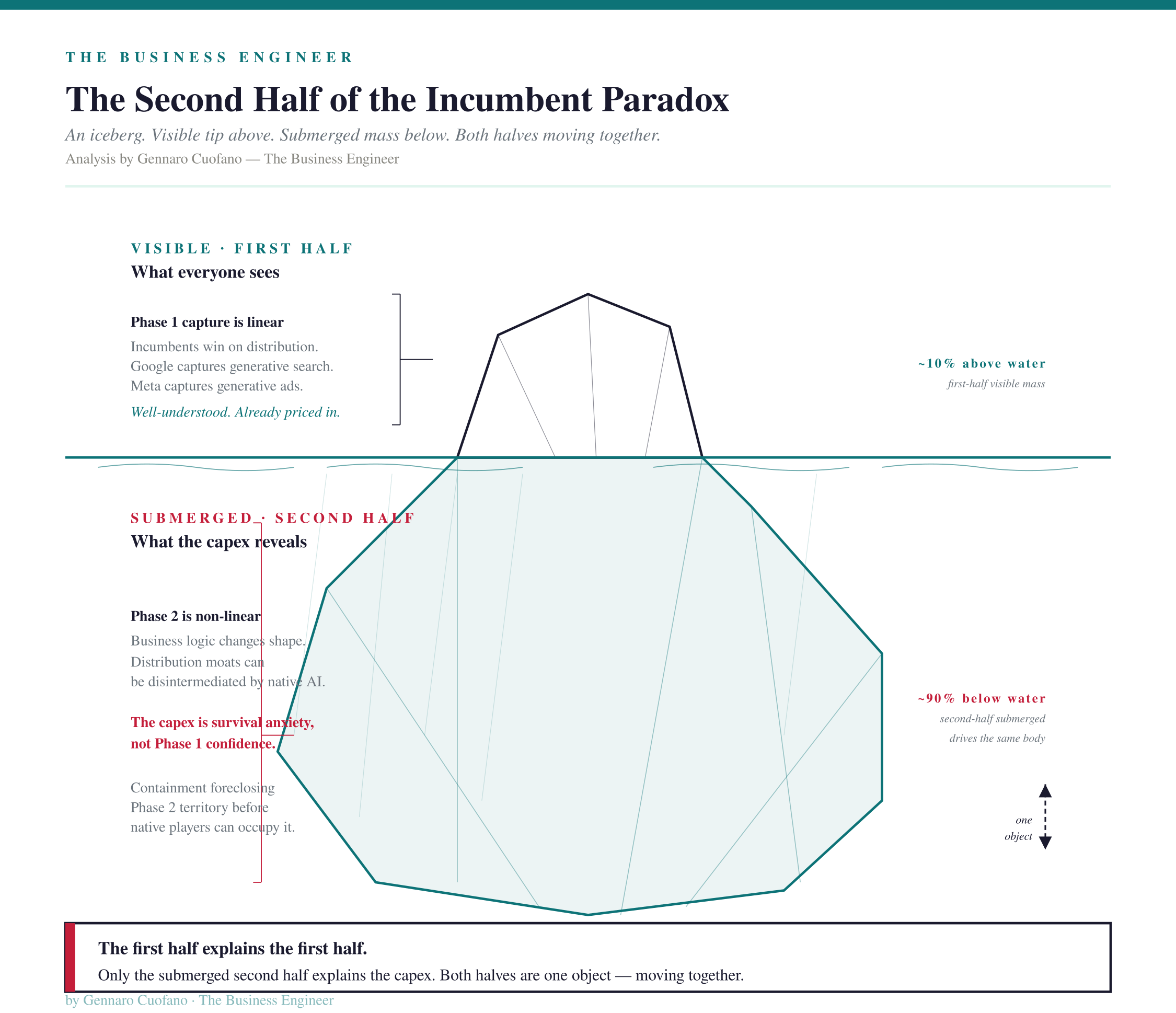

The Second Half of the Incumbent Paradox

The incumbent paradox has two halves. The Phase 1 half says that in early integration, incumbents capture most of the value because integration is linear and their distribution, capital, and operational advantages dominate. That half is well understood and uncontroversial.

The Phase 2 half says that as the underlying business logic changes — as native AI players reach scale, as the substrate becomes the product, as distribution surfaces themselves get disintermediated by AI-native interfaces — incumbents lose their structural advantages, and the dominant players of the new phase are often not the same companies as the dominant players of the previous phase. The Phase 2 half is less discussed but more consequential.

The capex commitments tell us that the incumbents have internalized the second half of the paradox. They are not spending at these scales because they believe Phase 1 integration will be valuable — though it will be. They are spending at these scales because they believe Phase 2 will be existentially dangerous to their current positions if they do not lock in territory before native AI players reach it first.

The aggressive lock-in is rational under this reading. Meta’s capex bet is that its 3-billion-user distribution moat plus its own MTIA silicon plus its own Muse Spark model can outrun the disintermediation. Microsoft’s bet is that Copilot embedding plus Azure neutrality on model choice locks in enterprise procurement before native AI players reach enterprise scale. Google’s bet is the only one that fully bridges the two phases — the vertical column from silicon through distribution gives it the chance to remain dominant across the Phase 1/Phase 2 transition rather than only on one side of it.

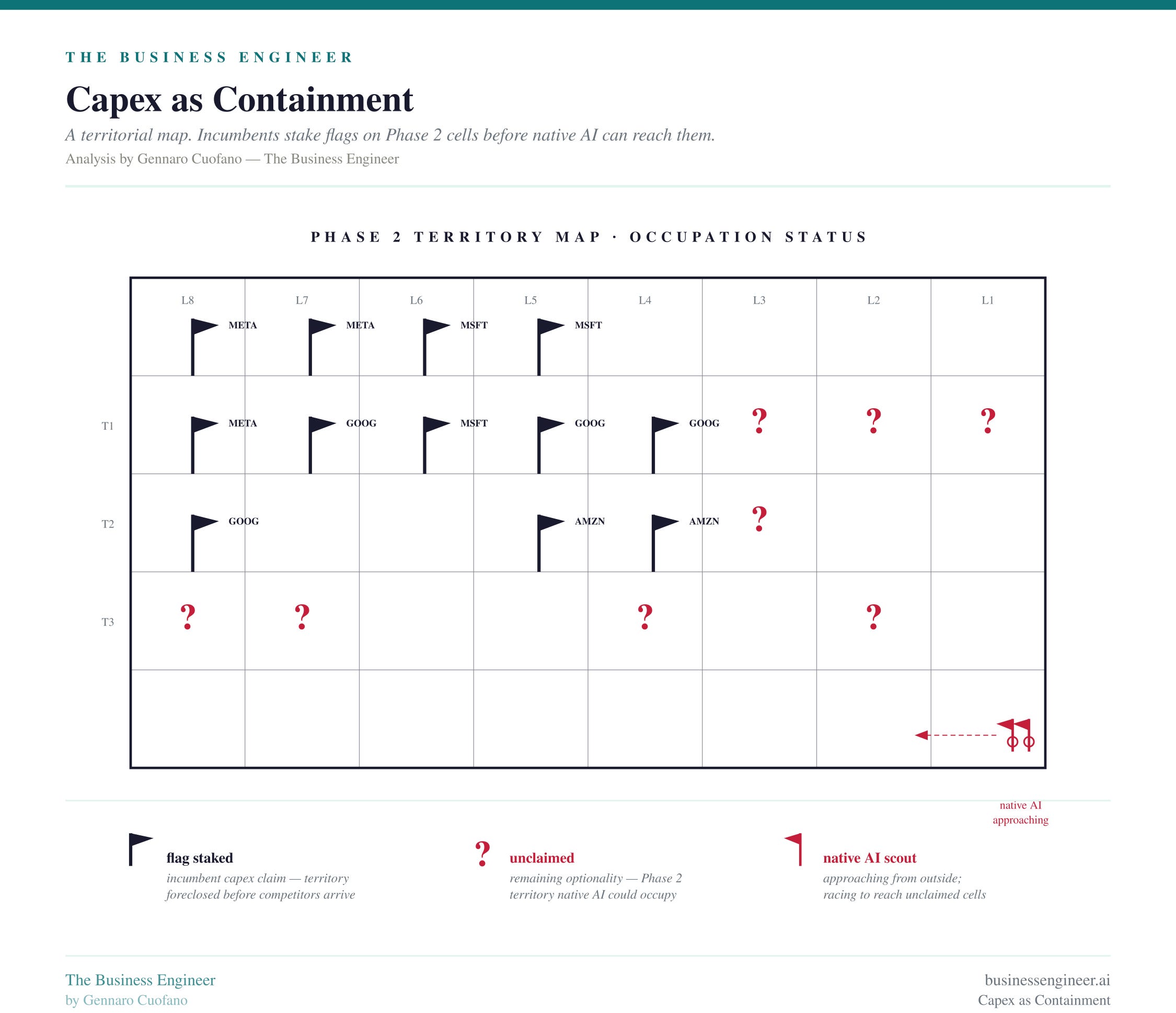

Capex as Containment

In Cold War terms, the incumbent capex bet is containment. The incumbents are not racing to win Phase 1. They are racing to make Phase 2 too capital-intensive for any native AI player to challenge their position. The strategy is to build moats deep enough to survive the disintermediation phase by foreclosing the territory before the rival reaches it.

This explains several otherwise puzzling features of the current cycle. It explains the willingness to crater near-term free cash flow — Meta’s free cash flow projected down nearly 90% on the year is incomprehensible under a Phase 1 thesis but perfectly rational under a Phase 2 containment thesis. It explains the urgency of the embedding deals — the Apple-Google arrangement is paying $1B/year for distribution embedding because the alternative is letting a native AI player reach a billion devices first. It explains the willingness to absorb displaced infrastructure — Microsoft picking up the 700 MW that Stargate could not place is rational because compute capacity is itself the contested territory.

It also explains the asymmetric incumbent behavior. Apple’s containment strategy is to rent capability (the Google deal) while keeping option value on building in-house, because Apple’s distribution moat is durable enough to outlast a two-year window of rented capability. Meta’s containment strategy is to spend more aggressively than anyone because Meta’s distribution moat (social and advertising surfaces) is more disintermediation-vulnerable than Apple’s (hardware and OS). Google’s containment strategy is the most coherent because Google is the only incumbent with a full vertical column that can be defended at every layer simultaneously.

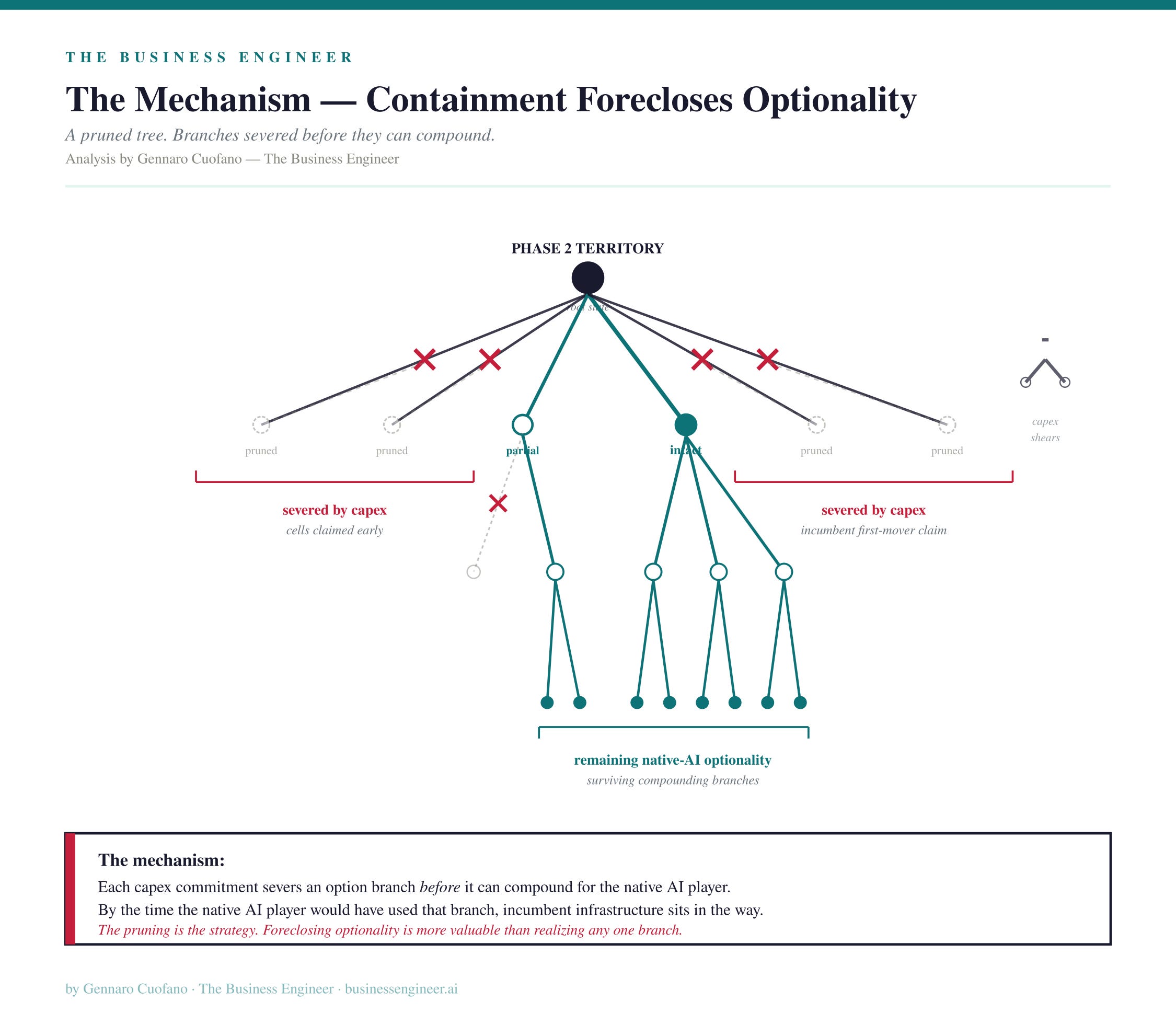

The Mechanism: Containment Forecloses Optionality

The structural mechanism is foreclosure of optionality. By spending at unprecedented scale at every layer of the substrate (compute, models, silicon, distribution embedding), the incumbents are foreclosing the optionality that a native AI player would otherwise have to enter at any single layer. The native AI player cannot challenge Google by building only a model, because Google’s column denies the silicon access, the compute access, the distribution access. The native AI player cannot challenge Meta by building only a distribution surface, because Meta’s capex denies the compute substrate and the silicon underneath.

The containment is not absolute. Two categories of native AI players have already broken through despite the containment: the frontier labs (OpenAI, Anthropic, xAI) by going directly to the model layer with sovereign-scale capital and dual-substrate compute arrangements, and the merchant custom silicon players (Cerebras, Groq) by occupying defect coordinates where the incumbent containment did not reach. Both categories survive because they did not try to enter on the incumbents’ chosen terrain.

But containment is succeeding broadly. The total number of native AI players currently positioned to threaten incumbent dominance in Phase 2 is small — perhaps 6-10 companies globally that have credible Phase 2 positions, and most of them are either embedded inside incumbent partnerships (OpenAI/Microsoft, Anthropic/Google + SpaceX) or operating in cells of escape (DeepSeek, Cerebras) rather than directly confronting incumbent territory.

What the Capex Map Predicts

If the containment thesis is correct, three predictions follow.

First, incumbent capex will not normalize as Phase 1 matures. It will continue at elevated levels through Phase 2 because the strategic logic is foreclosure, not expansion. Investors expecting capex normalization in 2027-2028 are reading Phase 1 logic into a Phase 2 contest.

Second, the dominant native AI players of Phase 2 will be the ones that occupied territory the incumbents could not reach in time. The frontier labs, the merchant custom silicon players, and the open-weight + silicon co-design coordinate are the working examples. New native players entering after 2026 will need to find new defects, because the incumbents have closed the obvious entry points.

Third, the geometries from Part IV of this piece — vertical, horizontal, flywheel, niche — are not just strategic descriptions. They are direct responses to the containment environment. Vertical geometry is incumbent containment perfected. Horizontal geometry is selling shovels to the containment effort. Flywheel geometry is the only geometry that does not play the incumbent containment game (because it operates outside the incumbents’ chosen terrain). Niche geometry is occupying defects the containment cannot reach.

The capex map is not a side variable. It is the most visible direct evidence that the incumbent paradox is fully operational, that the second half is what’s actually driving behavior right now, and that the entire cycle is being structured around the question of which incumbents survive the Phase 2 transition and which native AI players break through.

Coordinates, Cascades, and Geometries

Coordinates as the Unit of Analysis

A coordinate in the Topology is specified by three values: which of the 9 layers, which of the 3 phases, which of the 3 tiers. Companies and technologies do not occupy fixed cells in a grid. They occupy coordinates that may move next quarter, depending on cascades.

The discipline is to refuse to talk about “AI” in the singular and instead specify the coordinate. Every company, every technology, every commercial decision lives at a coordinate, and the coordinate determines the compounding rate, the risk profile, and the access regime.

Coordinates are dynamic. A coordinate is “Layer 6, deep in Phase 1, anchored in Tier 1 with secondary exposure to Tier 2” — and that coordinate may shift if a tier boundary deforms or a phase boundary moves. The reading discipline is explicitly impermanent — it produces working positions in a Topology that is itself deforming.

The Loaded Regions of the Topology in Mid-2026

Rather than enumerate eighty-one possible cells, the analytical work is to identify the regions of the Topology that are currently loaded — where cascades are concentrating commercial action.

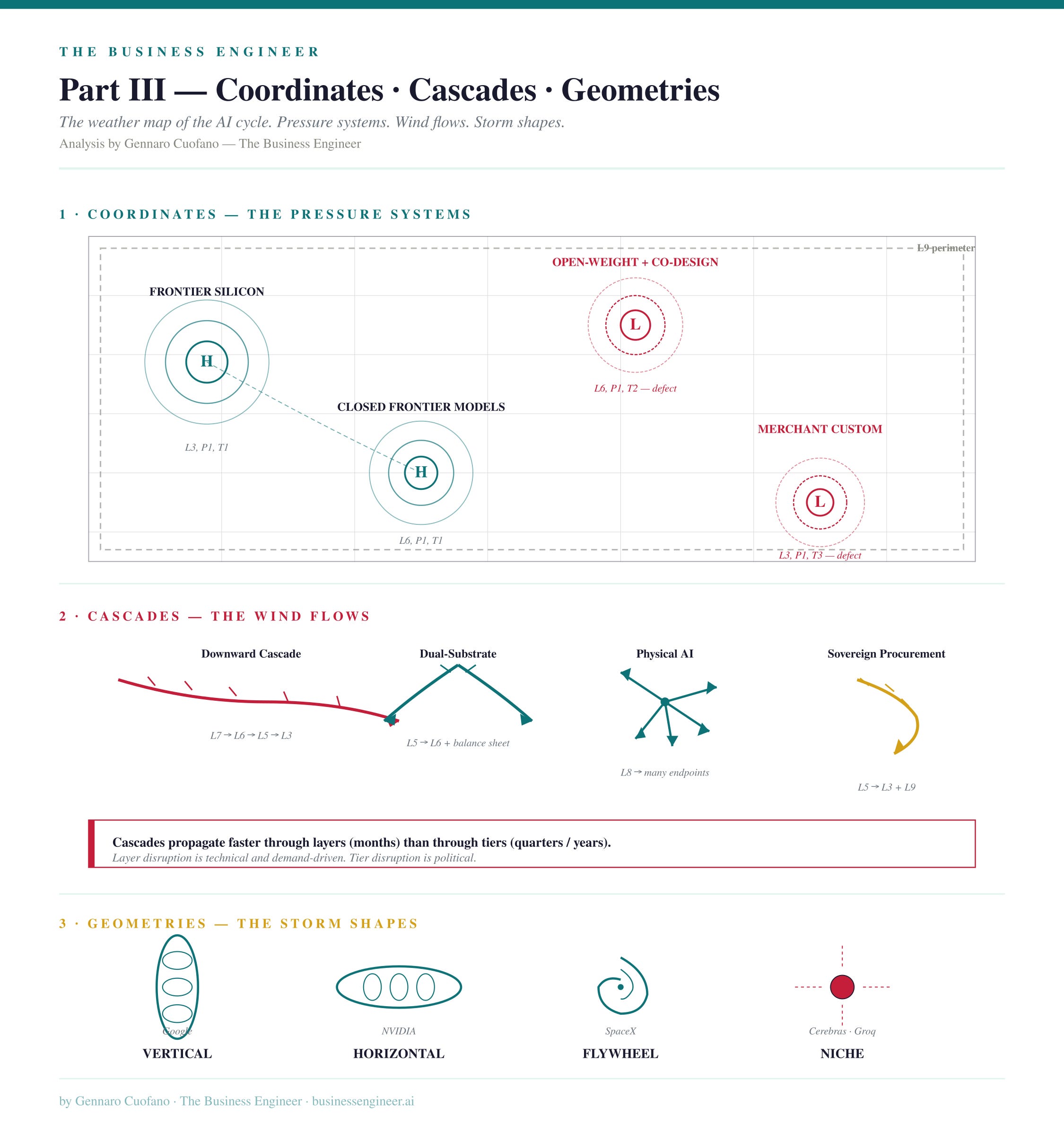

The frontier silicon region. Layer 3, Phase 1, Tier 1. Where Blackwell and Rubin live. Peak rent extraction running now. Walled by export controls that NVIDIA has internalized into forward guidance as a permanent base case. The structural bull case for NVIDIA lives here. The region stays loaded as long as the US can enforce the wall, which depends on TSMC, the Netherlands, Japan, and Korea continuing to align inside the perimeter.

The managed commerce silicon region. Layer 3, Phase 1, Tier 2. The H200 deal at the 25% surcharge. The prototype of how an entire layer can be commercially harvested at the boundary between Tier 1 and Tier 2. The region will extend over the next 24 months as more previous-generation strategic technologies are subjected to the surcharge structure.

The merchant custom silicon region. Layer 3, Phase 1, Tier 3. Cerebras, Groq, SambaNova, Tenstorrent. The downward cascade from the harness layer lands here. The region is structurally defensible because the harness above routes by cost-per-token and the foundries below are modularized. Other companies’ cross-layer binding has done the binding work for these companies.

The rack-scale networking region. Layer 4, Phase 1, Tier 1/2. NVLink, Spectrum-X, the protocols binding the rack together. Networking grew nearly 200% year over year because the binding constraint of cluster scale promoted this layer from cost item to system economic. The single most strategically important sub-layer for NVIDIA and the largest unrealized profit pool for any competitor that can credibly enter it.

The sovereign procurement region. Layer 5, Phase 1, Tier 2/3 boundary. Stargate UAE operational. Stargate UK in build. French sovereign cloud frameworks codified. Saudi PIF capital committed. The third buyer pole emerging with political conditions attached, and the region where the boundary between Tier 2 and Tier 3 is actively being negotiated. Sovereigns want infrastructure, not US-cloud-tenancy. In Cold War terms, this region is the non-aligned bloc emerging as a procurement category.

The frontier lab substrate region. Layer 5, Phase 1, Tier 1. Where the dual-substrate Anthropic story lives. Two independent compute substrates is a balance-sheet feature priced directly into secondary markets. Single-substrate compute with execution slippage is a liability priced directly into the IPO conversation. The region where compute-layer diversification became a Tier 1 valuation variable — strategic redundancy doctrine applied to commercial substrate.

The closed frontier model region. Layer 6, Phase 1, Tier 1. GPT-5.5, Claude Opus 4.7, Gemini 3.1 Ultra. Wallable. Switchable by government directive. The region where the model race compresses, where benchmark leadership trades between three labs, and where the strategic question is no longer “who has the best model” but “whose substrate diversification, distribution embedding, governance posture, and pipeline unification compounds fastest.”

The open-weight plus silicon co-design region. Layer 6, Phase 1, Tier 2. DeepSeek V4 optimized for Huawei Ascend 950PR. Llama on Cerebras. Mistral and Qwen on inference-specialized clouds. This region did not exist in any single framework alone. It became visible only when all three axes were crossed: an open-weight model, at Phase 1 commercial deployment velocity, in Tier 2 where the Strategic Denial wall forced silicon co-design to remain competitive. The co-designed pair becomes its own deployment paradigm.

The agentic harness routing region. Layer 7, Phase 1, Tier 3. Claude Code, Codex, Cursor, and the multi-vendor enterprise default. The harness layer has stopped being a workflow wrapper and become a routing engine — selecting between models on capability, between silicon on cost-per-token, between deployment substrates on latency. The region that generates the downward cascade through Layers 6, 5, and 3. The unification of the four scaling laws, if it succeeds, will reshape this region first.

The Physical AI distribution region. Layer 8, Phase 2, Tier 2/3. Starlink terminals at 10 million units. Robotics, automotive inference, AI-RAN base stations, workstations, game consoles. Phase 2 is firing here now. The region with the largest unrealized deployment surface area in the cycle.

The embedded frontier region. Layer 8, Phase 1, Tier 1. The Apple-Google deal embedding Gemini in iOS 26.4 and iOS 27. The frontier model entering the distribution surface of a billion devices. The region that makes vertical geometry economically generative — without distribution embedding, the column does not compound. And the canonical example of incumbent capex as containment: paying $1B/year to foreclose the surface before a native AI player reaches it.

The governance perimeter region. Layer 9, all phases, meta-tier. Layer 9 is the Three-Tier Architecture expressed in industrial terms. Governance does not sit on top of the stack. It surrounds the stack as a control plane perpendicular to every layer. The region where the rules of the Topology itself are being written — and where the rules change inside days rather than years.

The Diagonal of Dominance

Across the Topology, structural dominance concentrates along a diagonal that runs from current-phase to strategic-layer to high-tier. The diagonal of dominance is where the largest companies in the cycle have positioned themselves: NVIDIA along Layers 3-5 in Tier 1/2 in Phase 1. Google along Layers 3-9 in Tier 1 in Phase 1. SpaceX along Layers 1, 5, and 8 in Tier 1 in Phases 1 and 2 simultaneously. Anthropic along Layers 5-7 in Tier 1 in Phase 1. OpenAI along Layers 6-8 in Tier 1 in Phase 1.

The diagonal of dominance is not a destiny. It is the current arrangement of the largest profit pools, and it is sensitive to which regions of the diagonal stay loaded with rent and whether any company can build a credible position off-diagonal that compounds faster than the on-diagonal incumbents.

The Defects of the Topology

The most strategically interesting positions are not on the diagonal of dominance. They are topological defects — coordinates where a Tier 1 wall or an incumbent containment strategy has forced a non-incumbent to build a structurally different commercial paradigm.

The open-weight plus silicon co-design region is the canonical defect. China is structurally walled out of Tier 1 frontier silicon. The escape path is co-design: an open-weight model that runs efficiently on indigenous silicon, with the inference layer routing on cost-per-token rather than peak capability. The region exists only because the Tier 1 wall forced it into existence. And it now produces deployment economics that compound differently from the closed-weight Tier 1 region — open-weight models can be embedded into hardware shipments, can run inference at the edge, can be co-developed across multiple silicon vendors simultaneously.

The merchant custom silicon region is a second defect. NVIDIA’s full-stack dominance forced merchant challengers to flank rather than compete. The flanking position is defensible because the harness above routes against NVIDIA on price for specific workload shapes — and the routing logic is durable as long as agentic queries continue to consume 500x the tokens of chat queries.

Defects compound differently from diagonal positions. They generate fewer absolute dollars in the short run, but they are structurally more resilient to single-layer disruption because their geometry was built under structural constraint rather than under structural advantage. In topological terms, defects produce novel commercial properties — the same way doped defects in a silicon crystal produce the semiconductor properties that make computing possible in the first place.

Cascades as Propagation Logic

Cascades are how the Topology reorganizes itself. They are deformation events that propagate through coordinates, reshaping which regions are loaded and which are not. Four cascades are currently running and reshaping the Topology in real time.

The downward cascade from the harness. Started at Layer 7 with the agentic harness becoming a routing engine. Propagated to Layer 6 by giving open-weight models a commercial path that does not depend on NVIDIA. Propagated to Layer 5 by creating inference-specialized clouds as a new sub-category. Propagated to Layer 3 by making merchant custom silicon economically rational. Four layers reorganized inside 18 months. The cascade is still running.

The dual-substrate cascade. Started at Layer 5 with SpaceX’s compute services agreement with Anthropic. Propagated to Layer 6 by pricing the asymmetry between dual-substrate labs (Anthropic) and single-substrate labs (OpenAI) directly into secondary-market valuations. Propagated to the macroeconomic dimension of Tier 1 by making compute-layer diversification a balance-sheet feature priced into the IPO conversation. The cascade is reshaping how frontier labs are valued.

The Physical AI cascade. Started at Layer 8 with the Edge Computing redraw collapsing gaming, workstations, robotics, AI-RAN, automotive, and satellite terminals into a single Physical AI surface. Pulling Phase 2 commercialization forward across multiple endpoint categories simultaneously. The adoption velocity in industrial robotics is pulling adjacent endpoint categories along the same curve. The cascade is shortening Phase 2’s timeline.

The sovereign procurement cascade. Started at Layer 5 with sovereign AI moving from announcement to order book. Creating a new buyer pole that does not fit cleanly into either Tier 2 or Tier 3. Propagating to Layer 3 (frontier GPU) by formalizing a new procurement category. Propagating to Layer 9 (governance) by extending the political conditions of the access regime to new jurisdictions. The cascade is creating a new sub-tier inside Compute Capacity that does not currently exist as a stable category.

Cascades propagate faster through layers than through tiers. A deformation at a single layer can reorganize four layers in months (the downward cascade is the working example). A deformation at a single tier reorganizes the access regime more slowly — the Three-Tier Architecture has held essentially intact through three administrations and one Supreme Court ruling. Plan for both. Expect more of the former.

Geometries as Traversal — And as Containment Response

Companies do not occupy coordinates in a literal sense. They run geometries that traverse coordinates. And the geometries are not just strategic descriptions — they are direct responses to the incumbent containment environment from Part II.

Vertical geometry (Google). Traverses Layers 1 through 9 within a single tier perimeter. Internal consistency along a column. The bet is that layer consistency compounds — that controlling a full column inside one tier beats any horizontal position. In containment terms, vertical geometry is incumbent containment perfected — Google is the only incumbent whose column extends across the Phase 1/Phase 2 boundary, which is why Google is the only incumbent that does not face the Phase 2 disintermediation risk at the same intensity as Meta or Microsoft. Strength: every layer reinforces the one above it. Weakness: brittle to failure at any single layer in the column. Google can carry this risk because Alphabet’s free cash flow can absorb single-layer disruption. Few others can.

Horizontal geometry (NVIDIA). Owns a band across Layers 3 through 5 and operates simultaneously across Tier 1 and Tier 2. The segment redraw assuming zero China data center compute as a permanent base case is NVIDIA explicitly internalizing the Tier 1 wall and pricing it. In containment terms, horizontal geometry sells shovels to the containment effort — every incumbent capex dollar that flows through Layers 3-5 pays rent to NVIDIA. The bet is that interface count compounds. Strength: every transaction that crosses the band pays rent. Weakness: hyperscaler custom silicon erodes the band from within, and merchant custom challengers flank it on physics dimensions from below.

Flywheel geometry (SpaceX). Runs engines at three different layers — Distribution (Starlink at Layer 8), Capability Substrate (launch and orbital deployment at Layers 1 and 2 in industrial logic), Models and Harness (xAI, Grok at Layers 6 and 7). Binds them through five compounding loops. In containment terms, flywheel geometry does not play the incumbent containment game at all — it operates outside the incumbents’ chosen terrain. This is structurally significant: SpaceX is not competing for the same territory the incumbents are foreclosing. It is building new territory (orbital compute, satellite distribution, integrated launch+silicon+model) that the incumbents have not yet identified as territory worth foreclosing. Strength: the compounding rate equals the geometric product of individual loop rates. Weakness: single-point-of-failure on Starship execution.

Niche by adjacent integration (Cerebras, Groq). A single layer × single tier position made defensible by other companies’ cross-layer binding. In containment terms, niche geometry occupies coordinates the incumbent containment cannot reach — specifically, the cost-per-token niches that the harness layer routes against the incumbents. The bet is that routing economics compounds. Strength: minimal capital requirement, maximum focus on a specific physics niche. Weakness: gated by whether the layer above continues to route in your favor.

The four geometries are not equivalent strategies. They are different bets about which axis compounds fastest, and they are direct responses to a containment environment that itself emerged from the incumbent paradox. Vertical bets the time axis. Horizontal bets the space axis. Flywheel bets multi-axis compounding by operating outside the contested territory. Niche bets single-coordinate optimization at defects the incumbents cannot reach.

None of them wins universally. Each captures the segment its shape is built for. Procurement teams already run multi-geometry postures by default.

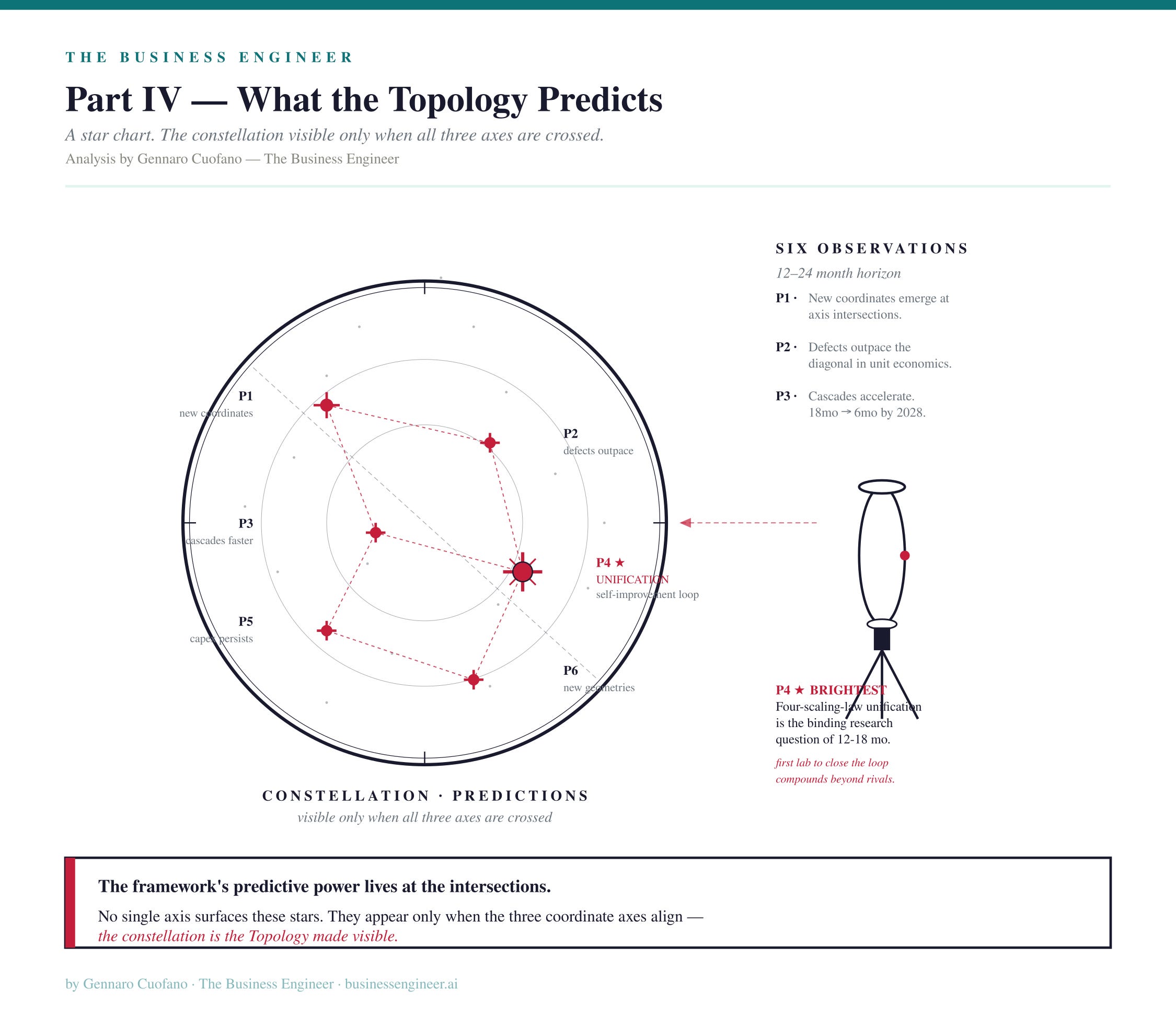

What the Topology Predicts

The Topology generates predictions that the component frameworks could not generate alone.

New coordinates emerge at the intersection of axes, not at single positions. The open-weight plus silicon co-design region was not visible to any framework that read only the time axis, only the space axis, or only the power axis. It became visible only when all three were crossed. The next 24 months will produce more such regions. Watch the intersections, not the axes alone.

Defects outpace the diagonal in specific dimensions. The diagonal of dominance produces the largest absolute revenues. Defects produce structurally different deployment economics that the diagonal cannot replicate. Over a 5-10 year window, defects will outpace the diagonal in unit economics, in deployment surface area, and in resilience to single-layer disruption. The diagonal wins on absolute scale. Defects win on compounding rate inside their niche.

Cascades will accelerate as the Topology matures. The four current cascades took 12-18 months each to propagate through multiple layers. As the Topology becomes more densely interconnected, future cascades will propagate faster. A cascade that today takes 18 months may, by 2028, propagate inside 6.

The unification of the four scaling laws is the binding research question of the next 12-18 months. Whichever frontier lab first closes the pipeline into a self-improvement loop compounds at a rate no competitor can match. This is the single highest-leverage strategic variable at the model layer, and it is currently shaping the dual-substrate compute decisions, the incumbent embedding deals, and the secondary-market premiums.

Incumbent capex will not normalize as Phase 1 matures. Incumbents will continue spending at elevated levels through Phase 2 because the strategic logic is containment, not expansion. Investors expecting capex normalization in 2027-2028 are reading Phase 1 logic into a Phase 2 contest.

New geometries emerge as new coordinates open up. The four current geometries will not be the only geometries by 2028. A “Lateral Flywheel” geometry that runs engines across Tier 2 markets (sovereign procurement, managed commerce silicon, open-weight model deployment) without running a Tier 1 engine at all — the structural form of a non-allied AI conglomerate that wins by operating cleanly outside the Tier 1 wall. Watch for the first credible Chinese conglomerate to assemble this geometry. It will be the most strategically important geometry of the second half of the decade.

What Stays Flexible

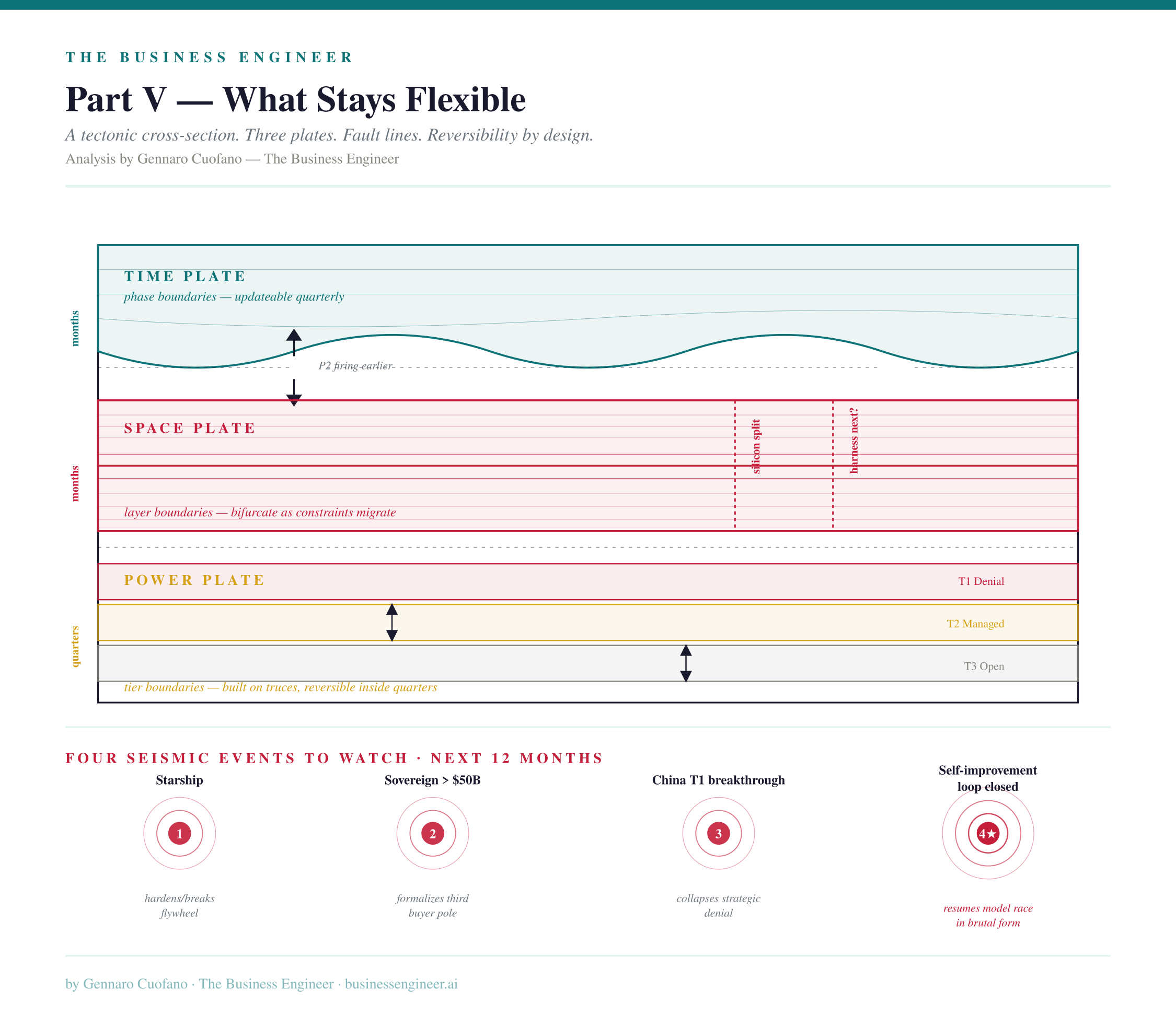

The Topology survives as new information arrives because none of its components is rigid.

Phase boundaries are descriptive, not prescriptive. Phase 2 is firing earlier than originally framed because Physical AI deployment surfaces collapsed into a single unified category faster than expected. If autonomous driving regulatory approvals accelerate, or if humanoid robotics crosses a unit-cost threshold, Phase 2 fires harder and the loaded regions shift. The phase axis is updateable on a quarterly cadence.

Layer boundaries bifurcate as binding constraints migrate. Silicon already split three ways. Networking may split intra-rack versus inter-rack. Harness may split routing versus orchestration. Distribution may split web-native from Physical AI surfaces formally. Governance is already behaving more like a perpendicular control plane than a layer at the top. The space axis is topologically stable. Its internal differentiation is not.

Tier boundaries are built on truces, not treaties. The architecture has reconfigured inside 72 hours under court pressure. A China-side Tier 1 breakthrough — CXMT HBM at competitive yields, SMIC sub-5nm at volume — would collapse Strategic Denial in semiconductors and reorganize the entire power axis below the foundation model layer. The tier axis is reversible inside quarters, not decades.

Four events to watch in the next twelve months that would force a redraw of the Topology.

First, a Starship outcome that hardens or breaks Flywheel geometry. Aircraft-like cadence collapses or reinforces the entire third-geometry region of the Topology and validates or invalidates the orbital compute roadmap.

Second, a sovereign procurement crossing $50 billion in a single contract. That moment formalizes the third buyer pole as a permanent feature of Layer 5 and gives sovereigns formal contracting frameworks rather than ad hoc deals.

Third, a China-side Tier 1 breakthrough at the silicon or foundry layer. Any credible move at CXMT, SMIC, or indigenous EUV equivalents collapses Strategic Denial in semiconductors and reorganizes the power axis below the foundation model layer.

Fourth, a credible signal that one frontier lab has closed the four-scaling-law unification into a working self-improvement loop. That event resumes the model race in a more brutal form and reshapes every other variable in the framework — frontier-lab valuations, compute procurement, incumbent embedding deals, governance posture.

The Topology is not a snapshot. It is a working surface. The coordinates loaded today were not all loaded twelve months ago. The coordinates that will be loaded twelve months from now are not all visible from here.

The Reading Discipline

For any company, specify three coordinates. Which layers does it occupy in the Map of AI? Which phase is each of those layers in? Which tier governs commercial access to each layer? Then ask the strategic question: is the company’s geometry compounding faster or slower than the coordinates it occupies?

A company occupying a Phase 1 layer with a vertical geometry compounds through ownership consistency along its column. Google in 2026.

A company occupying a horizontal band that spans Tier 1 and Tier 2 compounds through interface rent across its band. NVIDIA in 2026.

A company occupying three layers at three different phases through a flywheel compounds through loop interaction — and is gated by whichever loop is weakest. SpaceX in 2026, gated by Starship.

A company occupying a single layer in a single tier with a niche geometry compounds through routing economics — and is gated by whether the layer above continues to route in its favor. Cerebras in 2026, gated by the agentic harness layer’s continued willingness to route on cost-per-token.

A company occupying an open-weight Tier 2 coordinate compounds through silicon co-design and deployment surface area — and is gated by whether the Tier 1 wall holds or collapses. DeepSeek in 2026, gated by US export-control policy and CXMT yields.

A company sitting on incumbent distribution at Phase 1 with massive capex containment compounds through foreclosure of optionality for native AI players — and is gated by whether Phase 2 disintermediation arrives before the containment is complete. Meta in 2026, gated by whether 3 billion users continue to engage with social and advertising surfaces in their current form.

For any technology, ask the same three coordinates. Robotics? Layer 8 distribution surface, Phase 2 unlocking now, Tier 2/3 commercial access depending on jurisdiction. Reasoning models? Layers 6 and 7, deep in Phase 1, Tier 1 for frontier weights. Open-weight inference clouds? Layer 5 with a Layer 3 dependency, Phase 1, Tier 2/3.

Each technology lives at a coordinate. Each coordinate has a different compounding rate, a different risk profile, and a different access regime. The discipline is to refuse to talk about “AI” in the singular and instead specify the coordinate.

Key Takeaways & Mental Models

The Dual Analogy. AI is microprocessor-like at the physical supply chain (Layers 1-5) and Cold-War-like at the frontier (Layers 6-9). Mechanism: the two regimes collide at the boundary between Compute Capacity and Foundation Models — and that collision is what makes the Three-Tier Architecture structurally necessary rather than politically contingent. The Cold War reference is about governance architecture, not about damage potential.

The Topology. The AI cycle is best read as three orthogonal axes — time (Supercycle phases), space (9-layer Map of AI), and power (Three-Tier Architecture). Mechanism: each axis answers a question the others cannot. The strategically interesting action lives where all three intersect.

Coordinates over Cells. Companies and technologies do not occupy fixed positions. They occupy coordinates that may move next quarter. Mechanism: the reading discipline is to specify coordinates, which forces awareness that the Topology is deforming around the company in real time.

The Four Scaling Laws and the Unification Question. Pre-training, post-training, reasoning, and agentic tool use are running in parallel. The binding research question of the next 12-18 months is whether they can be unified into a self-improvement and continual-learning loop. Mechanism: unification, if achieved at a single frontier lab first, compounds at a rate no competitor can match — and reshapes every other variable in the framework.

The Incumbent Paradox, Both Halves. Phase 1 favors incumbents through linear integration of their existing advantages. Phase 2 favors native AI players through non-linear business-logic change. Mechanism: incumbents who have internalized the second half spend at unprecedented capex scales to foreclose Phase 2 territory before native AI players can occupy it. The capex is backward-induced from Phase 2 survival anxiety, not forward-projected from Phase 1 expansion.

Capex as Containment. The scale of incumbent spending only makes sense as a containment strategy, not as a linear-integration strategy. Mechanism: incumbents are building moats deep enough to survive disintermediation by foreclosing the territory at every layer of the substrate before native AI players reach it. The strategy explains the willingness to crater near-term free cash flow, the urgency of distribution embedding deals, and the aggressive consolidation of compute capacity.

The Diagonal of Dominance. Structural dominance concentrates along a diagonal running from current-phase to strategic-layer to high-tier. Mechanism: the largest companies in the cycle have positioned along the diagonal because the diagonal contains the largest profit pools — but the diagonal is sensitive to which regions stay loaded with rent.

Defects as Topological Anomalies. Coordinates created by Tier 1 walls or incumbent containment are topological defects that produce novel commercial properties incumbents cannot replicate. Mechanism: geometries built under structural constraint develop deployment economics that diagonal incumbents cannot reproduce without abandoning their own positions.

Cascades as Propagation Logic. Cascades are deformation events that propagate through coordinates, reshaping which regions are loaded. Mechanism: cascades propagate faster through layers than through tiers. Layer-level disruption is technical and responds to demand pressure; tier-level disruption is political and responds to negotiation cycles measured in quarters.

Geometries as Containment Response. Vertical, Horizontal, Flywheel, and Niche by Adjacent Integration are direct responses to the incumbent containment environment. Mechanism: vertical perfects incumbent containment; horizontal sells shovels to it; flywheel operates outside the contested territory; niche occupies defects containment cannot reach.

Reversibility by Design. The Three-Tier Architecture is built on truces, not treaties. Mechanism: the Topology tolerates frequent reconfiguration because no single tier boundary is treaty-grade. A court ruling, a single breakthrough, a single sovereign procurement can move a coordinate from one tier to another inside a quarter.

Governance as Perimeter, Not Roof. Layer 9 and the meta-tier of the Three-Tier Architecture describe the same object from different angles. Mechanism: governance does not sit on top of the stack — it surrounds the stack as a control plane perpendicular to every layer, and its charge comes from the political tier system that gives it teeth.

The Reading Discipline. Refuse to talk about “AI” in the singular. Specify the coordinate. Mechanism: every technology, every company, every commercial decision lives at a coordinate, and the coordinate determines the compounding rate, the risk profile, and the access regime.

The Bottom Line

The model race did not end. It paused at the boundary of the four-scaling-law unification question and will resume in a more brutal form when one frontier lab closes the pipeline first. The geometry race began in parallel, structured around the incumbent containment environment that the capex map made visible. Neither race is the whole story, because both are traversals through a coordinate system that the component frameworks describe separately and the Topology describes together.

The microprocessor analogy explains the physical supply chain of AI — energy, foundries, silicon, networking, compute. It tells you why bottlenecks cascade, why allocation power matters more than chip design, why incumbents capture early value in Phase 1.

The Cold War analogy explains the governance regime around the frontier — foundation models, agentic harness, distribution surfaces, governance perimeter. It tells you why capability denial is structurally permanent, why three-tier control regimes are stable, why dual-substrate strategic redundancy is being priced into valuations, why sovereign procurement is emerging as a non-aligned procurement category.

The two analogies meet at the boundary between Layer 5 and Layer 6. The Three-Tier Architecture exists because the two regimes collide at this boundary. And the Topology is the unified working surface that holds both regimes in one frame.

The Supercycle tells you when value emerges across the layered stack — and what binding research question is shaping the next 12-18 months. The 9-Layer Map tells you where value accumulates. The Three-Tier Architecture tells you who is allowed to operate. The capex map tells you why incumbents are spending at containment scales rather than integration scales. The geometries tell you how companies traverse the Topology. Cascades tell you which coordinates will be loaded next.

Most of the strategic action of the next decade lives at coordinates that exist only when all three axes are crossed. The open-weight plus silicon co-design coordinate. The sovereign procurement coordinate. The Tier 2 managed-commerce silicon coordinate. The Physical AI distribution coordinate. The rack-scale networking coordinate. The unified self-improvement loop coordinate, when it arrives. None of these are visible from any single framework alone. All of them are doing work today.

Three years of frameworks have converged on a single working surface. The Topology will look different again in seven weeks. The discipline is to keep reading by coordinates, not by labels.

Stay close.

With massive ❤️ Gennaro, creator of The AI Supercycle, a spin-off of The Business Engineer